by Clifford Asness, Ph. D. AQR Capital Management, Inc.

Just how volatile was the recent market ride? Cliff Asness puts the volatility into perspective in terms of both its absolute and surprise levels.

You don’t need me to tell you that markets have been pretty wild lately. But, perhaps I can help with a little perspective versus history, and try to home in on what was merely big about these past few days versus what was really really big. Warning, this one gets a bit wonky with some number overload.

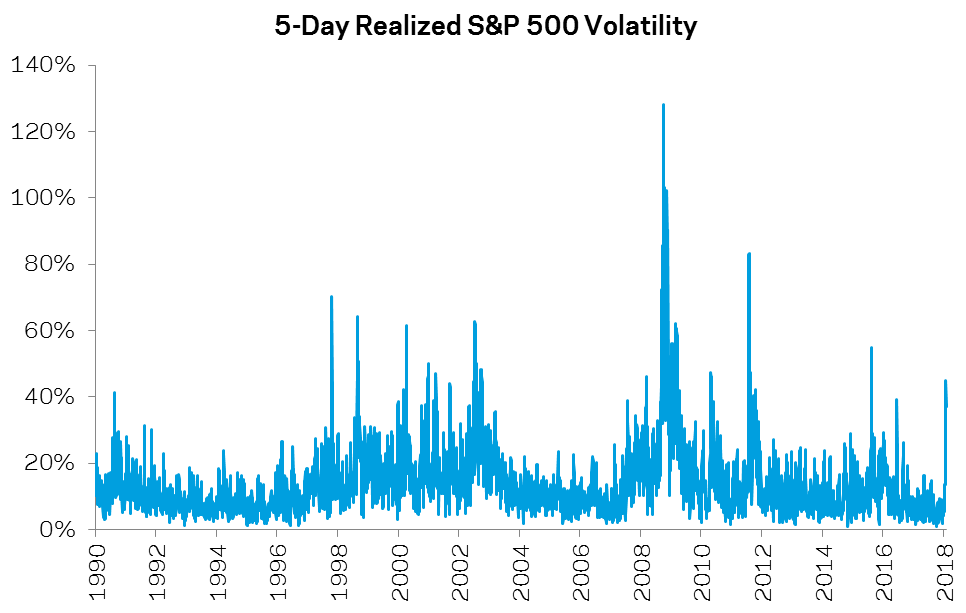

In this note, I look at rolling 5-day daily volatility of the S&P 500 starting from 1990, when we also have data on the VIX. 1 2 3 For the five days central to this swoon (2/2/2018 – 2/8/2018 4 ) the annualized daily volatility was 38.9%. 5 6 That’s big. But we’ve seen much bigger. The maximum occurred, not surprisingly, in the teeth of the Global Financial Crisis (10/09/2008 – 10/15/2008), hitting 128.2% annualized over those five days (and a nice example of the silliness of annualizing 5-day events!). The 99th percentile 5-day rolling volatility from 1990-present is 55.5%, and the recent 5-day period of 38.9% registers a 97th percentile. Sure, those are big outcomes, but two standard deviation events are a dime a dozen in financial markets. To put it into perspective, below I graph this realized 5-day volatility back to 1990.

Source: Bloomberg, AQR, Jan 9, 1990 through Feb 12, 2018. For illustrative purposes only.

Clearly recent events were big, but similar things have occurred quite a few times, and much bigger ones happened during the GFC.

