by Richard Turnill, Global Chief Investment Strategist, Blackrock

Richard draws lessons from a year that saw surprisingly large returns, falling inflation and flat long-term bond yields.

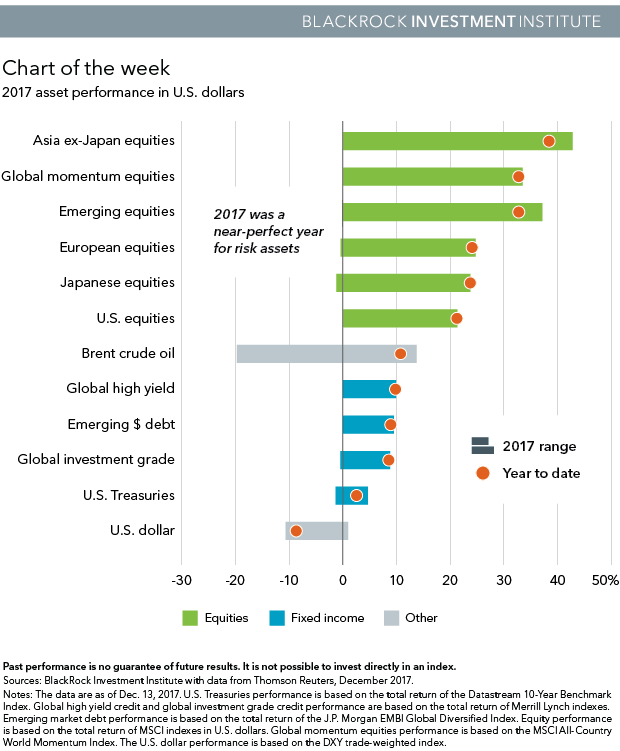

The past year turned out to be more bullish than we anticipated. Consensus growth expectations caught up to ours and global earnings jumped—but the magnitude of asset returns surprised us. Most asset classes have performed well, with many delivering double-digit returns, as shown in the chart below.

The events many worried about in early 2017—including the election of a far-right government in France and aggressive U.S. trade policy—didn’t materialize. The MSCI ACWI closed at a record high 61 times, and 30-day realized volatility of the S&P 500 Index hit its lowest level since the early 1960s. Other surprises: Inflation fell and long-term bond yields were flat even as the economy improved, while cryptocurrencies posted huge returns.

Five lessons from the past year

The big stock market winners in 2017 include emerging market and Asian equities, the momentum style factor (stocks trending strongly higher in price) and the technology sector. The lesson here: Sustained, above-trend economic growth has helped companies deliver on earnings, fueling strong equity returns. All major regions increased earnings at a clip faster than 10%, Thomson Reuters data show. We expect more good things in 2018, but 2017 earnings performance will be a harder act to follow.

Two other lessons: First, low volatility can be sustained for longer than many expect. Our research shows that equity market volatility tends to stay low in steady economic expansions, provided systemic financial vulnerabilities remain in check. We see no such risks on the horizon at present, notwithstanding pockets of froth in the credit markets. Second, geopolitical risks are not all created equal. It’s worth taking the time to look through what may be excessive market fears. This was our approach to Europe. The French presidential election result put fears of a eurozone breakup to rest, a “soft Brexit” appears to be emerging, and the eurozone has managed to eke out the fastest growth since March 2011. But a tougher U.S. stance to trade still looms as a major threat to the global free-trade regime.

The final lessons? Low bond yields are not just about the Federal Reserve (Fed), and currencies can be wildcards. U.S. 10-year yields are broadly flat, 30-year yields lower, and the U.S. dollar down for the year—even as the economy improved, and the Fed raised rates and announced it would start shrinking its balance sheet. A soft patch in inflation is partly why. We see this dynamic reversing in 2018 as U.S. core inflation rises back above 2%. Yet we also see structural factors, including a post-crisis rise in global savings, as capping long-term rates as the Fed presses ahead with further rate rises in 2018. The bottom line: 2017 was a near-perfect year for risk assets. What’s ahead? Check out our 2018 Global Investment Outlook, and read more market insights in my Weekly Commentary.

Richard Turnill is BlackRock’s global chief investment strategist. He is a regular contributor to The Blog.

Copyright © Blackrock