by Leon Roisenberg, Vice President, Equity Applied Research, MSCI

In constructing portfolios, asset managers expose the portfolio to factor tilts that greatly influence fund performance. Some of these exposures, which can provide sources of excess return, may be intentional but others may not. A manager who makes the wrong bet could be on the wrong side of history.

To what extent do factor exposures affect performance, and which factors have had the greatest impact?

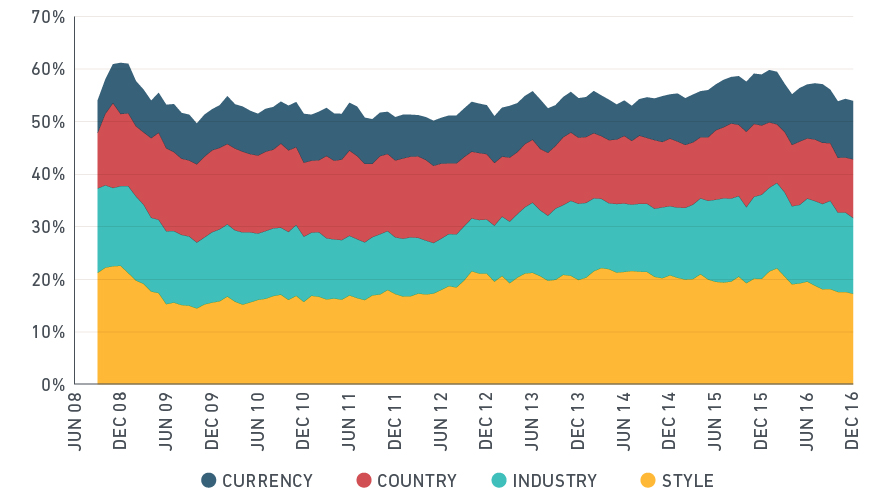

Using MSCI’s Peer Analytics dataset, we examined the composition and performance drivers of active global funds through the lens of our Global Total Market Equity Model. Our key finding: Exposure to common factors (the sum of the four groups in the below exhibit) accounted for 55% of funds’ 5-year active performance vs. 45% for stock-specific contributions during a 13-year period.

Factor groups explain 55% of funds’ performance

Mean absolute contribution fraction of total active return by factor group

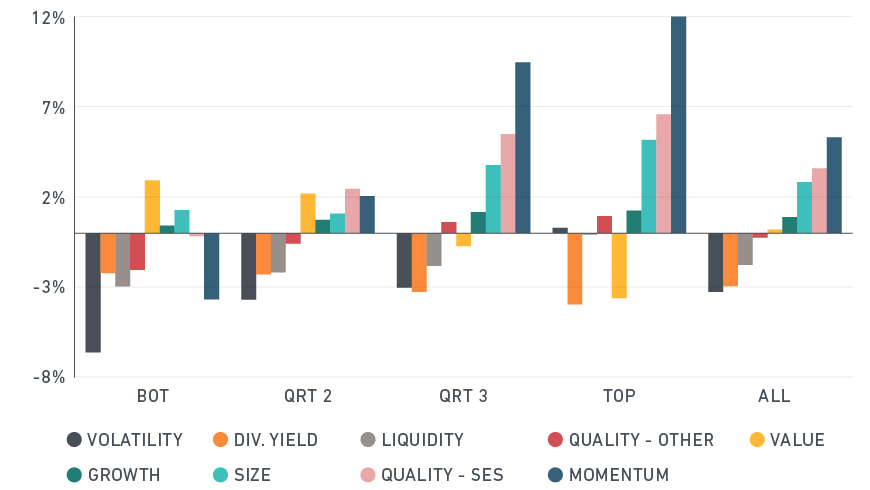

Among factor groups, exposure to style factors (in yellow) was the largest contributor, accounting for 19% of total active return. Within style factors, Systematic Equity Strategies (SES) — rules-based strategies that have generated excess returns over long time periods — explained 54% of contributions. When we peel the performance onion further, we find that Price Momentum, Residual Volatility, Beta, Dividend Yield and Profitability were the most significant individual factors.

Which factors provided the greatest contributions to performance?

Mean factor contribution fraction of total style contribution from individual factors for all funds and by performance quartile.

Unintended exposures also had a significant impact. For value managers, contributions from volatility, momentum and profitability factors accounted for 19%, 18% and 17%, respectively, of the total style contribution, exceeding that of the value factor itself (15%).

Finally, we found that use of style-consistent benchmarks, such as MSCI Factor Indexes, may provide a clear picture of how much of performance comes from factors versus stock contributions. This information may help asset managers address potential benchmark mismatches.

These findings underscore the importance of monitoring the contribution of common factors to fund performance in maintaining alignment with managers’ mandates and managing crowding risk.

Further reading:

Anatomy of Active Portfolios: How Factor Exposures Affect Fund Performance

Using Systematic Equity Strategies

What factors are more time-sensitive?

Copyright © MSCI