by Lance Roberts, Clarity Financial

It was interesting to see the markets reaction to the Consumer Confidence report on Tuesday, along with some of the media headlines, to wit:

“Consumer confidence just surged to its highest level since the recession. The latest reading on consumer confidence from the Conference Board came in at 104.1 for September, up from the prior month’s 101.8. The index touched 105.6 in August 2007.”

There are a couple of important points to consider in the statement above.

First, it is NOT surprising that after 8-years of an economic recovery that consumer confidence has finally recovered all the way back to where it was prior to the last recession. This is what you would expect of during any economic recovery, much less one driven by massive liquidity injections, Government programs to promote consumption and ongoing Central Bank interventions. The fact we are only NOW back at previous highs shows just how fractured the domestic economy was, and likely still is.

Secondly, and most importantly, records are a record for a reason. Record levels denote the point that previously marked the end of a cycle, not the beginning of a new one. This point is often missed by the mainstream media. Record highs of anything, whether it is economic, fundamental or financial data, are warnings signs of late stage events.

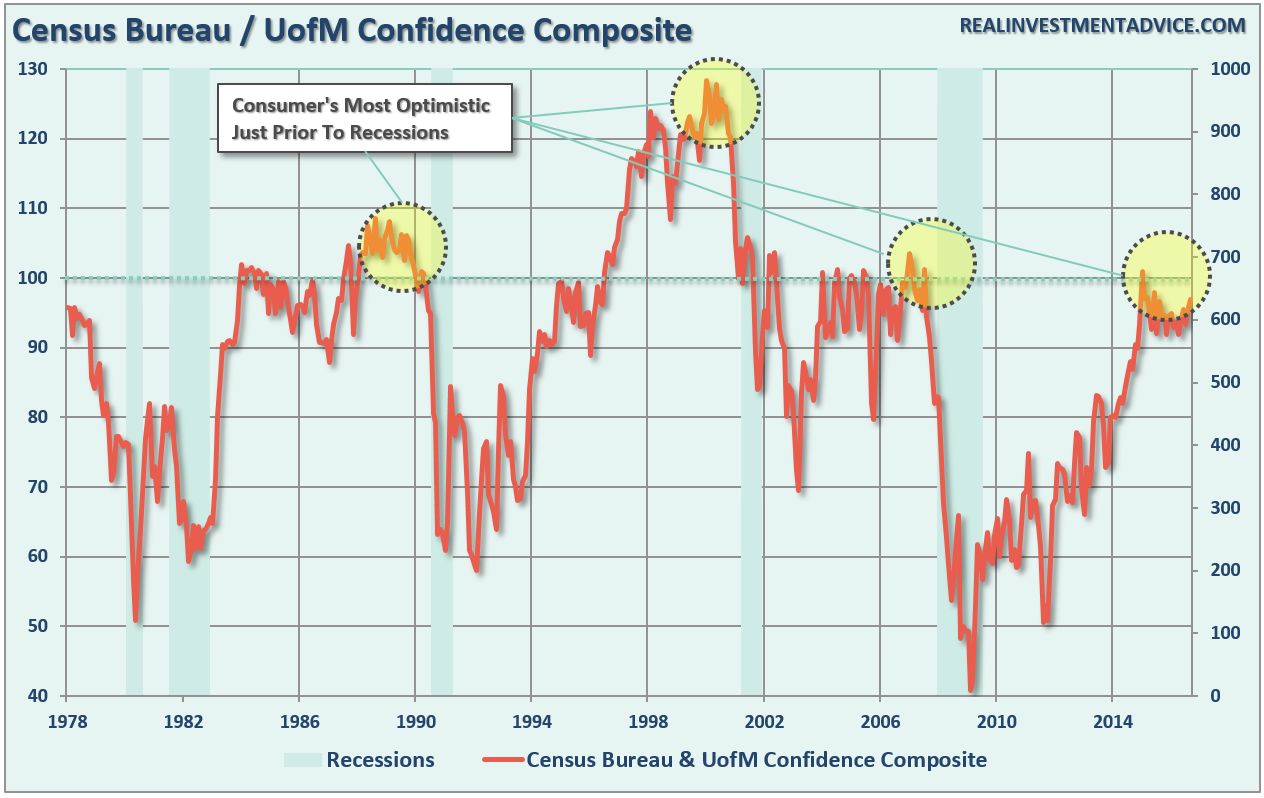

The chart below is the COMPOSITE confidence index which is an average of the Conference Board and University of Michigan consumer confidence indices.

As I said, it is not surprising that consumers are THE MOST optimistic just prior to the onset of a recession.

But is there a possibility of a recession?

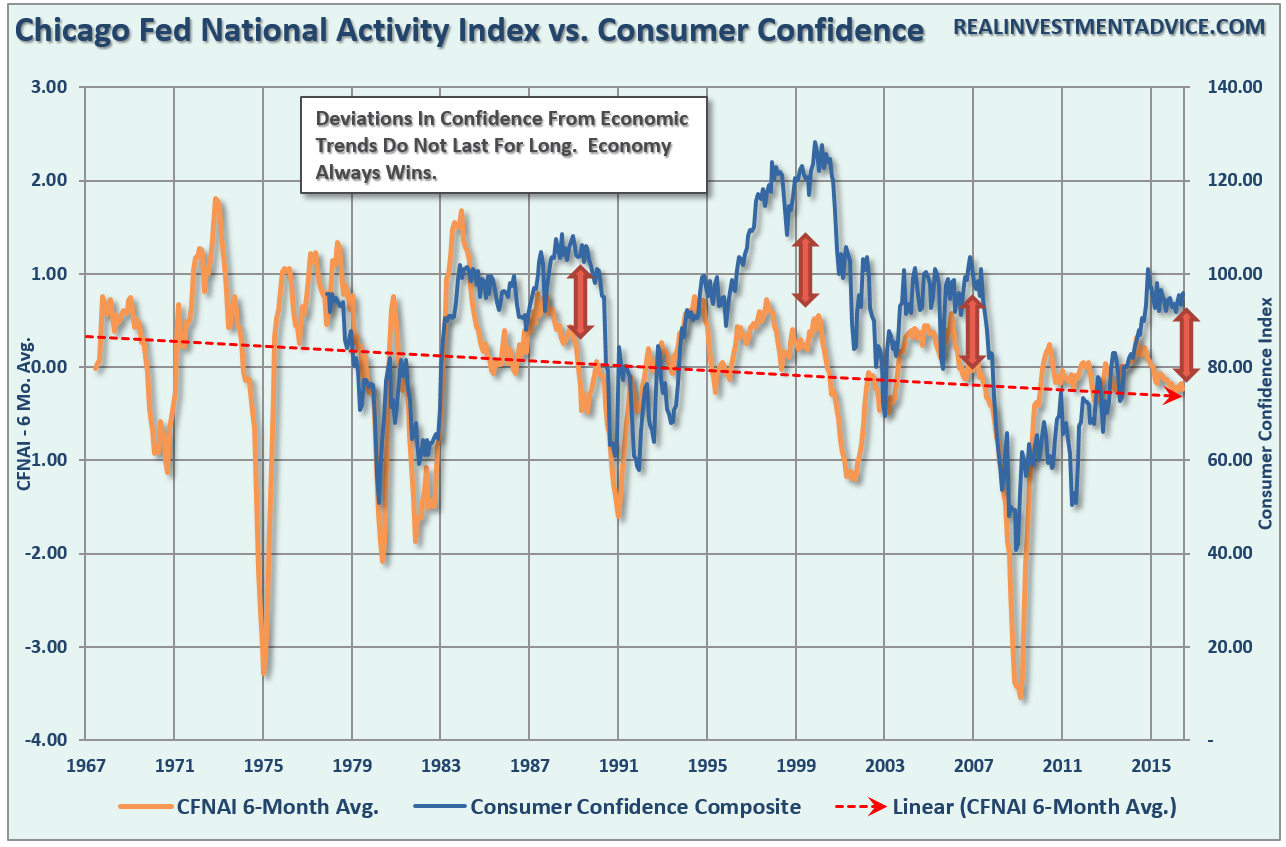

On Tuesday, I discussed the MOST IMPORTANT economic indicator – the Chicago Fed National Activity Index.

“While economic numbers like GDP or the monthly non-farm payroll report typically garner the headlines, one of the most useful economic measures is the Chicago Fed National Activity Index (CFNAI). The index is a composite index made up of 85 subcomponents which give a broad overview of overall economic activity in the U.S. Unfortunately, the media gives it little attention.

Currently, the CFNAI is not confirming the mainstream view of stronger “economy” headed into year-end, but rather one that may well be closer to the brink of recession. The chart below shows the diffusion index of the CFNAI index as compared to the S&P 500. Since the markets are reflective of the economy, the diffusion index shows the trend of the 85 subcomponents of the index. As shown, each time the diffusion index has reached current levels previously, the outcome for the economy and the markets was not so good.”

I have compared the CFNAI to the consumer confidence composite below. As you can see, there is a fairly high correlation between the two measures and recessions have been marked by declines.

We get a different view by using the 6-month average of the CFNAI, and again comparing it to the consumer confidence composite. You will notice the same correlation in the data as shown above. However, the temporary deviations between consumer confidence and the economy tend to occur in the latter stages of an economic expansion as “hope” runs high. Unfortunately, “hope” is eventually grasped by “reality” as consumer confidence plays catch-up with the economy and not the other way around.

While consumer confidence is hitting peaks currently, it should really be viewed as a warning rather than a reason to run out and commit capital to risk assets at potentially the wrong time.

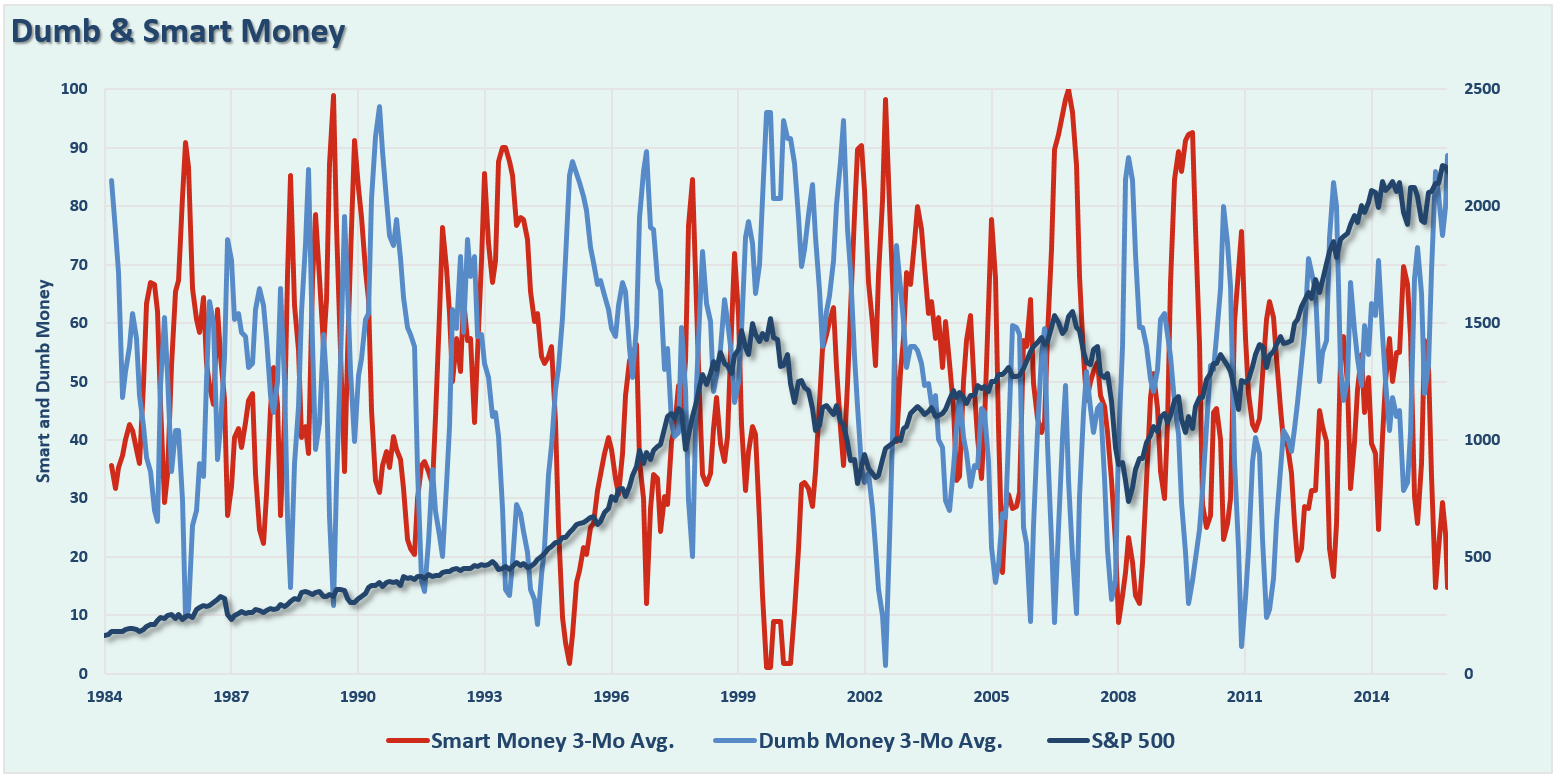

Is The Dumb Money Doing It Again

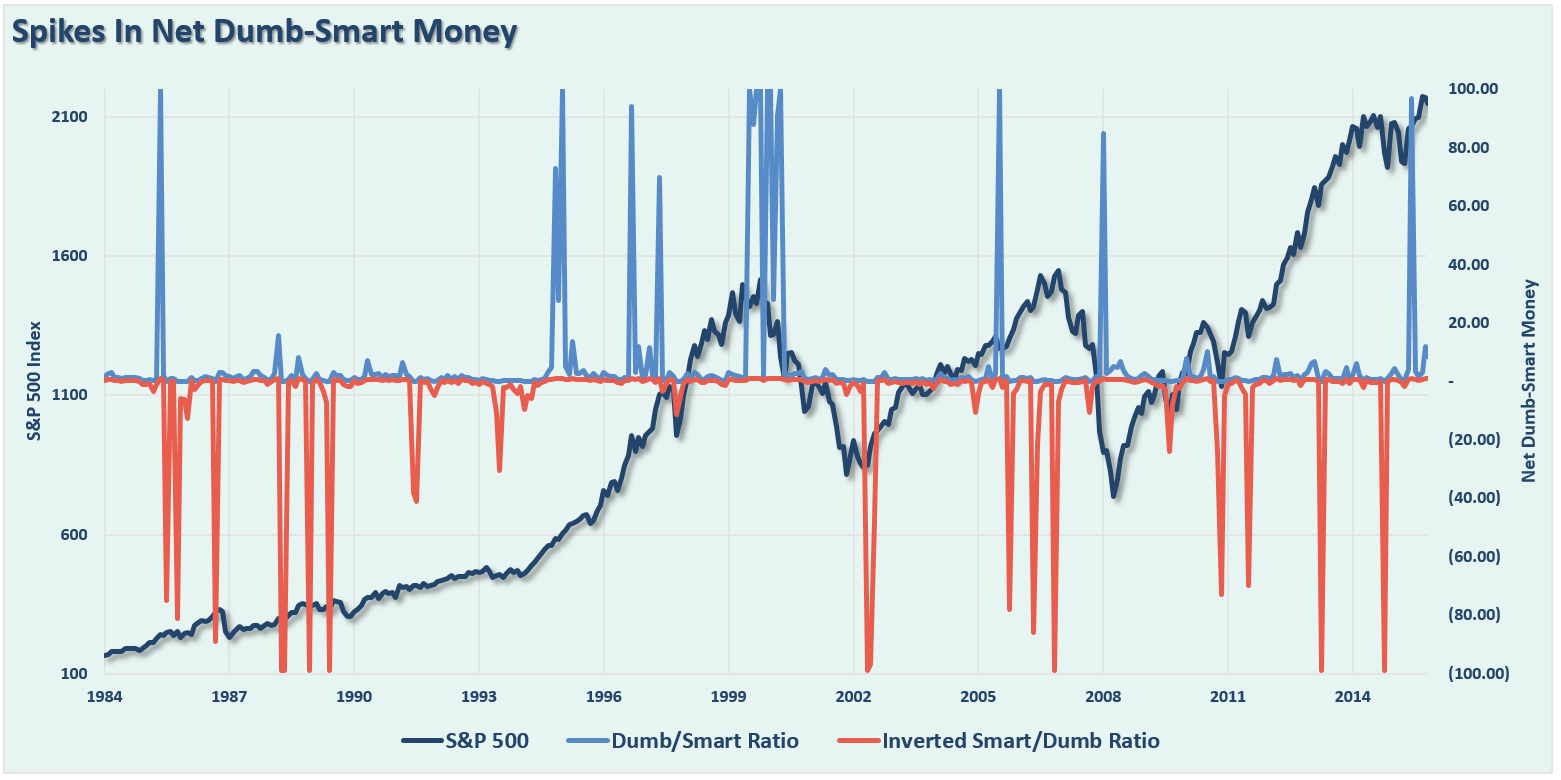

Despite the warnings of the economic and fundamental data, the exuberance of investors is always an interesting phenomenon to watch. One way to view investor behavior is by looking at the commitment of traders (COT) data to see where large traders (supposedly the smart money) and retail investors (the dumb money) are placing their bets. The chart below shows the data smoothed with a 3-month average going back to 1984.

While the data is “noisy,” a cursory look reveals what is generally accepted in the financial markets – “you suck at investing.” Small traders consistently buy tops and sell bottoms even though they are repeatedly told just to “buy and hold” long-term.

This should immediately make you question what you hear in the media and from financial pundits. If THEY are all telling you to “buy and hold” because YOU can’t effectively manage your money, then why are THEY not following the same advice? As the old axiom goes:

“If you are playing poker and can’t tell who the pigeon is, it’s you.”

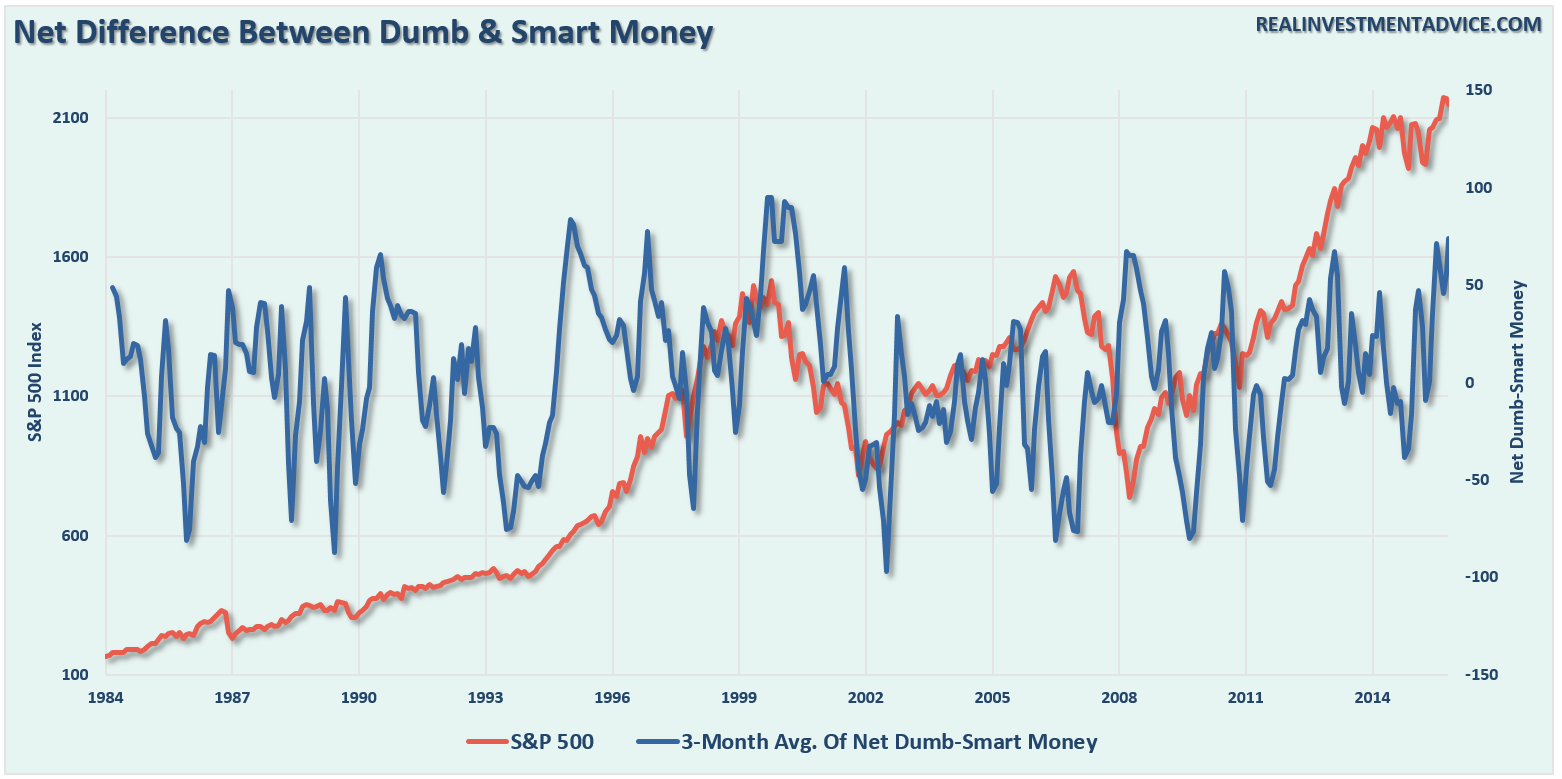

Another way to look at the data is to take the net difference of the two measures and subtracting the “smart money” from the “dumb money.” I have once again smoothed the data with a 3-month moving average to reduce the noise. What we find is once again a high propensity of retail investors to be buying into the market near both short and intermediate-term market peaks.

Lastly, if we take the ratio of the dumb-to-smart money and an inversion of the smart-to-dumb ratio we once again find further confirmation of retail investors poor investment decision processes.

Here is the point. Once again, we are witnessing smart-money reducing exposure to “risk” while retail investor continues to stay invested. This will likely not end well and, as I addressed Tuesday, there are many indications that we are likely very near a long-term peak in the market.

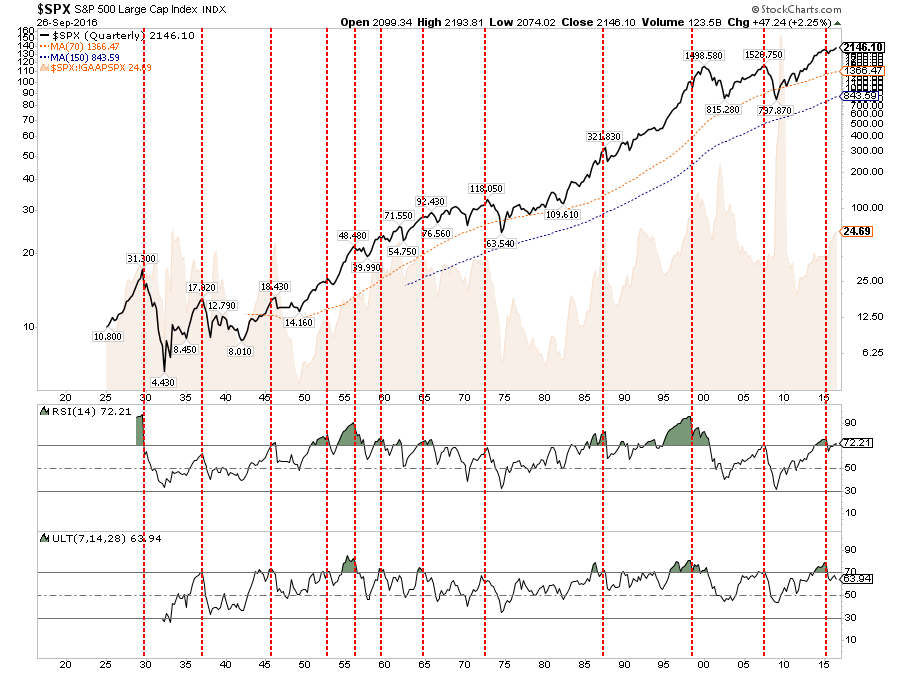

“The short-term outlook remains bullishly constructive for the moment as long as the market can maintain the bullish trend line from the February lows. However, on a longer-term basis, the economic and fundamental data is having a much more difficult time trying to support current price and valuation levels. As shown in the chart below of quarterly data, the market is currently at levels that have historically ALWAYS been associated with a major peak.”

It might be worth turning off the “nattering nay-bobs” on television and start thinking about what the “smart money” knows that you don’t.

But They Said The “Bond Bull” Was Dead…Again

Beginning in 2013, I started writing a series of articles suggesting why interest rates were going lower for longer.

When Bill Gross said the bond bull market was dead – I bought bonds.

When the mainstream media repeatedly touted the “death of the bond bull” each time rates ticked up, I bought more bonds.

Three weeks ago, the media once again started proclaiming the death of the “bond bull market” once again. And…I bought bonds. To wit:

“This past week there was ample commentary suggesting interest rates were set to “soar” higher and the death of the“bond bull market” was finally here. While such commentary is always inevitable whenever rates rise for any given reason, it is hardly the case.

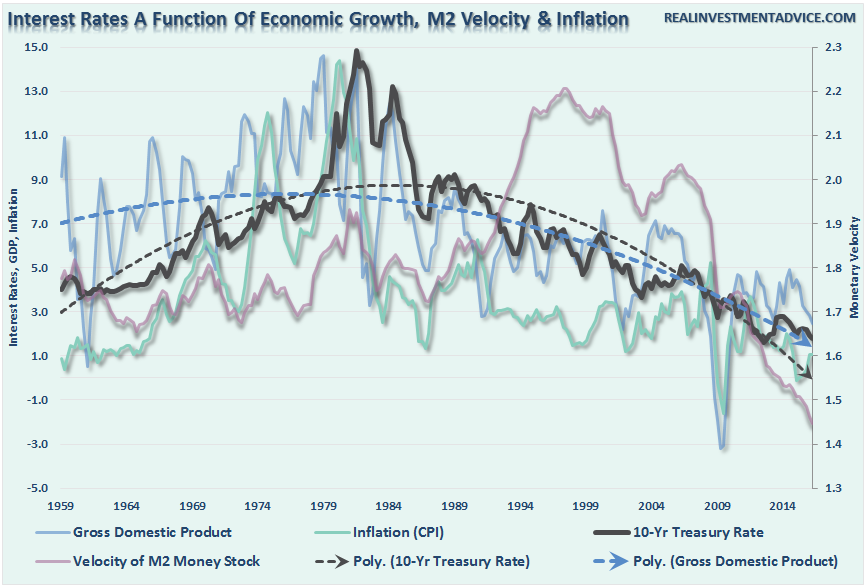

First of all, as I have stated previously, interest rates do not function in isolation. They are a function of economic growth over time as borrowing costs are driven by the demand for credit given the return on investment generated from borrowing activities. In other words, money isn’t borrowed at 4% interest if the return on the use of those borrowed funds is 3%.

The chart below proves this.”

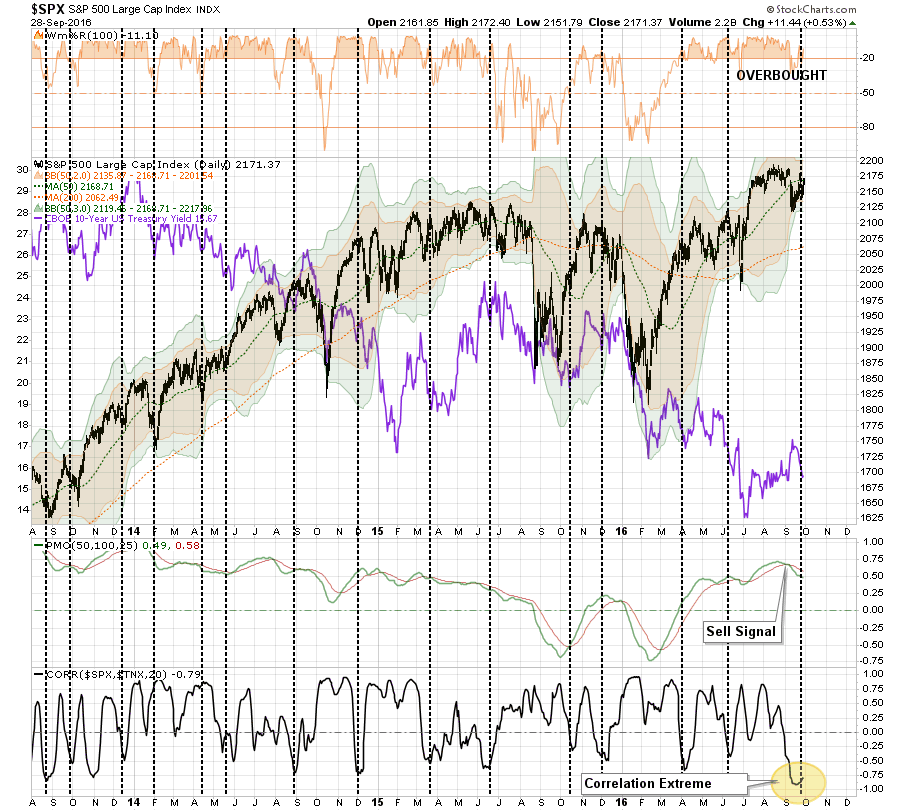

“Given that interest rates had gotten extremely oversold during the “Brexit,” money poured into bonds for safety, it is not surprising to see rates have a reflexive move higher. What we saw on Friday was likely rate “shorts” being blown out of positions.

However, interest rates are now at extreme overbought levels only seen near peaks in interest movements AND pushing on the downtrend line from 2015. This will likely prove to be a decent opportunity to rebalance bond exposure to target levels in portfolios next week.

I will be adding more bonds to portfolios next week as well.”

Chart updated through this week:

Interestingly, as I stated last week:

“With 10-year rates now back to an overbought condition (bonds now oversold), and pushing the accelerated downtrend line that began with the conclusion of QE3, the most likely movement will be down in conjunction with a ‘risk-off’ move in the markets.”

Importantly, while interest rates could possibly tick higher to the long-term downtrend line at 2.1%, (OMG, run for the hills), the reality is the economy is not growing strongly enough to support substantially higher rates which will push the economy more quickly towards the next recession.

Of course, it is during recessions that interest rates fall sharply. Given the rising level of evidence of a potential recession within the next 12-18 months, and with the majority of global economies already sporting negative rates, I continue to expect Treasury yields to ultimately approach zero.

Of course, there is also this little problem of correlation extremes between bonds and stocks, especially when combined with overbought conditions and sell signals. If history plays out, the next correction in stocks will likely break the uptrend and send money rushing back into bonds for “safety.”

I wouldn’t be too quick on making funeral arrangements for the “bond bull market” just yet.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In

Copyright © Clarity Financial