by Burt White, Chief Investment Officer, LPL Financial

KEY TAKEAWAYS

- Fourth quarter earnings season has not been a blowout by any stretch, but growth has been solid and puts the earnings recession further in the rear view mirror.

- Potential policies out of Washington, D.C. have dominated discussions, but there have been many other things to discuss, including resilient guidance, strong profit margins, and noteworthy results from the financials and industrials sectors.

Earnings update: Five Observations

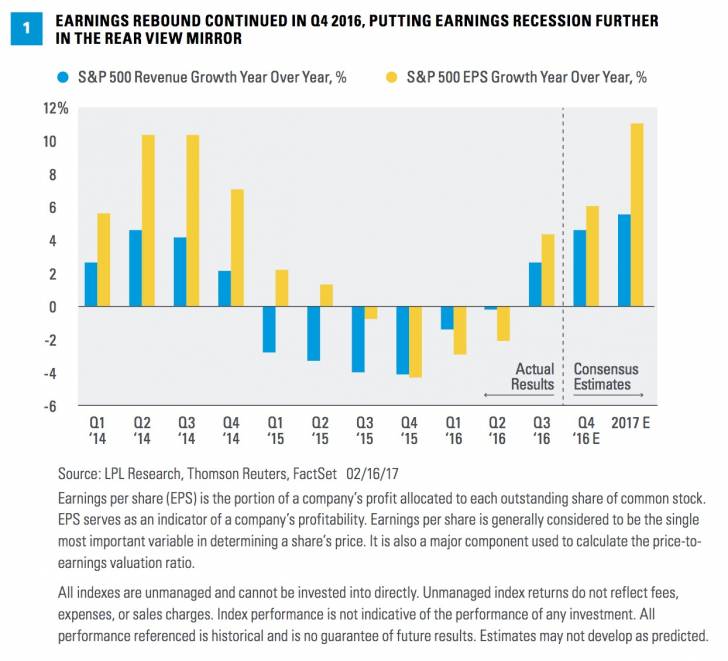

Fourth quarter earnings results are mostly in the books. It was not a blowout quarter by any stretch — earnings growth is tracking to about 7.5%, according to Thomson Reuters, only a below-average 1.5% improvement on the estimate at the start of the reporting quarter. But 7.5% earnings growth, along with 5% revenue growth, is nothing to sneeze at [Figure 1]. Further, policy optimism on Wall Street and among corporate management has helped full-year estimates for 2017 hold up relatively well. This week, we share five observations about fourth quarter earnings season so far.

Five key observations

Observation #1: Policy Talk Abounds

Market participants have been focused on the implications of a Trump presidency since Election Day. That focus has not changed during earnings season, with tax policy dominating discussions on earnings conference calls. In fact, of the first 317 S&P 500 companies that reported, tax policy was mentioned on 85 of the earnings calls [Figure 2]. Regulation — of particular interest for financials — and trade policy have also garnered a lot of attention. These policies have the greatest potential to influence broad earnings, while the rest of the topics in Figure 2 are either more sector specific or more likely to have only a small impact.

We still lack clarity on what tax reform and other policies out of Washington will look like. But the latest headlines out of Washington and actual earnings results have given us no reason to change our belief that policy changes may add meaningfully to earnings growth once implemented. The latest stock market gains are likely pricing in some of this policy impact, with the forward S&P 500 price-to-earnings ratio (PE) over 17. We may start seeing the impact of policy changes on earnings as early as late 2017, but any potential earnings boost is more likely to come in 2018. Estimates vary widely, but we believe an expectation of a 3-5% lift from tax reform, infrastructure spending, and deregulation is reasonable.

Observation #2: Guidance Has Generally Been Resilient

With more than 80% of S&P 500 companies having reported through February 17, 2017, S&P 500 estimates for 2017 have only fallen about 1.5%, according to Thomson Reuters data. Estimates are now calling for an 11% year-over-year increase, down from 12.5% as of January 1, 2017. On average, estimates fall between 2% and 3% during earnings season. The below-average reduction is an encouraging sign for growth. Looked at another way, a negative-to-positive preannouncement ratio of 2.4 for the first quarter is better than the long-term average (post-1990) of 2.7.

The leading economic indicators we watch, including the Conference Board’s Leading Economic Index (LEI) and the Institute for Supply Management’s (ISM) Purchasing Managers’ Indexes (PMI), are also sending positive signals and support our forecast for a mid- to high-single-digit increase* in S&P 500 earnings in 2017. Should our forecast prove accurate, it would miss the January 1 estimate by 4-5%, much better than the long-term average of 8-9% (post-1985 based on Ned Davis data).

*We expect mid-single-digit returns for the S&P 500 in 2017 consistent with historical mid-to-late economic cycle performance. We expect S&P 500 gains to be driven by: 1) a pickup in U.S. economic growth partially due to fiscal stimulus; 2) mid- to high-single-digit earnings gains as corporate America emerges from its year-long earnings recession; and 3) an expansion in bank lending; and 4) a stable price-to-earnings ratio of 18 – 19.

Observation #3: Wage Pressures Yet to Impact Profit Margins

Many have been warning about profit margin compression for the past few years based on mean reversion (excess profits bringing in competition, which can pull margins down) and on expected wage increases as the labor market tightens. Although corporate America has seen some profit margin compression since the highs two years ago, all of it can be attributed to the energy downturn. According to FactSet data, S&P 500 operating margins have fallen from a multi-decade high of 14.6% in the fourth quarter of 2014 to the latest reading of 13.7% for the fourth quarter of 2016. During this period, energy sector operating margins have fallen from about 12% to zero, essentially accounting for all of the compression at the S&P 500 level [Figure 3]. The energy sector is unlikely to return to the margins produced at $100/barrel oil prices anytime soon, if ever, but the sector should be able to recover at least half of the recent margin compression should oil prices stay in the $50s or higher, as we expect.

It is reasonable to expect profit margin compression from record highs as the economic cycle matures and wages, corporate America’s biggest cost line item, accelerate. Based on the U.S. Bureau of Labor Statistics’ measure of wage growth (average hourly earnings), wage inflation slowed from 2.8% in December 2016 to 2.5% in January 2017. That pace of wage inflation and steady job gains (an average of 195,000 jobs added over the past 12 months) are enough to support two or three rate hikes from the Federal Reserve (Fed) this year but are putting little pressure on corporate profit margins thus far.

Observation #4: Financials (Mostly) Shine

Financials were the clear winner through the first month of earnings season, having generated the fastest growth, at over 20%, and the most upside, at over 5%. The environment has been favorable for banks with a steepening yield curve (long-term interest rates rising more than short-term rates) and a pick-up in economic activity. Strong stock market gains, healthy credit markets, and robust trading activity have boosted capital markets firms. But a sharp decline in financials’ earnings last week (February 13-17, 2017) due to a large reserve taken by a property and casualty insurer culled a lot of the sector’s growth, and all of the upside [Figure 4]. The insurer-driven weakness does not take away from the double-digit earnings gains delivered in the quarter by banks and capital market firms, which make up the bulk of the sector.

Estimates for financials have also been among the most resilient during earnings season, reflecting the favorable environment noted above and prospects for deregulation.

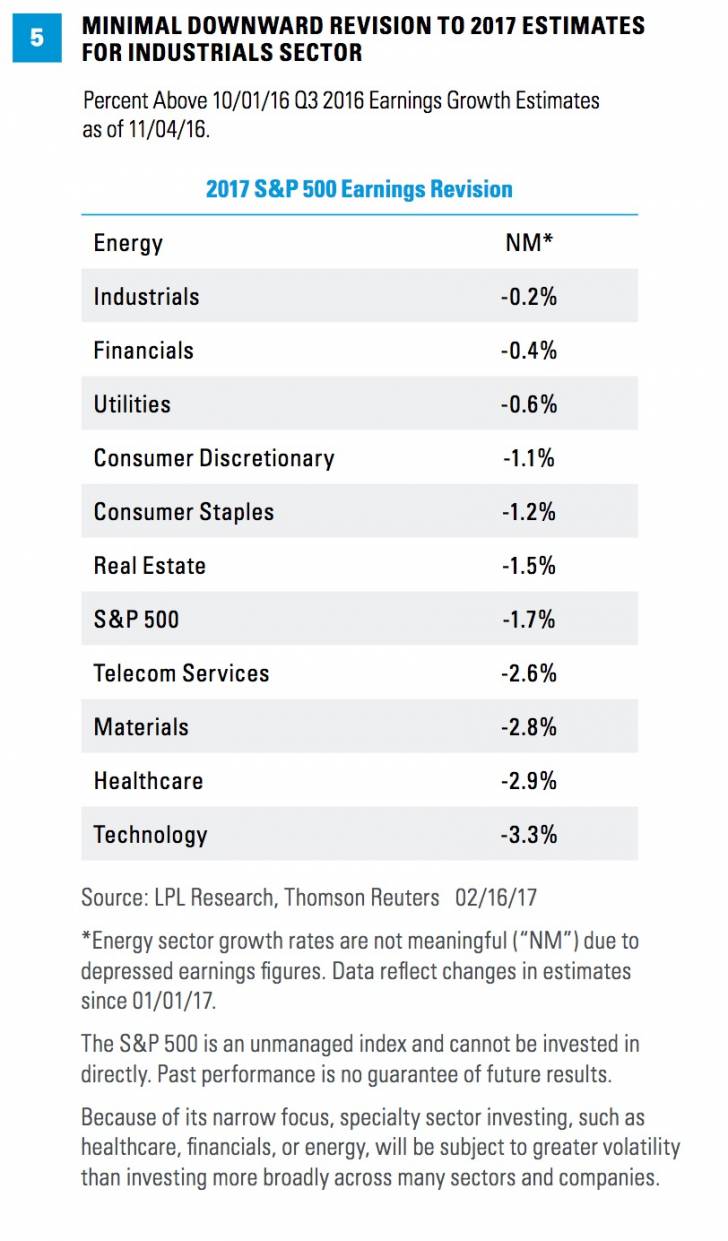

Observation #5: Industrials Expectations May Have Gotten Too Low

The industrials sector has struggled with low growth rates, shortfalls relative to expectations, and reductions in guidance over the past year or so. The sector has been a victim of the two biggest drags on earnings during this time: the strong U.S. dollar and the oil downturn. These two drags have reversed meaningfully, which may have finally enabled the industrials sector, with its significant commodity-sensitive businesses and high overseas exposure, to finally meet its growth expectations.

The upside the sector has generated during earnings season (2.7%) is solid, but perhaps more impressive is that first quarter 2017 estimates for the sector have risen 2.1% since January 1, 2017, while sector estimates for all of 2017 have hardly budged [Figure 5]. We believe this resilience reflects overly pessimistic expectations and optimism surrounding a potential infrastructure spending program later this year or in 2018.

Conclusion

Fourth quarter earnings season has not been a blowout by any stretch, but growth rates have been solid and have put the earnings recession further in the rear view mirror. Although much of the talk has been about potential policies out of Washington, D.C., there have been many other things to discuss, including resilient guidance, strong profit margins, and noteworthy results from the financials and industrials sectors. Look for more on earnings from us in our Corporate Beige Book commentary in two weeks on March 6, 2017.

*****

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

All investing involves risk including loss of principal.

Forward price-to-earnings is a measure of the price-to-earnings ratio (PE) using forecasted earnings for the PE calculation. While the earnings used are just an estimate and are not as reliable as current earnings data, there is still benefit in estimated PE analysis. The forecasted earnings used in the formula can either be for the next 12 months or for the next full-year fiscal period.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Leading Economic Index is a monthly publication from the Conference Board that attempts to predict future movements in the economy based on a composite of 10 economic indicators whose changes tend to precede changes in the overall economy.

The U.S. Institute for Supply Management (ISM) Purchasing Managers’ Index (PMI) is an economic indicator derived from monthly surveys of private sector companies, and is intended to show the economic health of the U.S. manufacturing sector. A PMI of more than 50 indicates expansion in the manufacturing sector, a reading below 50 indicates contraction, and a reading of 50 indicates no change.

Copyright © LPL Financial