Russ reviews the landscape after the selloff and discusses how little has actually changed.

Monday was all about superlatives: the largest one-day point drop in the Dow Jones Industrial Average and the biggest one-day percentage change in the VIX Index. Apart from the gyrations, Monday was also distinguished in another respect: There was no obvious catalyst for the spike in volatility. While last Friday’s stronger-than-expected jobs report spooked investors, a slight acceleration in wage growth does not typically result in a doubling of volatility.

Instead, as has happened in the past, market volatility was less about the economy and more about unwinding extremely crowded trades, most notably a bet on low volatility.

As the dust settles, if only temporarily, investors are left wondering what has changed. From my perspective, not much.

1. The selloff was narrow, not systemic.

Although it was hard to find much comfort in Monday’s volatility, it is worth highlighting that the selling was mostly confined to stocks. This should be treated as a positive. While there is no law of nature that prevents divergences between asset classes, systemic selloffs, by definition, involve more than one asset class. Other asset classes, most importantly credit, proved more stable. High yield spreads have widened about 25 basis points (bps, or 0.25%) from the late January low. Still, at approximately 335 bps, spreads are only back to where they were earlier in the year. In contrast, during the correction in early 2016, spreads widened to over 800 bps.

2. The magnitude of the rise in volatility is unlikely to last.

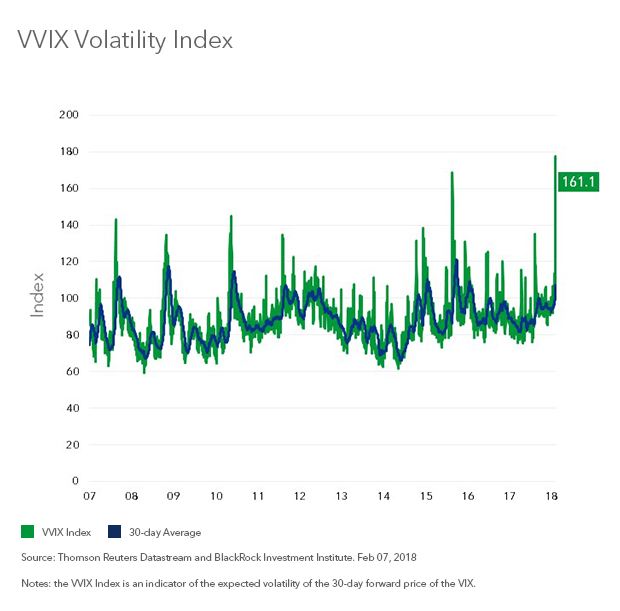

The stability in spreads is important because historically spreads are the best coincident indicator of equity market volatility. As I’ve discussed in previous blogs, if investors are really concerned about the economy, they should demand a higher premium to loan to more speculative companies. This is not the case today. Given still benign financial market conditions and a solid economy, a simple model of the VIX suggests U.S. equity market volatility should be trading in the mid-teens, not over 30. Put differently, the spike in volatility appears completely disproportionate (see the chart below). For the first time in years, implied volatility looks too high relative to the real economy and credit markets.

3. U.S. stocks are still very expensive.

While the selloff can be explained by position unwinding, the simple fact is that as we approach the 10th year of the bull market, volatility is likely to pick up. The crowding in short-volatility positions is evidence of a broader trend: increased risk taking. For long-term investors the most important manifestation of that trend is a U.S. stock market trading at elevated valuations that do not discount much in the way of bad news.

Where does that leave investors? The good news is that this most recent bout of market volatility appears both exaggerated and contained. A +1000 point slide in the Dow Jones Industrial Average and a one-day doubling in volatility do not reflect any deterioration in the real economy. The bad news? With valuations stretched and investors straining in ever more creative ways for returns, calm is unlikely to reign for long.

Russ Koesterich, CFA, is Portfolio Manager for BlackRock’s Global Allocation team and is a regular contributor to The Blog.

Investing involves risks, including possible loss of principal.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of February 2018 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

©2018 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

422771