by Joachim Klement, CFA, CFA Institute

“Past performance is no guarantee of future results” is a maxim every investor knows by heart. It has been repeated so often, no investor would base the selection of stocks or funds on past performance alone, right? Wrong.

There have been numerous studies that show investors are more inclined to buy equities that have gone up in price than those that have declined.

In the mutual fund world, individual fund investors tend to buy funds that have had good performance relative to their peers and to sell funds with bad absolute performance, according to a study by Zoran Ivkovic and Scott Weisbenner.

Don’t Just Sit There, Do Something!

But sophisticated investors couldn’t possibly be as “dumb” as individual investors, right? Wrong again.

Pension funds and other institutional investors have teams of fund selectors to help identify the best-in-class funds for every investment style or asset class. And these highly paid experts should certainly be able to select the better performing funds within each peer group.

The problem is that while expert fund selectors have more tools at their disposal and spend more time analyzing funds, they are also under pressure to justify their fees and salaries. It doesn’t sit too well with trustees if an adviser does all this work and then concludes that nothing needs to be changed — especially when a fund is underperforming.

A prolonged period of underperformance leads to increased pressure to not just sit there but to do something, and this pressure can eventually become the dominating factor driving decisions to fire and hire mutual fund managers.

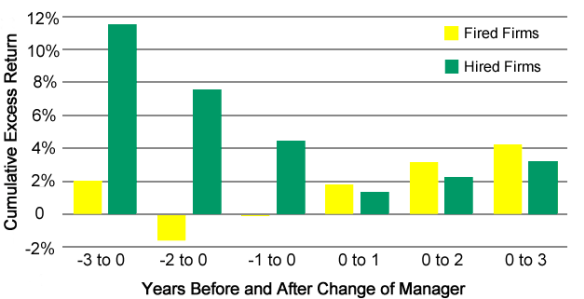

Amit Goyal and Sunil Wahal documented this effect in institutional investor portfolios. Their major finding is so impressive that it is reproduced below.

In the years before fund managers are fired, they underperform their benchmarks, while newly hired manager outperform their benchmarks by wide margins. Once managers have been fired and new ones hired, however, this outperformance disappears. In fact, the fired managers on average tend to outperform newly hired managers in the three years after a change.

This is not to mock the investment consultant industry. I am guilty of these charges myself. In my previous incarnation as an investment consultant, I can remember several instances when performance pressure translated into an increased impetus to replace a good manager. And in another role as a portfolio manager, I came under tremendous pressure once performance was weak for more than a year. These experiences taught me a lot about career risk and frustrated me enough to write an academic paper on the topic that will soon be published in the Journal of Behavioral Finance.

Pick the Dogs Not the Stars

The above results indicate that, in practice, it might be better to pick past losers rather than past winners when selecting funds. If fund performance is mean reverting, then it might be a good strategy to select funds with several years of underperformance instead of funds with several years of outperformance.

The profitability of such a strategy was recently explored by Bradford Cornell, Jason Hsu, and David Nanigian. In what I call the “Dogs of Morningstar” strategy, they selected the funds in the commonly used Morningstar database that were in the bottom decile in terms of three-year performance and compared the performance of this group of funds to those in the top decile. In the subsequent three years, the funds in the bottom 10% outperformed the funds in the top 10% by more than 2%. Even the average funds outperformed the top decile funds.

There are several lessons investors can learn from this.

Cornell and his colleagues recommend putting more emphasis on fund selection criteria that have a proven track record of identifying superior funds ex ante. But there is also a dumb alpha technique here. Instead of being motivated by the rule “Don’t just sit there, do something,” investors might instead act based on the rule “Don’t just do something, sit there.”

Doing nothing and sticking to a selected fund for the long term — or just selecting funds at random and then sticking to them — can be a significant source of alpha in the long run. Of course, this requires something that many investors find very difficult to implement: patience and discipline.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©iStockphoto.com/CSA-Archive