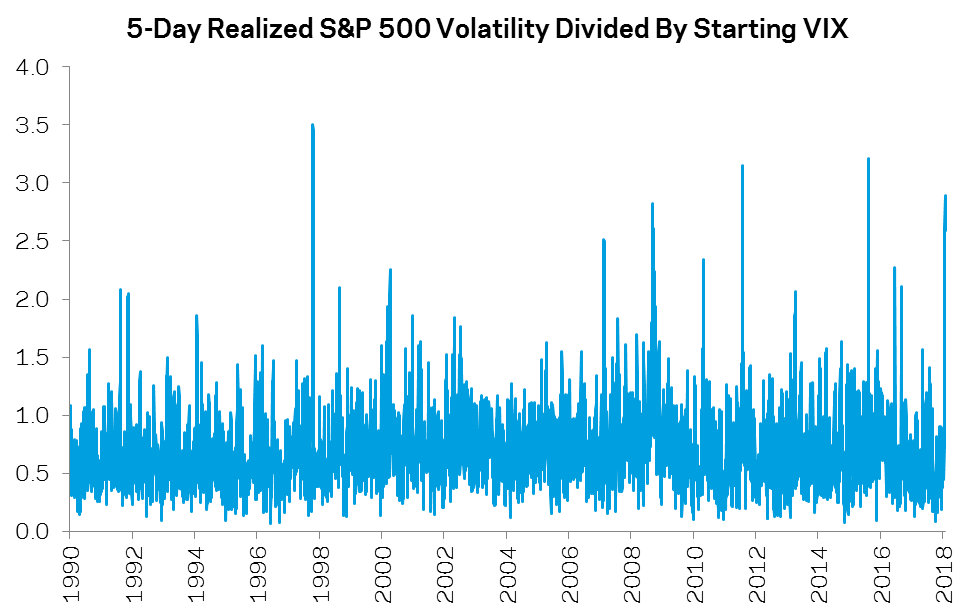

Now, let’s look at it slightly differently. We’re still sticking with our very short-term 5-day volatility measure, but now let’s look at it as a ratio to the level of the VIX at the start of each 5-day period. This is potentially very different. To the extent the VIX measures forward-looking volatility expectations, this ratio is a measure of how surprising, not simply how big, 5-day volatility turned out to be. As the graph below shows, at the worst drawdown during this recent period, 5-day realized volatility (38.9%) was a whopping 2.9x larger than the starting VIX level (13.5%). This was a +3.3 standard deviation event (again, using logs to normalize the series), which is extreme but still something that occasionally happens per the graph below. Clearly, the recent downturn has been more extreme versus the past in terms of “surprise volatility,” as compared to simply volatility itself. In particular, note that the GFC still produces some biggies, but not wildly larger surprises versus other periods as the volatility was less surprising (it didn’t come as much out of the blue as the VIX correctly ex ante captured some of it, likely because trailing volatility was high for a while).

Source: Bloomberg, AQR, Jan 9, 1990 through Feb 12, 2018. For illustrative purposes only.

The maximum ratio ever hit was 3.5x (over the period 10/22/1997 – 10/28/1997), when U.S. stock markets declined during the 1997 Asian financial crisis. This 1997 maximum surprise came about in a somewhat different way than recent events. Unlike last week, the VIX didn’t start this 1997 stretch low and then get hit with big vol. Rather, it began on 10/21/1997 with a VIX of 19.5%, which is the 60th percentile (last week’s drawdown began from a VIX of 13.5% which is the 24th percentile 7 ) and then experienced a 68.4% annualized 5-day volatility (99th percentile), considerably higher than last week’s high levels. The story of 1997’s surprise was extremely high realized volatility (though not hitting 2008 levels, which were even higher, but not a bigger surprise – yes, I know it’s getting a little hairy in here!) compared to an above average starting VIX. In slight contrast, last week’s surprise was quite high, but it came from less extreme realized volatility (a recent level of 38.9% for the 5-day drawdown period and a max of 44.9% shifting to one day later vs. 68.4% in the 1997 event) compared to a fairly low starting VIX. This highlights how looking at surprises can be somewhat different than just looking at volatile periods. The very recent surprise was high, similar to the 1997 surprise, but the absolute level of volatility wasn’t as extraordinary.

Now let’s apply the above to examine a real life investing issue. Some investors use volatility forecasts to vary their investment size in an attempt to target more stable returns, effectively holding larger positions after periods of low volatility (or a low VIX 8 ) and smaller positions after periods of high volatility (with an assumption that volatility is fairly “sticky” so these trailing levels have power to forecast the upcoming future). Recent events have to be pretty bad for those who try to target such a constant volatility, right? They must have been positioned way too aggressively given the VIX was so low, and thus, had to get hit much harder by the surprise in realized volatility, right? Well, in a word, yes. But that’s not the whole story by a long-shot.

To study this, I build a toy risk-model (that is, a risk-model I hope gets at the main point but is way simpler than one you’d likely use in real life). I imagine an investor trying to target a 15% 9 constant volatility exposure to the S&P 500 (or, to be fussy, the S&P 500 and cash, as varying the amount of cash is how this is done) using today’s VIX to make the decision whether to lever up (when the VIX is forecasting lower than 15% volatility) or de-lever (when the VIX is forecasting higher than 15% volatility). Now, even in a toy model, I can’t just use a VIX of 25 to say “the VIX is forecasting a 25% annualized volatility.” That toy would be broken at the get-go. The VIX reflects option-based implied volatilities that average decently higher than realized volatility (leading to the so-called volatility or variance risk premium). So I enhance the risk-model (though I’d still call it a toy!) to adjust for the VIX’s average overstatement.I look back over the prior rolling three years and measure the ratio of the median VIX to the median realized 5-day S&P 500 volatility, and use this ratio in conjunction with the VIX level to size positions at each point in time. So if that ratio has been 1.5x (meaning the VIX overstated volatility by 50%) over the last three years and the VIX is at 30 now, I’d use 20% (30 divided by 1.5) for predicted volatility. So, in this case, to keep a constant 15% volatility I’d de-lever the S&P by being 75% long (15%/20%). 10 11 Got it?☺

So imagine you used this way-too-simple model to manage your S&P 500 exposure from 1993 - present. 12 That is, instead of a regular S&P 500 index fund, you ran a “constant vol” S&P 500 index fund using this method. First, your price return was about 2% better per annum. I don’t take that too seriously. Even 25 years isn’t that long to estimate mean returns (and I know that in some other asset classes, like bonds, this has gone the other way over this period). 13 This is about volatility/downside management so that’s what I focus on next.

Well, not surprisingly, the recent swoon was indeed worse for the constant vol crowd. The S&P’s recent drawdown (1/29/2018 – 2/8/2018) was -10.2% while the (toy risk-model) constant vol targeters fell -14.5%. Sounds ugly. And indeed it was ugly, as you’d expect for such a big surprise that starts from a low vol (and thus high exposure for vol targeters) place. If one takes the full series (1993 - present) targeted vol S&P 500 daily return compounded over these nine days and subtracts the regular S&P 500 daily return, the -4.3% difference (-14.5% vs. -10.2%) was a -3.3 standard deviation event. 14 15 So, we are definitely looking at a pretty bad event for those targeting volatility. That’s the view from the trees of recent turmoil. Let’s move to the forest.

Let’s look at the risk characteristics over not just the recent turmoil but the whole 1993 - present experience (which certainly includes the recent big moves). The S&P 500’s daily returns over this period realized an annualized volatility of 17.7% 16 , a skewness of -0.1, and a kurtosis of 9.5 (extremely “non-normal”). The volatility-targeted S&P 500’s daily returns realized an annualized volatility of 16.9%, a skewness of -0.4, and a far more “normal” kurtosis of 1.7. The worst day for the S&P 500 was -9.0% vs. -7.7% for the vol-targeted version.

Over 20-day rolling return windows, the regular S&P 500 delivered a skewness of -0.8 and a kurtosis of 4.1, vs. -0.1 and 0.2 for the very “normal” looking vol-targeted version from 1993 - present. The worst rolling 20-day period was -28.2% for the S&P 500 versus a way smaller -15.1% for the vol-targeted series. Looking at one year rolling return windows, the worst case for the S&P 500 was -49.1% vs. -34.6% for the vol-targeted investment (both series start to look pretty normally distributed at the rolling annual horizon). 17 Finally, if we look at the worst drawdowns over the whole sample, the S&P 500 comes in at 56.8% with the vol-targeted version at -48.8% (sorry, vol targeting can’t save you from bad times, though perhaps can sometimes make them a bit less painful). 18

The point here isn’t to extoll this exceedingly simple model or even volatility targeting itself. The point is that anything should be evaluated over as long a time-frame as possible (and for which you have relevant data). Over this 25-year period, using just the VIX (adjusted for its average overstatement) to target volatility has led to a decently more stable investment than just the S&P 500 itself, even considering the recent surprise that’s gone against it, and total returns at least as good (recall they were actually considerably better but we, mostly, don’t believe that’s a permanent property of this approach).

Back to our main story. As of now (no predictions going forward!) this recent wild period is not super crazy when we look just at volatility itself (it’s high, but not super high vs. history). But, when we look at it as a surprise (by comparing the realized 5-day volatility to the starting VIX) it’s a considerably more shocking event, though still not unprecedented. Similar events have occurred five or so times in the 1990 - present history (again, see the above figure). Finally, when just using the simple method of targeting constant volatility that we employ here, this recent surprise swoon was, as we’d expect, pretty bad for volatility targeters. But, over the longer term, volatility targeting, even the super simple volatility targeting our toy risk-model employs, may, on average, deliver more downside stability than not volatility targeting and implicitly letting the market dictate the volatility of your investment.

******

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of AQR Capital Management, LLC, its affiliates or its employees.

This document has been provided to you solely for information purposes and does not constitute an offer or solicitation of an offer or any advice or recommendation to purchase any securities or other financial instruments and may not be construed as such.

The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Diversification does not eliminate the risk of experiencing investment losses.

Please note that changes in the rate of exchange of a currency may affect the value, price or income of an investment adversely.

The factual information set forth herein has been obtained or derived from sources believed by the author and AQR Capital Management, LLC (“AQR”) to be reliable but it is not necessarily all-inclusive and is not guaranteed as to its accuracy and is not to be regarded as a representation or warranty, express or implied, as to the information’s accuracy or completeness, nor should the attached information serve as the basis of any investment decision.

Information contained on third party websites that AQR Capital Management, LLC, (“AQR”) may link to are not reviewed in their entirety for accuracy and AQR assumes no liability for the information contained on these websites.

Toy Risk Model Source: AQR, using data from Bloomberg, for the period Jan 23, 1990 through Feb 12, 2018. For illustrative purposes only and not representative of a portfolio that AQR currently manages. Hypothetical Data has inherent limitations, some of which are disclosed herein. Not to be construed as investment advice or a specific recommendation. There is no guarantee, express or implied, that long-term return and/or volatility targets will be achieved. Realized returns and/or volatility may come in higher or lower than expected. There is no guarantee that this strategy will be successful.

The results shown represent a hypothetical illustration. Hypothetical or simulated performance results assume the portfolio holding(s) were purchased on the first day of the period indicated. The hypothetical or simulated performance results are compiled with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. Changes in the assumptions may have a material impact on the model presented. Other periods may have different results, including losses. There can be no assurance that the analysis will achieve profits or avoid incurring substantial losses. AQR did not manage or recommend this allocation to clients during periods shown, and no clients invested money in accounts managed by AQR in accordance with the recommended allocation.

There is a risk of substantial loss associated with trading commodities, futures, options, derivatives and other financial instruments. Before trading, investors should carefully consider their financial position and risk tolerance to determine if the proposed trading style is appropriate. Investors should realize that when trading futures, commodities, options, derivatives and other financial instruments one could lose the full balance of their account. It is also possible to lose more than the initial deposit when trading derivatives or using leverage. All funds committed to such a trading strategy should be purely risk capital.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from AQR.

This post was originally published at AQR Capital

Copyright © AQR Capital