by Russ Koesterich, Portfolio Manager, Blackrock

Gold has performed surprisingly well this year. Russ discusses why that might not be the case going forward, and it may be time to pare positions.

For a year in which risky assets continue to grind higher, assets offering potential hedges against those risks are doing remarkably well. Long-duration U.S. bonds are up roughly 9% while gold has advanced better than 11%. The latter’s performance is particularly surprising.

Gold is up in an environment in which investors have had little reason to hedge; any market pullback has been both mild and fleeting. Yet gold has kept pace with the overall returns of a typical 60/40 portfolio. In other words, this has been an unusual year in that your hedges have not cost you anything in the form of foregone returns.

That said, I would be inclined to hold a bit less gold into year’s end and early 2018. My message: Trim, but don’t abandon, the asset class. Here’s why.

1. Washington

Back in late August I discussed the relationship between gold, political uncertainty and tax reform. While still not a sure thing, the odds of tax reform have risen since late summer. Fiscal stimulus in the form of a tax cut would arguably undermine gold in two ways: marginally higher real, or inflation-adjusted, interest rates, and less political uncertainty. As discussed in previous blogs, the best predictor of gold’s performance is the level of real rates. Marginally faster growth, even if only modest and temporary, is likely to put some upward pressure on real rates and correspondingly downward pressure on gold.

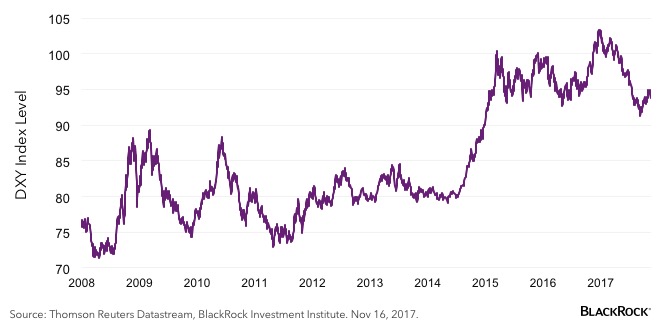

2. The U.S. dollar

One reason gold has done as well as it has year-to-date is weakness in the dollar. The U.S. Dollar (DXY) Index is down more than 9% from its early January high. More recently, however, the dollar has been firmer as investors have repositioned for a slightly more aggressive Federal Reserve (see the accompanying chart). In the near term I would expect a steadier dollar, particularly if the proposed tax cuts pass. A firm dollar removes another support for gold.

U.S. Dollar Index (DXY)

Where does this leave investors? Still holding gold, just a bit less. For most investors, this means somewhere in the mid to single digits, as a percentage of their asset allocation.

But it’s important to note, while the near-term environment for gold is not ideal, there are still good reasons to maintain some exposure, including the diversification benefits. With the exception of long-dated U.S. bonds, gold continues to be one of the more diversifying asset classes.

In most instances of higher volatility, gold provides a hedge against not only equity risk but credit as well. With credit spreads tight (i.e. a sign that bonds are expensive) and U.S. equity valuations still stretched, investors may consider lightening up on their portfolio insurance, but they should not abandon it.

Russ Koesterich, CFA, is Portfolio Manager for BlackRock’s Global Allocation team and is a regular contributor to The Blog.

Copyright © Blackrock