Now May Be a Good Time to Increase Exposure to International Equity

by Matt Bennett, Vice President, Fidelity Investments

Key Takeaways

• The multiyear rally in U.S. stocks has left many equity portfolios with a home-country bias and less diversification than expected.

• While investors with a home-country bias may have done well in recent years, international stocks have rallied strongly of late, and many indicators suggest now may be an ideal time for an increased allocation to non-U.S. equities.

• International stocks are benefiting from strong earnings growth, cheaper valuations, a synchro.nized global expansion, and falling correlations.

• Taking an active approach to security selection can be a compelling way to pursue favorable returns when investing internationally.

The strong performance of U.S. stocks during the past several years has benefited numerous investors. However, it has also raised the level of risk in many portfolios. Due to the long-running popularity of U.S. stocks, many investor portfolios now have an extreme home-country bias (excessive allocation to domestic stocks). Overexposure to a single country or region creates concentration risk in a portfolio, leaving it vulnerable to a downturn in the region and underexposed to stronger performance in other parts of the world.

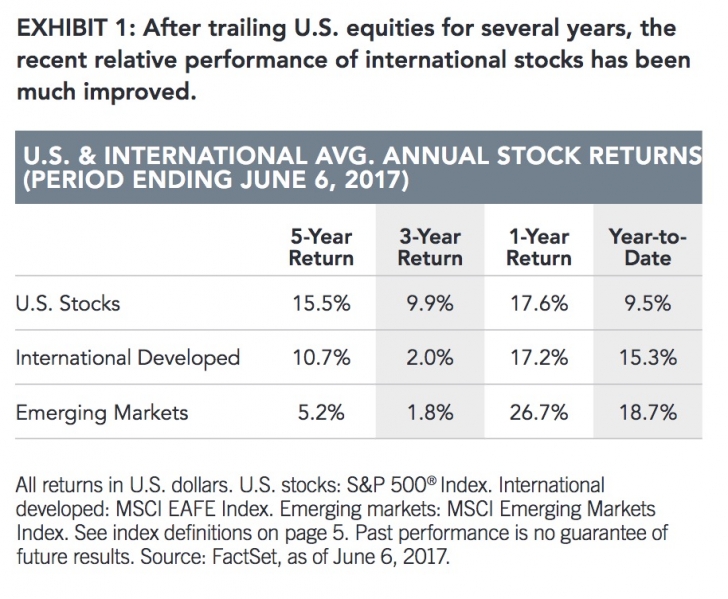

One way to help mitigate the risks of a home-country bias is to increase exposure to international stocks, and now may be an opportune time to do so. Many leading indicators suggest that the fundamental and cyclical dynamics for non-U.S. stocks have improved. In accordance, the earnings and stock prices for international companies have greatly improved during the past year (see Exhibit 1, page 2), and their valuations remain attractive relative to U.S. stocks.

Home-Country Bias, Explained

Home-country bias—the natural tendency of investors to be most attracted to investments in their home market— is not just a U.S. phenomenon. Investors around the world tend to favor the stocks of their home country.

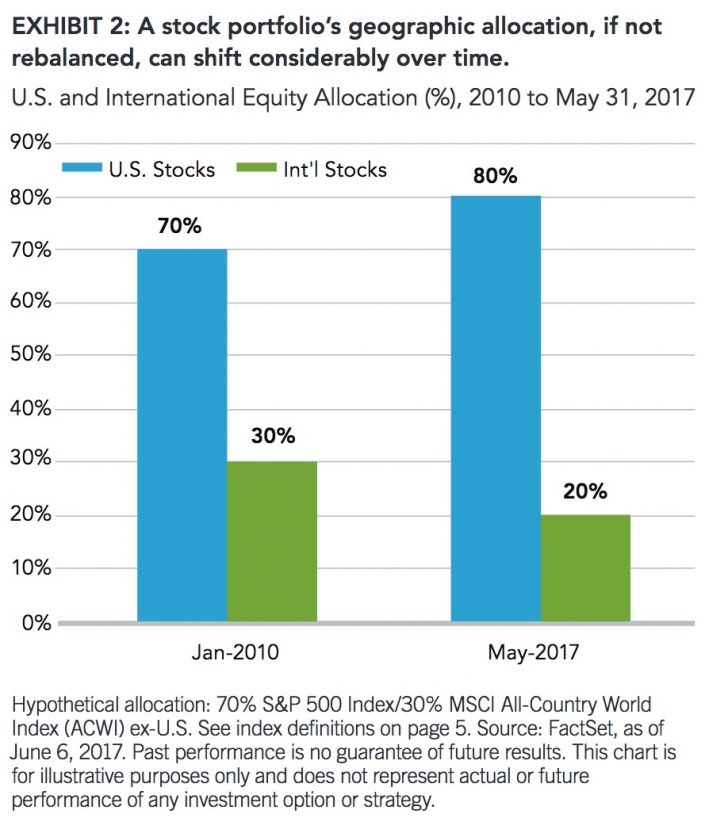

A home-country bias can develop from a conscious decision—an extreme form of “know what you own”— or it can develop unintentionally, as a result of market action. To illustrate the latter, imagine that a hypothetical equity allocation of 70% U.S./30% international stocks was constructed in January 2010 (roughly the start of the

U.S. outperformance cycle) and was left untouched (no investments in or out of the portfolio) during the seven-year U.S. rally. By May 2017, the portfolio would have lost a full one-third of its international exposure (from 30% international to 20%), based solely on the capital appreciation of U.S. vs. international stocks during that period (see Exhibit 2). This illustrates how an equity bias can develop unintentionally without a periodic rebalancing of one’s stock portfolio.

Although U.S. investors with a home-country bias may have done well in recent years, it’s crucial to understand that the performance leadership of domestic and international stocks has tended to be cyclical—one has historically outperformed the other for several years at a time. In fact, the average cycle of the out- or underperformance has been roughly seven years,1 which is about how long domestic stocks outperformed in this current cycle. Therefore, with the U.S. rally getting long in the tooth and leading indicators pointing toward improved prospects for non-U.S. equities, now may be an ideal time to consider an increased allocation to international stocks.

Why International Now?

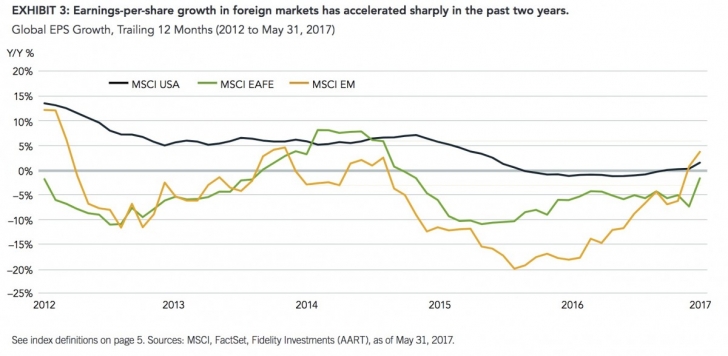

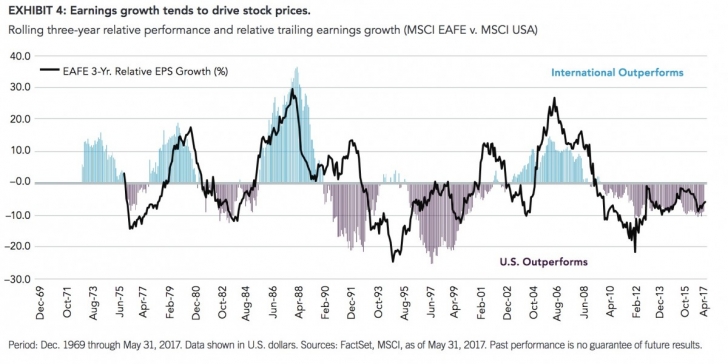

International earnings are climbing: International economies have shown renewed cyclical growth momentum relative to the U.S. since mid-2015. Accordingly, the gap in corporate earnings growth has also narrowed, making the cyclical outlook for international equities relatively more attractive after several years of underperformance (see Exhibit 3).

Attractive valuations: Price-to-earnings (P/E) ratios for both developed international and emerging-market equities remain attractive versus their history and relative to the U.S. market. According to MSCI, as of May 31, 2017, the MSCI USA Index was trading at 18x forward earnings, compared with only 15x for international developed stocks (MSCI EAFE) and 12x for emerging-market stocks (MSCI EM). The investment thesis is that by investing when a market is “cheap,” a subsequent reversion to average valuation can provide good upside.

Most synchronized global expansion in years: For the past 12 months, the global economy has been experiencing a relatively steady, synchronized expansion. Generally, most developed economies are in more mature (mid to late) stages of the business cycle, with the Eurozone not as far along as the United States. China’s improved cyclical trajectory has boosted many emerging economies and catalyzed a recovery in the global manufacturing, trade, and commodity industries.

Falling correlations may provide more active opportunities: During the past three decades, rising globalization coincided with an increase in global equity correlations. Recently, however, anti-globalization sentiment may be contributing to greater diversification benefits for international stocks. Lower correlations could further boost opportunities for active international equity managers, who seek to exceed benchmark performance over the long term by taking advantage of less-efficient markets.

Investment Implications/Conclusion

Exposure to international equities may help to reduce overall portfolio risk and dampen volatility through greater diversification and lower correlations among investments. Fidelity believes taking an active approach to security selection can be a compelling way to pursue favorable returns when investing internationally. And when it comes to reducing a home-country bias, there may be no time like the present to increase one’s allocation to stock markets overseas. Currently, the prospects for international stocks seem especially bright. Improved profits and low valuations have made foreign equities more attractive relative to U.S. stocks. The synchronized global expansion also provides a solid backdrop for international equities, and renewed cyclical growth overseas—combined with a maturing U.S. business cycle—suggests the gap in economic performance between the U.S. and the rest of the world has now disappeared.

So investors may want to check to see if their equity exposure needs to be rebalanced and, if so, consider an increased allocation to international stocks. It could make a “world” of difference in their portfolios.

Fidelity Thought Leadership Vice President Matt Bennett provided editorial direction for this article.

*****

For Canadian prospects and/or Canadian institutional investors only. Offered in each province of Canada by Fidelity Investments Canada ULC in accordance with applicable securities laws.

Endnotes

1 Based on rolling five-year relative performance between the S&P 500 Index and the MSCI All Country World ex USA Index.

Unless otherwise disclosed to you, any investment or management recommendation in this document is not meant to be impartial investment advice or advice in a fiduciary capacity, is intended to be educational, and is not tailored to the investment needs of any specific individual. Fidelity Investments and its representatives have a financial interest in any investment alternatives or transactions described in this document. Fidelity receives compensation from Fidelity funds and products, certain third-party funds and products, and certain investment services. The compensation that is received, either directly or indirectly, by Fidelity may vary based on such funds, products, and services, which can create a conflict of interest for Fidelity and its representatives. Fiduciaries are solely responsible for exercising independent judgment in evaluating any transaction(s) and are assumed to be capable of evaluating investment risks independently, both in general and with regard to particular transactions and investment strategies.

Information presented herein is for discussion and illustrative purposes only and is not a recommendation or an offer or solicitation to buy or sell any securities. Views expressed are as of June 23, 2017, based on the information available at that time, and may change based on market and other conditions. Unless otherwise noted, the opinions provided are those of the author and not necessarily those of Fidelity Investments or its affiliates. Fidelity does not assume any duty to update any of the information.

Investment decisions should be based on an individual’s own goals, time horizon, and tolerance for risk. Nothing in this content should be considered to be legal or tax advice and you are encouraged to consult your own lawyer, accountant, or other advisor before making any financial decision.

Stock markets, especially non-U.S. markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Foreign securities are subject to interest rate, currency exchange rate, economic, and political risks, all of which are magnified in emerging markets.

Investing involves risk, including risk of loss. Past performance is no guarantee of future results. Diversification and asset allocation do not ensure a profit or guarantee against loss.

Index performance includes the reinvestment of dividends and interest income. Securities indices are not subject to fees and expenses typically associated with investment funds. An investment cannot be made in an index.

Index definitions

Standard & Poor’s 500 (S&P 500®) Index is a market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent U.S. equity performance. S&P 500 is a registered service mark of The McGraw-Hill Companies, Inc., and has been licensed for use by Fidelity Distributors Corporation and its affiliates.

MSCI USA Index is a market capitalization-weighted index that is designed to measure the performance of the large- and mid-cap segments of the U.S. market.

MSCI Europe, Australasia, Far East Index (EAFE) is a market capitalization-weighted index that is designed to measure the investable equity market performance for global investors in developed markets, excluding the U.S. and Canada.

MSCI Emerging Markets (EM) Index is a market capitalization-weighted index designed to measure the investable equity market performance for global investors in emerging markets.

MSCI All Country World (ACWI) ex USA Index is a market capitalization-weighted index designed to measure large- and mid-cap stock performance across 22 of 23 developed-market countries and 23 emerging-market countries.

Third-party marks are the property of their respective owners; all other marks are the property of Fidelity Investments Canada ULC.

If receiving this piece through your relationship with Fidelity Institutional Asset Management® LLC (FIAM), this publication may be provided by Fidelity Investments Institutional Services Company, Inc., Fidelity Institutional Asset Management Trust Company, or FIAM, depending on your relationship.

If receiving this piece through your relationship with Fidelity Personal & Workplace Investing (PWI) or Fidelity Family Office Services (FFOS), this publication is provided through Fidelity Brokerage Services LLC, Member NYSE, SIPC.

If receiving this piece through your relationship with Fidelity Clearing and Custody SolutionsSM or Fidelity Capital Markets, this publication is for institutional investor or investment professional use only. Clearing, custody, or other brokerage services are provided through National Financial Services LLC or Fidelity Brokerage Services LLC, Members NYSE, SIPC.

Copyright © 2017 Fidelity Investments Canada ULC. All rights reserved. US: 797124.1.0 CAN: 816596.1.0