by Jeffrey Kleintop, Global Chief Investment Strategist, Charles Schwab & Co., Inc.

Key Points

- Over the past 15 years, earnings per share for both international and U.S. companies went from $33 to $108, but they took very different paths, illustrating the diversification benefits of global investing.

- Earnings of international companies exhibited greater sensitivity to economic growth and inflation, and experienced more varied economic conditions.

- A sharper upturn in the earnings growth of international companies may result if this year’s synchronized global economic upturn continues and if inflation revives.

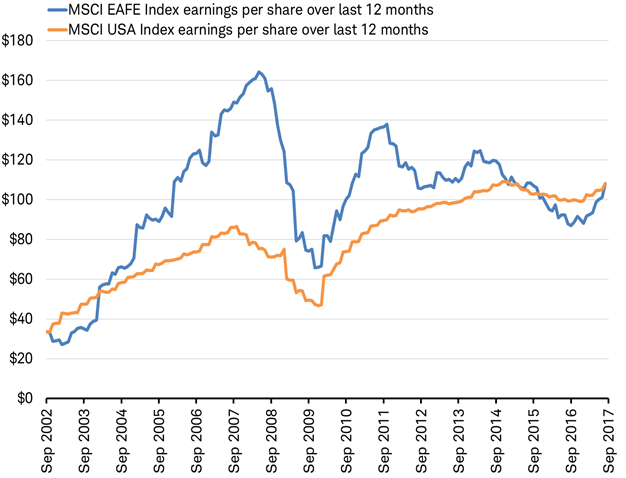

The saying goes: it is not the destination, it's the journey. This universal truth applies to corporate earnings. Earnings per share took very different paths for international (MSCI EAFE Index) and U.S.-based (MSCI USA Index) companies as they both went from $33 to $108 EPS over the past 15 years, as you can see in the chart below. Let's take a look at what these different paths of the past 15 years may tell us about the future for what has been the most important long-term driver of the stock market.

Same start and finish, but different paths for earnings

Source: Charles Schwab, Factset data as of 9/1/2017.

Why the different path?

While there are a great number of shared drivers of earnings of the global companies that make up the U.S. and international indexes, there are three important differences that have contributed to their unique paths:

- Earnings of international companies were more cyclical – The 2002-2008 global economic expansion fueled a dramatic rise in earnings for international companies in those six years (from $33 to over $160), then the global financial crisis resulted in a sharp drop back to about $60 in 2009, which was then followed by a powerful global economic rebound in 2010 to near $140. Earnings for U.S.-based companies moved in a similar direction, but the swings were only about half the magnitude.

- Earnings of international companies have been subject to more varied economic conditions – After the world economy rebounded from the financial crisis, individual economies began to get out of sync with each other. For international companies, the 2010 earnings rebound in was cut short by the 2011 Japan recession, the 2011 European debt crisis and 2012-13 European recession. A brief earnings rebound in late 2013 to early 2014 was again cut short by another recession in Japan and the 2015 oil-driven Canadian recession. In contrast, the U.S. economy experienced consistent, though below-average, economic growth over the same period, supporting less volatile earnings growth.

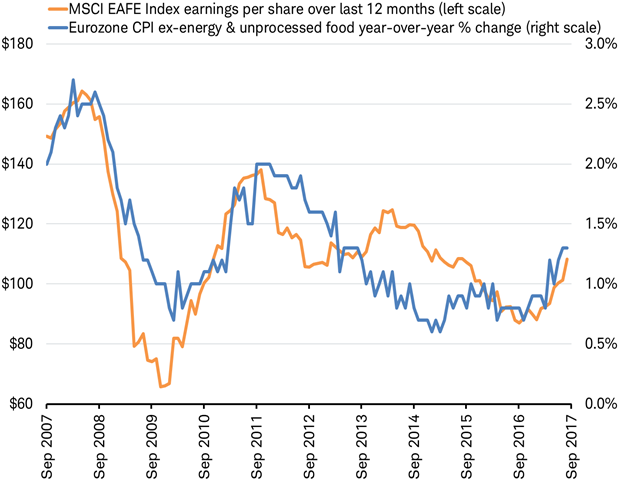

- Earnings of international companies have been much more sensitive to inflation – Even though inflation is embedded in both revenue and costs for business, the way it balances out is not always even. Earnings for international companies have tended to rise and fall with the pace of inflation, as you can see in the chart below.

Earnings for international companies tend to rise and fall with the pace of inflation

Source: Charles Schwab, Factset data as of 9/1/2017.

One important factor behind this connection between inflation and international company earnings is the financial sector is the biggest contributor to earnings for international companies while the information technology sector is the largest contributor to U.S. company earnings. Financial stocks are much more inflation sensitive than tech stocks.

The influence of inflation can also be seen in how international and U.S. stock markets behave—the U.S. stock market tracks the tech sector, while the 21-nation MSCI EAFE Index tracks a combination of three sectors: financials, industrials and materials (all three of them sensitive to the pace of inflation), as you can see in the charts below.

The performance of the MSCI USA Index tends to track the information technology sector

Measures total return from start of period.

Source: Charles Schwab, Factset data as of 9/1/2017.

The performance of the MSCI EAFE Index tends to track three inflation-sensitive sectors: Industrials, Materials and Financials

Measures total return from start of period.

Source: Charles Schwab, Factset data as of 9/1/2017.

Three takeaways

These three differences in the drivers of the relative earnings growth of international companies may offer us three takeaways on what we may expect going forward:

- A continuation of the globally-synchronized economic expansion taking place this year, with growth in all of the world's top 20 economies, may extend the sharper upturn in earnings for international companies seen so far in 2017.

- The potential exists for varied economic conditions to return which could weigh on the earnings of international companies. While broad global growth is widely expected by economists for 2018, there is the possibility that some economies may slip into recession or slow materially such as the United Kingdom given a potential Brexit-related stall in business investment and consumer spending.

- If inflation makes a return in the years ahead it may provide a greater boost to earnings of international companies. Alternatively, the return of the deflation would weigh more on the earnings of international companies.

Note that there is no mention of politics or monetary policy in the explanation of the fundamental differences in how earnings have evolved for U.S. and international companies over the past 15 years. It's not that these environmental factors haven’t mattered—it's that the differences across borders seem to have mattered much less than differences between the sectors that drive different stock markets. For example, the environment for tech companies inside the U.S. differs from that outside the U.S., but not by as much as the environment for tech differs from that of financials.

Stocks have tended to track earnings closely over the long-term. The decoupling and recoupling of earnings from $33 to $108 for both international and U.S. companies illustrates to us that there is no fundamental reason to favor one region over another for the long-term, but the different paths shows the diversification that can be obtained by owning stocks from many regions and highlights the potential for tactical shifts between regions.

Copyright © Charles Schwab & Co., Inc.