3 Things: The Economic Fabric & Rising Recession Risks

by Lance Roberts, Clarity Financial

LIBOR Pointing To Weaker Economy

Last week, I laid out the 12-reasons for why stock market “bulls” should pray that interest rates don’t rise. Just one word describes the outcome of that event given the current excessively leveraged consumption based economy of today – disaster.

The point here is that with the Federal Reserve talking about “tightening” monetary policy by hiking the “Fed Funds” rate – the reality is the Fed Funds rate has little to do with the actual credit market. The Fed rate is not actively traded and variable rate financial products are not linked to it. However, the London Interbank Offered Rate (LIBOR) is the rate used as the benchmark for many adjustable rate mortgages, business loans and financial instruments traded on global financial markets. In other words, increases in LIBOR tightens the flow of liquidity in many of the debt markets that directly affect the average consumer and small business by increasing costs. This is particularly burdensome when annual rates disposable income growth is on the decline.

Danielle DiMartino-Booth pointed out this problem in her latest post:

“Disposable personal income growth, adjusted for inflation, grew by 2.2 percent over last year, a full percentage point below March’s 3.2-percent pace. That downshift helps explain two things. For starters, the saving rate fell in June to 5.3 percent, the lowest since last October. Meanwhile, revolving credit growth, aka credit card spending, galloped ahead at a 9.7-percent annual rate.”

In other words, consumers are turning to credit consumption to support their current standard of living rather than the expansion of consumption. This is why economic growth continues to wane.

This brings me to my point. If it is LIBOR that affects the consumer, and ultimately economic growth given the 70%ish contribution of consumption to it, then we should be looking at the rates that directly impact the consumer. Whether it is auto loans, mortgages, variable rate debt, credit cards, etc., those interest rate costs are directly impacted by changes in LIBOR.

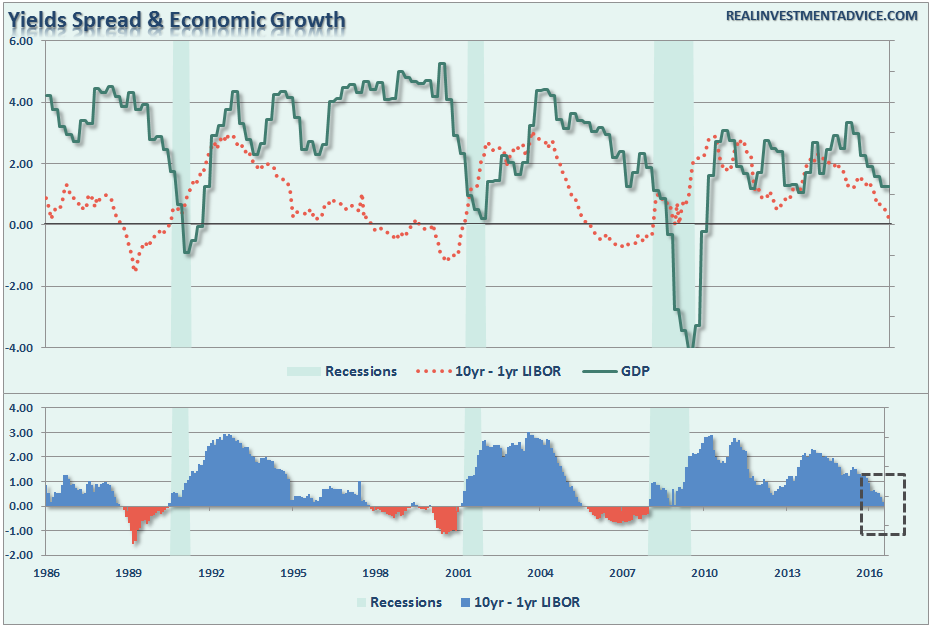

The chart below shows the spread between the 10-year Treasury and the 12-month LIBOR. With interest rates rising sharply on the short end of the yield curve the impact to consumption will likely occur sooner than currently anticipated.

