Diversify your income portfolio with senior loans

by Christopher Doll, Vice President, Head of Product & Business Strategy, PowerShares Canada, Invesco Canada

In today’s low-yield environment, fixed-income returns are uninspiring. Many advisors are looking to diversify beyond traditional fixed-income asset classes, and senior loans are an attractive floating-rate option for some investors.

Today’s environment

Canadian corporate spreads have come down considerably since highs reached in February 2016 and are now sitting below 10-year averages. U.S. high-yield spreads have also come down during this time and are now below historic averages.1 In today’s low-yield world, investors are hungry for income and demand is outpacing supply – leading to a tightening of credit spreads. However, with mixed economic signals, weaker cash-flow fundamentals and political uncertainty across the globe, we may be entering a period in which we see spreads widening in the high-yield space. Generally speaking, widening credit spreads indicate growing market concern about the borrowers’ ability to service their debt. Narrowing credit spreads therefore indicate improving creditworthiness.

Currently, high-yield to bank loan spreads are tight, potentially favouring senior loans – high-yield spread over senior loans is now less than 1%. In addition, we’re seeing corporate balance sheets in the U.S. levering up again, as demonstrated by net debt/EBITDA (earnings before interest, tax, depreciation and amortization) data, as well as interest coverage ratios weakening. Profit margins are significantly weaker due to wage growth and the cost of interest, while delinquency rates are rising.1

With this as the backdrop, there is a strong case to be made for taking a more defensive stance with your high yield allocations by employing the potential benefit of senior loans.

Getting to know senior loans

Senior loans provide an attractive yield per year of duration – the underlying yield for each year of duration risk taken on. Duration risk is the sensitivity of a bond’s price to a one percent change in interest rates – the higher a bond’s duration, the greater its sensitivity to interest rates changes.

For example, as of May 31, 2017, the S&P/LSTA U.S. Leveraged Loan 100 Index, the underlying index for PowerShares Senior Loan Index ETF (BKL), provides a yield-to-maturity2 of 4.38% on a duration of 0.08 years, meaning roughly 54.75 % of yield per year of duration.3 By comparison, the FTSE TMX Canada Universe Bond Index offers 1.88% on a duration of 7.49 years, resulting in 0.25% yield per year of duration.4 These numbers represent the potential yield available to an investor for a given level of interest-rate risk – the higher the yield per year of duration, the less interest-rate risk an investor is required to take on to get more yield potential.5

What these numbers illustrate is the attractive yields that senior loans have provided despite lower spreads. Comparing these numbers to those for higher-yield bonds, where spreads are wider and yields have been higher, senior loans still come out on top. For example, the BofA Merrill Lynch US High Yield Bond Index yields 5.54% on a duration of 3.68 years, resulting in a much lower 1.51% yield per year of duration.1 Not only do senior loans provide attractive yields, but they also help avoid the interest-rate risk that high-yield bonds can present.

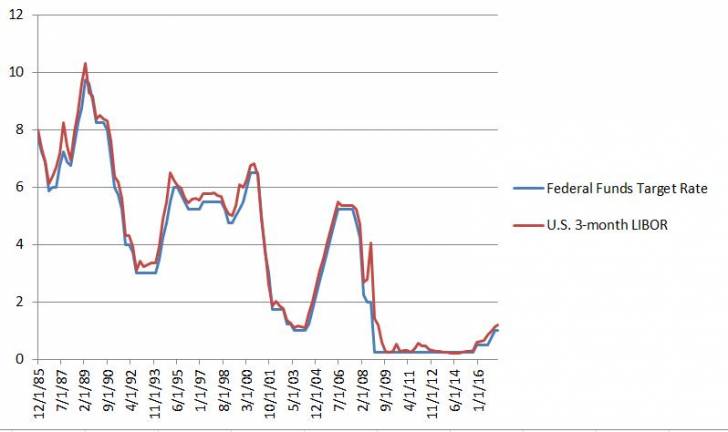

Senior loans and LIBOR

The reference rate for senior loans, 3-month LIBOR (London Interbank Offered Rate), continues to rise and currently sits at 1.21%.1 The U.S. Federal Reserve (Fed) raised rates June 14, 2017 for the fourth time since December 2015, with a final hike expected by the end of 2017. Historically, the Fed Funds rate and LIBOR have been highly correlated, so in my opinion, we expect LIBOR to track higher over the course of this year. As a result, the loan coupons on senior loans would then reset higher over the next few quarters.

Credit quality and default rates

Credit quality has improved in the senior loans space over the past year as U.S. corporate profitability expectations have risen and some issuers have been able to refinance their loans at lower interest rates and improve their balance sheets.2

Defaults in the senior loans space continue to remain very low. The default rate for S&P/LSTA U.S. Leveraged Loan Index fell to a 16-month low of 1.29% in May 2017. As a comparison, the U.S. speculative-grade corporate default rate was 3.6% in May 2017.6 This data highlights the improving credit quality and benign default rates that senior loans should benefit from over the remainder of the year.

Taking advantage of senior loan opportunities

With tighter spreads and lacklustre returns in the fixed-income market, senior loans can provide an opportunity for investors to diversify their fixed-income portfolios. These floating-rate loans can provide attractive yield-per-duration, LIBOR upside and strong credit metrics, which means an investment in this space can give people strong income potential, along with a measure of defense against rising interest rates. This can be a very attractive combination in today’s uncertain markets.

PowerShares Canada offers both hedged and unhedged exposure to the senior loans market with three TSX-listed ETFs.

PowerShares Senior Loan Index ETF – CAD hedged (BKL.F)

PowerShares Senior Loan Index ETF – CAD (BKL.C)

PowerShares Senior Loan Index ETF – USD (BKL.U)

This post was originally published at Invesco Canada Blog

Copyright © Invesco Canada Blog