by Scott Minerd, CIO, Guggenheim Partners LLC

The last two weeks have been pretty exciting, certainly a lot more interesting than anything we’ve been through over the last year. Given the recent market dislocation, there is a basis to rebalance portfolios and do trades to take advantage of relative repricing. At a macro level, it should not surprise anyone that rates have begun to rise—we have been talking about the Federal Reserve (Fed) tightening, we have been talking about how the Fed is behind the curve, how the market has not believed the Fed, and that someday this was going to have to get resolved, probably by the market having to adjust to the Fed’s statements.

The market has now gotten the joke. I still don’t think the yield curve is accurately priced, but it is a lot closer today than where it was at the beginning of the year.

The concern, as I explained in A Time for Courage, is that now the market is moving from complacency—where it really did not believe the Fed was going to do what it said it was going to do—to a time when it has begun to realize that the Fed may be behind the curve. The market is now coming to believe that the Fed is not going to make three rate increases this year, it is going to make four. And so, rates start to rise and the whole proposition that the valuation of risk assets is based upon, which is faith in ultra-low rates and continued central bank liquidity, comes into question. As markets lose confidence in that view. investors have started to rearrange the deck chairs by repositioning portfolios.

Anytime we see strength in economic data, we are going to see upward pressure on rates. Upward pressure on rates is going to result in concern over the value of risk assets, and we are going to have a selloff in equity markets, or the junk bond market, or both. Credit spreads will widen. The reality of the situation, however, is that the amount of fiscal stimulus in the pipeline, the U.S. economy fast approaching full employment, the economic bounceback in Europe, and the pickup in momentum in Japan and in China are all real. Against this backdrop, even a harsh selloff in risk assets is not going to derail the expansion.

The Fed knows this, and for that reason the Fed is shrugging its shoulders and saying, “Okay, we don’t have a mandate around risk assets, but we do have a mandate about price stability and full employment. And it looks like we’re at full employment or beyond full employment, and the thing that seems to be at risk now is price stability. We’ve got to raise rates.”

What does that mean for investors? Markets are engaged in a tug of war between higher bond yields and the stock market. In the near term, the two markets will act as governors on each other: Higher bond yields will drive down stock prices, and lower stock prices will cause bond yields to stop rising and to fall.

"The market is moving from complacency about the Fed to realizing that it may be behind the curve."

An analogue to today may be 1987. That year began against the backdrop of 1985/1986, which had seen a collapse in energy prices. In 1986 oil prices were very low, and concerns around inflation had diminished. The Federal Reserve had dragged its feet on raising rates. As we entered 1987, in the first few months of the year the stock market took off. By the time we got to March, stocks were up 20 percent. In April there was a hard correction of approximately 10 percent. As fear overtook greed, market participants became cautious on stocks. Going into that summer the stock market rallied another 21 percent from the April lows.

By August we were at record highs; interest rates started to move up; the Federal Reserve was raising rates; the dollar was under pressure; and there were increasing concerns over inflation. The concern was the Fed was behind the curve as it accelerated rate increases. By October things were becoming unhinged. Bond yields had risen in the face of an extended bull market in stocks. The market reached a tipping point and began its infamous slide. By the time we got to the end of the year, the stock market for the year was up just 2 percent. That was the stock market crash of 1987, which wiped out about a third of the value of equities in the course of a few weeks.

Today, investors have the same sorts of concerns they had in 1987. For now, the market has gotten a reprieve. Soon, investors will start to have confidence in risk assets again. Risk assets like stocks will start to take off. Eventually, the perception will be that the Fed is falling behind the curve because inflation and economic pressures will continue to mount. Eventually the Fed will acknowledge that three rate hikes will not be enough, but it is going to raise rates four times in 2018, and market speculation will increase that there may be a need for five or six rate hikes. That will be the straw that breaks the camel’s back.