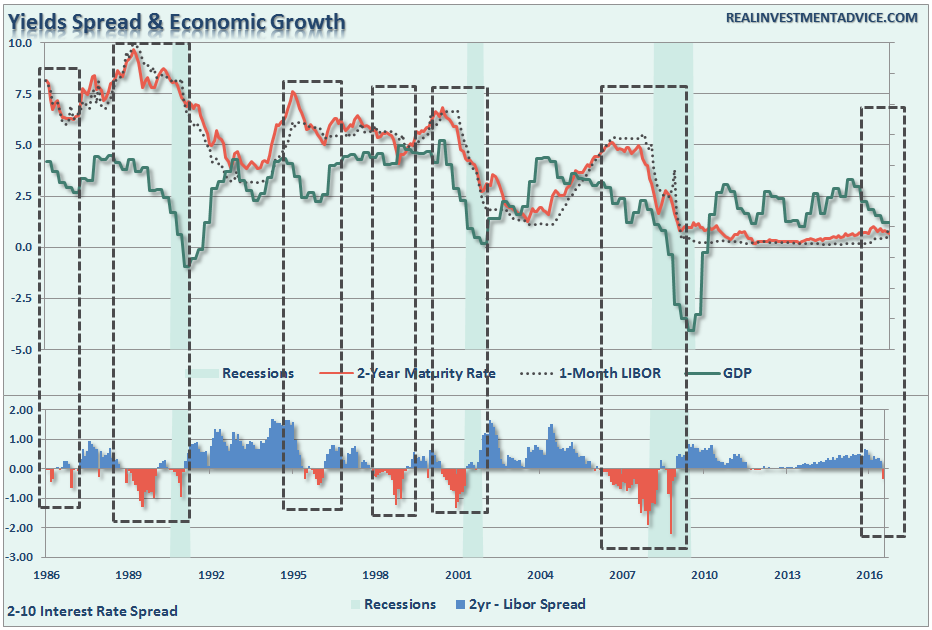

We can see this more clearly by looking at the very short-end of the yield curve and the spread between the 2-year Treasury rate and the 1-month LIBOR.

As shown, there is a very high correlation between negative spreads and future economic growth. In every instance where there has been a negative spread on rates, the economy has either slowed markedly or was in a recession.

As my Dad used to warn me just before I broke something that was previously working:

“Do you really think it is a good idea to mess with that?”

With the Fed hopeful strong economic data is on the way, the recent bounce in the data is likely not much more than that. The data suggests, on any fronts, the Fed will once again be disappointed as LIBOR “front ran” them to sharply tightening liquidity leading to further consumer constraint.

The potential for a Fed policy mistake at this juncture is extremely high and climbing.

All Tapped Out

Let me expand on this idea that consumers are ramping up debt to maintain their standard of living, primarily to offset surging healthcare costs courtesy of the Not-So-Affordable Care Act.

Recently, there have been many articles pointing to the rising saving rate, as reported by the BEA, as the reason why consumers are spending less. That rise was short-lived as wage growth turned sharply lower since the beginning of this year.

As shown, the savings rate, while higher than it was in prior to the financial crisis, is still well below levels that would signify a more healthy household balance sheet. However, I suspect that even the current increase in the personal savings rate, as reported by the BEA, is wrong.

Given the lack of income growth and rising costs of living, it is unlikely that Americans are actually saving more. The reality is consumers are likely saving less and may even be pushing a negative savings rate.

I know suggesting such a thing is ridiculous. However, the BEA calculates the saving rate as the difference between incomes and outlays as measured by their own assumptions for interest rates on debt, inflationary pressures on a presumed basket of goods and services and taxes. What it does not measure is what individuals are actually putting into a bank saving or investment account. In other words, the savings rate is an estimate of what is “likely” to be saved each month.

However, as we can surmise, the reality for the majority of American’s is quite the opposite as the daily costs of maintaining the current standard of living absorbs any excess cash flow. This is why I repeatedly wrote early on that falling oil prices would not boost consumption and it didn’t.

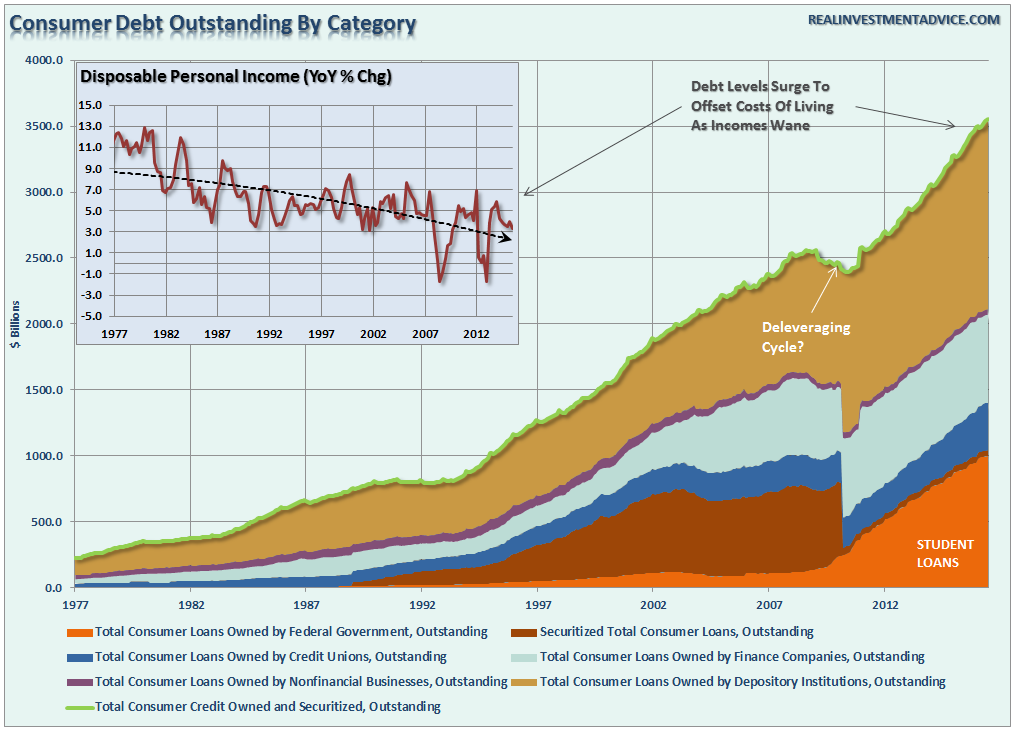

As shown in the chart below, consumer credit has surged in recent months.

Here is the other problem. While economists, media, and analysts wish to blame those “stingy consumers” for not buying more stuff, the reality is the majority of American consumers have likely reached the limits of their ability to consume. This decline in economic growth over the past 30 years has kept the average American struggling to maintain their standard of living.

As shown above, consumer credit as a percentage of total personal consumption expenditures has risen from an average of 20% prior to 1980 to almost 30% today. As wage growth continues to stagnate, the dependency on credit to foster further consumption will continue to rise. Unfortunately, as I discussed previously, this is not a good thing as it relates to economic growth in the future.

“The massive indulgence in debt, what the Austrians refer to as a “credit induced boom,” has likely reached its inevitable conclusion. The unsustainable credit-sourced boom, which led to artificially stimulated borrowing, has continued to seek out ever diminishing investment opportunities.”

Ultimately these diminished investment opportunities repeatedly lead to widespread malinvestments. Not surprisingly, we clearly saw it play out “real-time” in everything from sub-prime mortgages to derivative instruments which were only for the purpose of milking the system of every potential penny regardless of the apparent underlying risk. We see it playing out again in the “chase for yield” in everything from junk bonds to equities. Not surprisingly, the end result will not be any different.

So, don’t blame those poor consumer’s for not spending – they are spending everything they have and then some.

The Job Recovery Is Likely Over

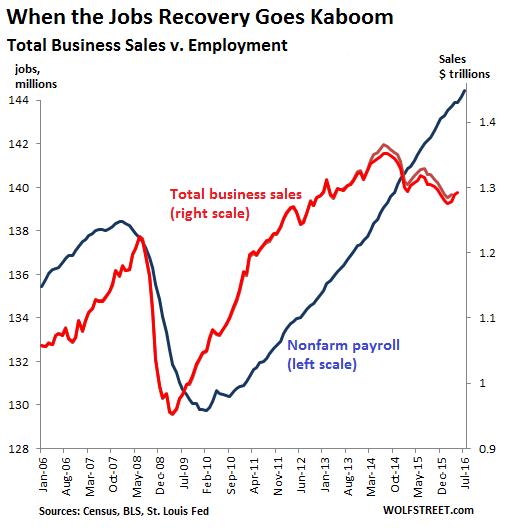

Wolf Richter penned a very interesting piece lately entitled: “This Is When The Jobs “Recovery” Goes KABOOM.”

“It will eventually impact the labor market. Here’s why: despite the hiring that companies have been doing, sales – the ultimate measure of “output” – have been heading south since mid-2014.

Total business sales, according to Census Bureau data, which include sales within the US by all companies, not just the largest in the S&P 500, peaked in July 2014 at $1.35 trillion. By May this year, the most recent data available, they’d dropped 4.4% to $1.29 trillion.

Despite sales cascading lower for a year-and-a-half, nonfarm employment from June 2014 through July 2016 has risen by 5.6 million jobs! And that’s what the productivity decline is also showing: the additional labor hours have been accompanied by a decline in sales!

The chart shows how jobs and total business sales are normally on the same wave length: When sales get hit, businesses cut their payrolls; when sales pick up, businesses hire. But since June 2014, a peculiar phenomenon has set in, with employment (blue line, left scale) rising and sales (red line, right scale) falling.”

This also confirms my comment recently on business investment.

“The +85k unadjusted number also confirms the trends of fixed and non-private residential investment. Businesses hire against the demand for their products and services. This is why, as shown in the chart below, the historical relationship between employment and fixed investment is extremely high….until now.”

Business investment does not fall in isolation. Companies invest in buildings, property, plant, and equipment when consumer demand is strong and economic growth is strengthening. As investment is made to expand production, more employment is needed to meet that demand. The opposite occurs prior to recessionary onsets.

Currently, while the BEA continues to spew out record job numbers, due primarily to seasonal adjustments and other factors, a substantial number of business activity indicators are suggesting the data is being substantially overstated. Future negative revisions to the data should not be surprising.

If you step back and weave all of these points together from consumer credit, to employment to wages, savings and interest rates, the picture of rising recession risks clearly emerge.

With markets ignoring the data, the outcome for investors is likely not pretty.

As David Rosenberg stated just recently:

“Okay, this really is one weird market.I am looking at the hedge fund proxy market positioning from the latest Commitments of Traders report from the Commodity Futures Trading Commission, and the results are startling. I’m quite sure I have not seen such levels of confidence on one hand, and cognitive dissonance on the other.”

Just some things I am thinking about.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial.