by Lance Roberts, Clarity Financial

As a portfolio manager, I start each morning by consuming copious amounts of a heavily caffeinated beverage and a data feed from a litany of web and blog sites. Over the last few days, as asset prices have set new records, there have been numerous articles on whether the market is currently in a bubble. Here are a few I grabbed from a Google search:

- Where’s The Next Bubble Forming In The Markets?

- How The ETF Bubble Feeds The Stock Market Bubble

- Market Entering A Bubble Zone

- U.S. Stock Market: Is The Bubble About To Burst

Well, you get the idea. First, like a “watched pot never boils,” bubbles occur when no one is looking for them. Bubbles are a function of greed running rampant combined with a mass hypnotic state the current ride will never end. The shear fact that multitudes of articles are being written about “market bubbles” is a sign that we are likely not there…just yet.

However, as a shot of caffeine hits my brain, I read with interest a WSJ article entitled “Tech Is No Bubble, But The Market Might Be” which I have summarized for you:

- Technology stocks have finally surpassed the 17-year old peak.

- 80% of the gains in the technology sector has come from just 8-companies.

- A measure of dispersion in performance shows little excess from the long-run average.

- While there may be an “everything bubble,” technology stocks don’t look especially frothy.

While these are certainly some interesting arguments, the comparison between now and the turn of the century peak is virtually meaningless. Why? Because no two major market peaks (speculative bubble or otherwise) have ever been the same.

Let me explain.

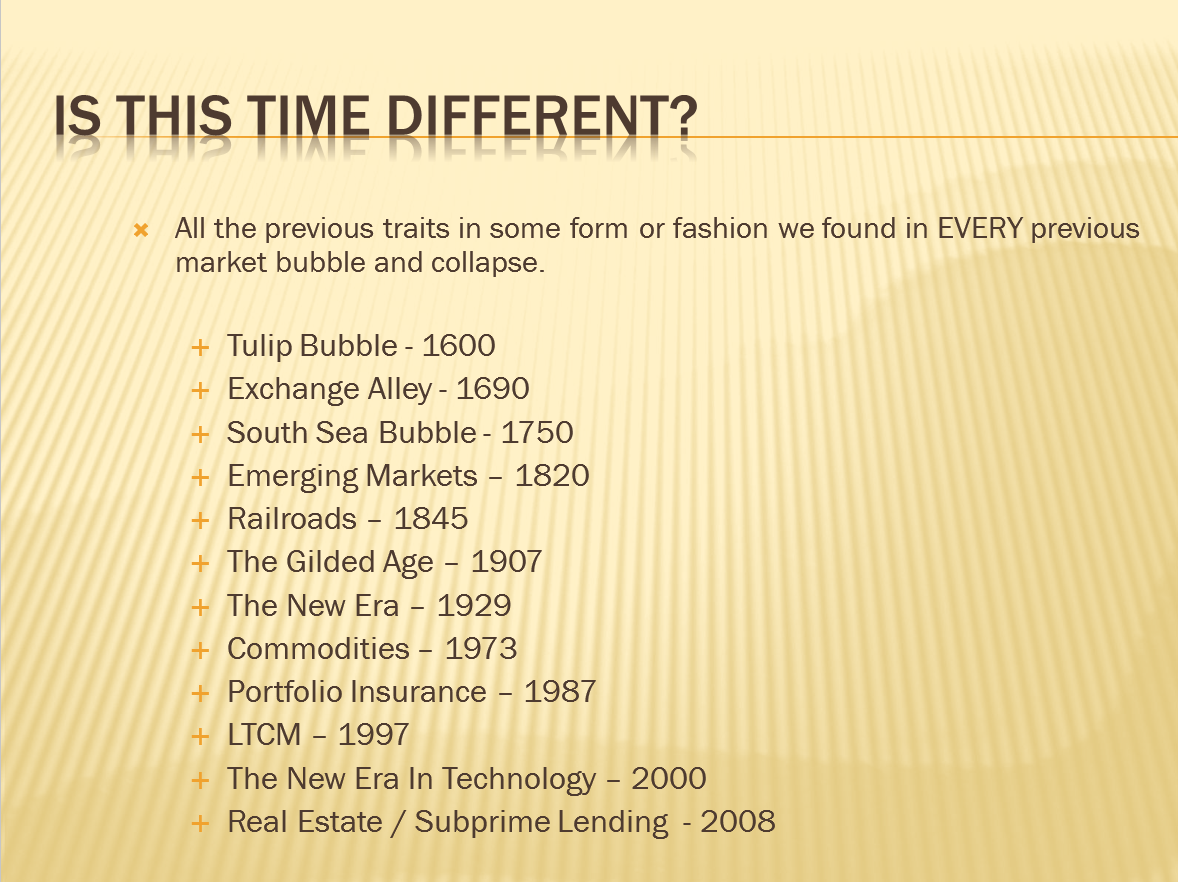

In late October of 2007, I gave a seminar to about 300 investors discussing why I believed that we were rapidly approaching the end of the bull market and that 2008 would likely be bad…really bad. Part of that discussion focused on market bubbles and what caused them. The following two slides are from that presentation:

Every major market peak, and subsequent devastating mean reverting correction, has ever been the result of the exact ingredients seen previously. Only the ignorance of its existence has been a common theme.

The reason that investors ALWAYS fail to recognize the major turning points in the markets is because they allow emotional “greed” to keep them looking backward rather than forward.

Of course, the media foster’s much of this “willful” blindness by dismissing, and chastising, opposing views generally until it is too late for their acknowledgement to be of any real use.

The next chart shows every major bubble and bust in the U.S. financial markets since 1871 (Source: Robert Shiller)

At the peak of each one of these markets, there was no one claiming that a crash was imminent. It was always the contrary with market pundits waging war against those nagging naysayers of the bullish mantra that “stocks have reached a permanently high plateau” or “this is a new secular bull market.” (Here is why it isn’t.)

Yet, in the end, it was something that was unexpected, unknown or simply dismissed that yanked the proverbial rug from beneath investors.

What will spark the next mean reverting event? No one knows for sure, but the catalysts are present from:

- Excess leverage (Margin debt at new record levels)

- IPO’s of negligible companies (Blue Apron, Snap Chat)

- Companies using cheap debt to complete stock buybacks and pay dividends, and;

- High levels of investor complacency.

Either individually, or in combination, these issues are all inert. Much like pouring gasoline on a pile of wood, the fire will not start without a proper catalyst. What we do know is that an event WILL occur, it is only a function of “when.”

The discussion of why “this time is not like the last time” is largely irrelevant. Whatever gains that investors garner in the between now and the next correction by chasing the “bullish thesis” will be wiped away in a swift and brutal downdraft. Of course, this is the sad history of individual investors in the financial markets as they are always “told to buy” but never “when to sell.”

For now, the “bullish case” remains alive and well. The media will go on berating those heretics who dare to point out the risks that prevail. However, the one simple truth is “this time is indeed different.” When the crash ultimately comes the reasons will be different than they were in the past – only the outcome will remain same.

Copyright © Clarity Financial