This is a highly plausible scenario for this year, but who knows how these things play out in the end. The reality today is that the economy is strong, interest rates are rising, and equities look fairly cheap. The Fed model right now would tell you the market multiple should be 34 times earnings. That is just fair value, not overvalued. And based on current earnings estimates for the S&P this year, the market multiple is closer to 17 times earnings. If stocks go down by 10 percent, the market multiple would drop to 15 times earnings. This would be getting into the realm of where value stocks trade. If there were a 20 percent selloff, you’re at a 14 times multiple. These market multiples don’t make sense. Markets do not price at 14 times earnings in an accelerating economic expansion with low inflation.

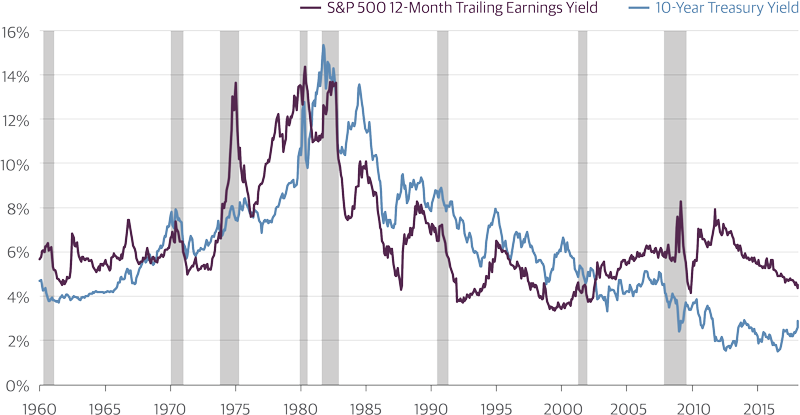

Stocks Are Cheap

Equity earnings yields* exceed still-low Treasury yields.

Source: Bloomberg, Guggenheim Investments. *Earnings yield equals the inverse of the price/earnings ratio. Data as of 2.16.2018.

I found it interesting that as the 10-year Treasury note started to approach 3 percent the world went into a panic. It is easy to see what happens to the yield curve as the Fed tightens. A few weeks ago the 2s/10s curve was around 50 basis points; today it is at 74. You can see in the nearby chart the downtrend over the last three years in 2s/10s and 2s/30s curves. We had moved so far away from trend that a temporary steepening was to be expected. These spreads have stabilized, which means we could very well be back to the flattening trade. But if these spreads blow out further and the curve continues to steepen, then we have to start thinking that maybe there is something more seriously wrong in a reflationary sense.

Nevertheless, the Fed has made it clear that it is not going to let inflation take off. The Fed is going to continue to tighten, and as the Fed continues to tighten it’s going to continue to put flattening pressure on the curve.

The Fed is due to tighten again on March 21. At that time we will get some clues as to whether it is their view to become cautious or reinforce their inflation-fighting commitment. We are at a very interesting juncture in the market, and it can be very nerve-wracking. If you think of this as a crisis, then I always am reminded of the two Chinese characters for crisis, the first meaning danger, the second meaning opportunity. There is danger here, but there is also a lot of opportunity, and that is why it is a time for courage.

Yield Curve Flattening Trend Is Intact

The Treasury yield curve has been flattening for several years. As the Fed continues to tighten, it will exert flattening pressure on the curve.

Source: Bloomberg, Guggenheim Investments. Data as of 2.14.2018

Important Notices and Disclosures

Investing involves risk, including the possible loss of principal.

2s/10s curve: the difference between the two-year Treasury yield and the 10-year Treasury yield. 2s/30s curve: the difference between the two-year Treasury yield and the 30-year Treasury yield. Basis point: 1 basis point equals 0.01%.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author or speaker, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. No part of this material may be reproduced or referred to in any form, without express written permission of Guggenheim Partners, LLC.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Real Estate, LLC, GS GAMMA Advisors, LLC, Guggenheim Partners Europe Limited and Guggenheim Partners India Management.

©2018, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC.