by Jeffrey Saut, Chief Investment Strategist, Raymond James

“Unseasonably mild and clearing,” was the weather forecast going into the Ides of March back in the year of 1888. And it was true, as temperatures hovered in the 40s and 50s along the East Coast. However, torrential rains began falling, and on March 12th the rain changed to heavy snow, temperatures plunged and sustained winds of more than 50 miles per hour blew. The “Great White Hurricane” had begun! In the next 36 hours some 50 inches of snow would blanket New York City and the winds would whip that snow into 40- to 50-foot snowdrifts. Telegraph and telephone lines were snapped, fire stations were immobilized, New Yorkers could not get out of their homes, 200 ships were blown aground, and before the storm was over 400 people would die. The resulting transportation crisis led to the construction of New York's subway system.

We revisit the Great Blizzard of 1888 this morning because of the weather that has crippled the Northeast corridor beginning last Thursday. Actually, I guess it was on Wednesday the storm hit because my friend and VE Capital portfolio manager Eric Kaufman’s plane was canceled early Thursday morning on his way to Orlando to speak at the Money Show and then spend some time with us here in Saint Petersburg. I didn’t see the final tally, but NYC was expecting a foot of snow and Boston was slated to get even more. Fortunately, communities are more capable of dealing with such storms today than they were more than a century ago.

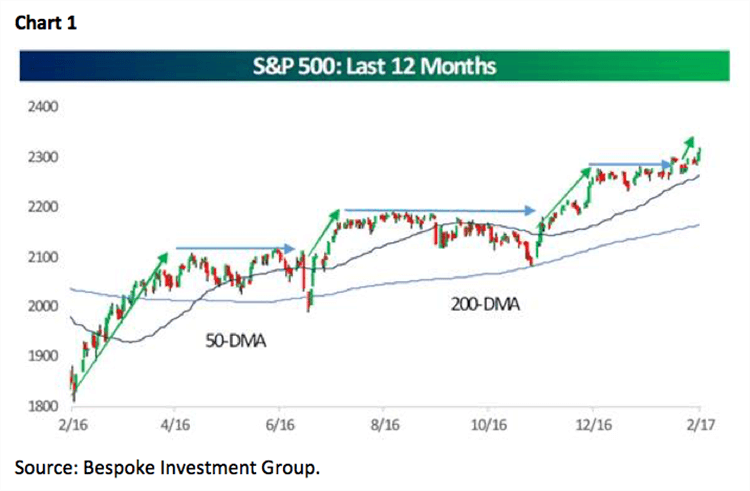

I remember the big snow storm that “stopped” NYC in February 1978 when Central Park saw an accumulation of some 18 inches and the trading on the NYSE was impacted. This time trading was not nearly as impacted as the S&P 500 (SPX/2316.10) traded decent volume and rose from Wednesday’s closing price of roughly 2289 to Friday’s close of ~2316, trading to a new upside break-out high (Chart 1). Plainly this flies in the face of what our short/intermediate-term models were suggesting since they “looked” for a downside window of vulnerability in late January, or early February. The catalyst du jour for the nearly +1.2% two day two-step once again appeared to be vibes emanating from the D.C. beltway and the White House. To wit, DJT told airline executives, “Lowering the overall tax burden on American business is big league . . . that's coming along very well. We're way ahead of schedule, I believe. And we're going to announce something I would say over the next two or three weeks that will be phenomenal in terms of tax.” That announcement reversed worries that President Trump’s tax agenda was going to get lost in the “Washington Shuffle.” To reiterate, as Andrew and I have stated repeatedly, “DJT’s bark is worse than his bite.” We have written about this many times in that his background is in real estate. For example, say you put your house on the market for $1,000,000 and someone offers you $800,000. Your response would likely be, “Okay, how about $950,000” – the counter offer might be $850,000 – as the two of you negotiate toward the “middle.” That, dear readers, is DJT business model. Just think back to President Trump’s terse rhetoric regarding Japan a few months ago. Now the Trumps, and Japan’s Abes, are best friends enjoying life at the Florida White House. Indeed, DJT’s “bark is worse than his bite!”

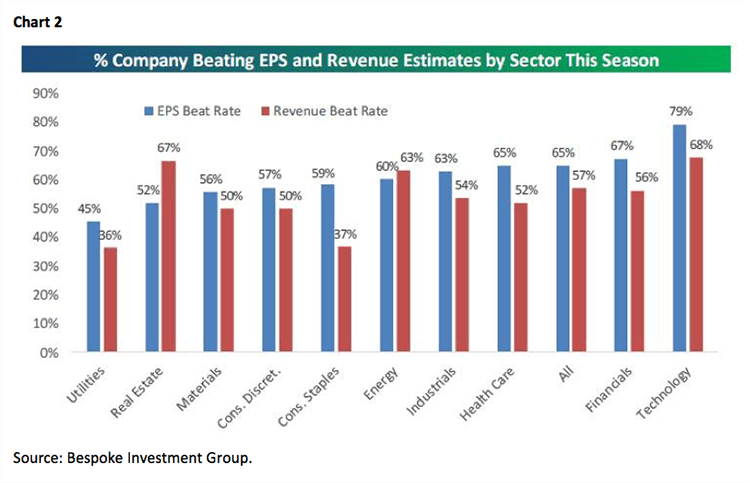

So what does all of this mean? Well, earnings continue to come in on the brighter side (as we expected) with 65% of reporting companies beating consensus estimates. Meanwhile, revenues are besting estimates by 57% reinforcing our belief the equity markets are transitioning from an interest rate, to an earnings driven, secular bull market. According to Thomson, “Fourth quarter earnings are expected to increase 8.4% from Q4 2015. Excluding the Energy sector, the earnings growth estimate improves to +8.6%.” As for sectors beating both earnings and revenue estimates, they are fairly consistent with those sectors emphasized in these reports. To that point our friends at the Bespoke organization write:

Technology and Financials — the two largest sectors of the market — have the strongest earnings beat rates, and they’re the only two sectors with stronger readings than the overall beat rate of 65%. Consumer Discretionary and Materials are the two cyclical sectors with the weakest earnings beat rates. In terms of revenues, Technology has the highest beat rate, while Consumer Staples and Utilities have the lowest.

That is consistent with our strategy over the past six months in that we have liked Technology and the Financials and have believed the “low volatility/defensive sectors” were overvalued (see Chart 2).

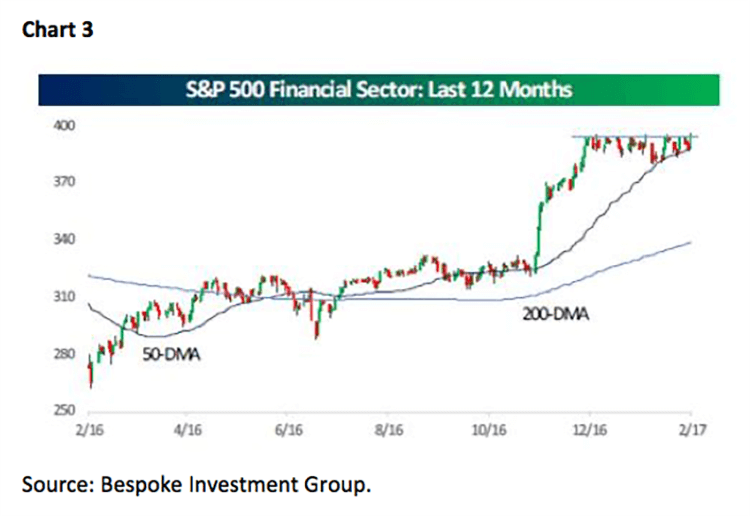

If you do not want to adopt our more cautionary near-term trading stance, we would point you to the “triple plays” (companies that beat earnings/revenue estimates, raised guidance, screen well on our models, and are favorably rated by our fundamental analysts) that have been featured in recent missives. Also for your consideration should be the Financial sector, which looks to have broken out to the upside (Chart 3).

While our models have not been correct recently, we have not given up on them since they have been generally correct for a long time. In point of fact, our short-term model is suggesting a trading top is currently occurring. Meanwhile, last week’s market move happened as Andrew and I received numerous emails from financial advisors telling us the equity markets are involved in a “melt up.” Ladies and gentlemen, that has historically been a worrisome sign. If our models prove to be wrong, we will adjust. However, we continue to adhere to those models and the market mantra, “The first objective of investing is to do no harm!”

The call for this week: There were a lot of positive things that came together last week in addition to the president’s “phenomenal in terms of tax [policy]” statement. The Fed’s Bullard said interest rates can remain low through 2017, oil prices rebounded on stronger consumer and labor numbers, and China praised our president for wanting a “constructive relationship.” This week’s attentions will probably focus on the comments from a plethora of Fed speakers including two trips to Capitol Hill by Janet Yellen. Those comments could cause some market consternations, as could some of these observations about last week’s action: the FANGs did not leap, Friday saw the first hour of trading to the upside and the last hour to the downside from the session’s highs, Syria’s Assad told news sources that some refugees are definitely terrorists, Pat Buchanan told the president that he needs to break judicial power calling for Congress to start using Article III, Section 2 (https://www.law.cornell.edu/constitution/articleiii), and then there was this from the always insightful Jason Goepfert (SentimenTrader):

The rally's meek underpinnings. Stocks have rallied strongly over the past three months, but there have been few breadth thrusts. The S&P 500 has enjoyed a 65-day, 10% gain to new highs, but there have been only two days during that stretch that would qualify as a thrust. That's the weakest such rally since 1999.

Our models continue to suggest that it is unlikely this is going to be the beginning of a whole new up leg for the S&P 500. In fact, our models telegraph that the maximum upside from here for the SPX is 2330. That said, they also suggest no big downside collapse either.

PS: From The King Report, “In the current environment, it is dangerous to forecast beyond a few hours because a DJT tweet or pronouncement can occur at any moment. However, barring the appearance of new dynamics in the interim, the grand unveiling of DJT’s tax plan should generate some type of stock market peak.

Copyright © Raymond James