The Helicopters Have Arrived

by Carl Tannenbaum, Asha Bangalore, Northern Trust

SUMMARY

- Notes From Japan: The Helicopters Have Arrived

- Mark Carney Takes Center Stage After Brexit

- Lessons From Puerto Rico

The search for the perfect noodle soup is one that I hope never ends. But it came close to a conclusion during last week's visit to Japan. My daughter located Afuri, a ramen shop rated one of the best in Tokyo. After spending fifteen minutes trying to figure out how to operate the ordering machine in the corner, we were served the most beautifully-composed bowl I have ever seen. And the eating was even better. Slurping is encouraged, which goes against everything we've taught our children about table manners.

We saw perfection in composition on many fronts during the trip. But the Japanese economy is far from perfect or composed. Japanese policy makers face challenges unique to their nation, but there are lessons from the Far East that the West would do well to appreciate.

Japan was the darling of the global economy thirty years ago. Its industry was ascendant, its products were viewed as best-in-class, its banks occupied the top ten places on the global list and its management techniques were studied and emulated worldwide.

But asset prices got far ahead of fundamentals, and the eventual correction was severe. The Nikkei average fell by about 60% starting in 1990, and real estate values were similarly devastated. This created credit problems for the banks, which regulators chose to not to confront. Financial institutions pulled back on lending, consumers became conservative, and the result was a "lost decade," although the difficulty has lasted much longer than 10 years.

The first lesson we can draw from this history is that banking problems should be met head-on. The "delay and pray" strategy doesn't diminish the pain; it merely makes it chronic instead of acute. As we've argued before, it's best for bank supervisors to respond to crises by first getting additional capital into banks and then pressing for aggressive resolution of bad debts.

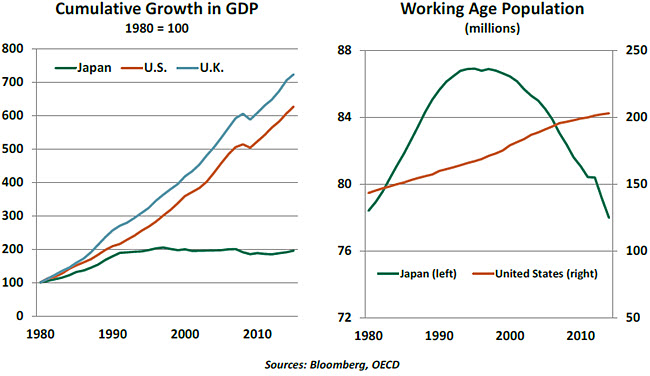

Japan's economic malaise corresponded with, and was reinforced by, a dramatic aging of the Japanese population. Japan has one of the lowest rates of immigration in the developed world; the purity of the culture is of paramount importance. (While we generally found the Japanese to be very welcoming and friendly, one evening my daughter and I were waved out of a local restaurant when we attempted to enter.) Birth rates are very low, in part due to the stigma faced by professional women who want to return to work after becoming mothers.

The collective aging of the population raised saving rates, lowered investment, and diminished productivity. According to the Organization for Economic Cooperation and Development, Japan's potential economic growth rate has fallen by 75% since 1990. Therein lies a second valuable lesson: don't get old. Countries that have growing and dynamic labor forces will move ahead; those that don't will be left behind. This is an aspect of the global immigration debate that deserves careful consideration.

The collective aging of the population raised saving rates, lowered investment, and diminished productivity. According to the Organization for Economic Cooperation and Development, Japan's potential economic growth rate has fallen by 75% since 1990. Therein lies a second valuable lesson: don't get old. Countries that have growing and dynamic labor forces will move ahead; those that don't will be left behind. This is an aspect of the global immigration debate that deserves careful consideration.

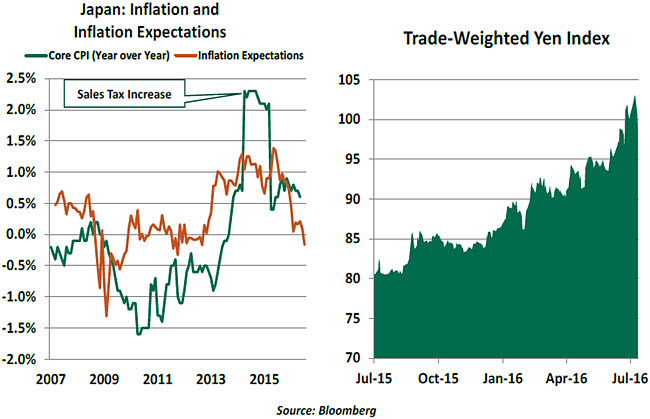

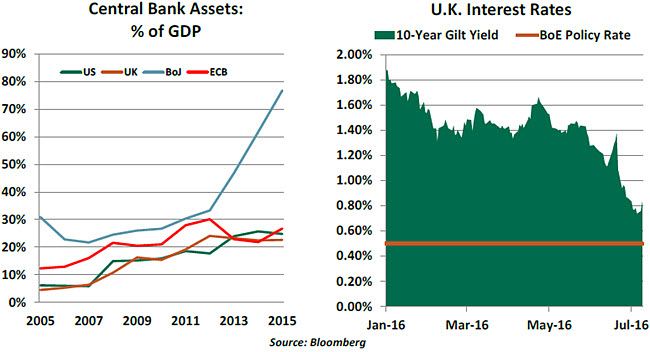

With Japanese growth running below even its meager potential, deflation set in. And more perniciously, the expectation of deflation set in. This served to hinder consumption even further (why buy now when it will be cheaper tomorrow?). Interest rates have been lower for longer in Japan than anywhere else, and its quantitative easing program is larger (as a percentage of gross domestic product) than that of any other country. Yet market-based inflation compensation remains negative and consumer surveys on inflation expectations are reporting their lowest levels since 2013.

Further frustrating the Bank of Japan has been the surprising strength of the Japanese Yen. (A glass of beer in a bar cost the equivalent of $15!) Monetary policy has sought to weaken the currency in order to advance exports, but international investors have viewed Japan as a safe haven during recent periods of volatility. The yen has actually gained 15% against a trade-weighted basket of currencies so far this year.

So, given all of these constraints, what can be done? That is the question facing Prime Minister Abe and Haruhiko Kuroda, his hand-picked leader of the central bank. Japan implemented negative interest rates on a very limited basis last January, but they have had little effect. And so "helicopter money" is at hand. Dropping currency onto the streets is not practical in the modern day, but the combination of government spending and central bank investment in government debt can achieve the same outcome. If the Bank of Japan agrees to hold the debt perpetually, or forgives it outright, the economy essentially receives yen from the sky.

Achieving this outcome requires close coordination between fiscal and monetary authorities. This is clearly present in Japan, but officially taboo elsewhere. Yet with central banks around the world holding increasing amounts of sovereign debt for increasing lengths of time, one might wonder whether monetization is already underway.

Achieving this outcome requires close coordination between fiscal and monetary authorities. This is clearly present in Japan, but officially taboo elsewhere. Yet with central banks around the world holding increasing amounts of sovereign debt for increasing lengths of time, one might wonder whether monetization is already underway.

Here too, the Japanese dynamic will bear close watching. Other countries find themselves with reduced options to deal with economic disappointment and high debt levels, which might lead them to reconsider the optimal degree of central bank independence.

In an interesting historical anecdote, the Japanese tried a helicopter money program in the 1930s. It ended with soaring inflation, deep fiscal austerity, and the assassination of the Japanese finance minister. We should certainly hope for a better outcome this time around.

Our conference took one afternoon off from discussion to visit Kamakura, a beautiful seaside city. At one stop, we were given instruction in Zen meditation, which aims to promote balance and serenity. If only we could arrange a large group class for the global economy...

A Central Banker for the Long Run

Looming economic and financial risks. A paralyzed legislature. A difficult leadership transition. An anxious and angry public. And a central banker trying to put a cushion under a crisis.

These circumstances describe the United States in 2008, with Ben Bernanke playing the leading role. But they also describe today's United Kingdom, with Bank of England (BoE) Governor Mark Carney attempting a reprise of Bernanke's bravura performance. Much is riding on the outcome of Carney's orchestration.

The BoE was forced to look outside for new leadership when Sir Mervyn King retired in 2013. Heirs apparent within the BoE had allegedly collaborated with banks to understate interbank borrowing rates during the financial crisis, in an effort to sustain confidence in the financial system. The resulting scandal led to a global search for a new Governor.

Mark Carney was something of a controversial choice, as he is the first foreign leader in the 322-year history of the BoE. While he worked in England for a time, he did so for Goldman Sachs, which has been vilified in some corners in the aftermath of the financial crisis. His annual salary of #880,000 makes him the most handsomely compensated of leading central bankers; he earns nearly six times what Janet Yellen does.

Nonetheless, Carney came to his current role with very strong credentials. He led the Bank of Canada for five years during the financial crisis and was the first central banker to cut interest rates in 2008 in anticipation of what was to come. The Canadian economy was the first in the developed world to return to its pre-crisis levels of output and employment.

Carney is also credited with shepherding Canadian banks though that era without experiencing the trauma seen in other countries. To be sure, the structure of the Canadian financial system and Canadian financial products does not allow for the same kinds of excess seen in the United States. But Carney's instinct to pledge substantial amounts of liquidity support proved correct.

Monetary policy in the United Kingdom has been on cruise control since Carney took the helm. The British economy has performed very well, allowing the BoE to close its quantitative easing (QE) program in 2012. Benchmark interest rates have been unchanged for the past seven years.

Until the Brexit vote, the questions surrounding the BoE centered on when interest rates might be raised. But the economic consequences of Brexit have changed the paradigm.

Given the post-Brexit disarray in other areas of U.K. leadership, Carney's aggressive tone since the referendum has been especially important. He knows the drill: get out in front of potential problems, with force, to sustain confidence in the financial system. The challenge in the current day, and his current place, is that monetary policy has already been stretched close to its limits. There is little room for rates to decline, and long-term interest rates in the United Kingdom are already at record lows without additions to QE.

Given the post-Brexit disarray in other areas of U.K. leadership, Carney's aggressive tone since the referendum has been especially important. He knows the drill: get out in front of potential problems, with force, to sustain confidence in the financial system. The challenge in the current day, and his current place, is that monetary policy has already been stretched close to its limits. There is little room for rates to decline, and long-term interest rates in the United Kingdom are already at record lows without additions to QE.

Nonetheless, Carney and his Monetary Policy Committee may feel the need to press forward. Given the current political dynamic on both sides of the English Channel, it could be some time before Brexit discussions can begin to limit the potential damage to the U.K. economy. And additional fiscal stimulus seems like a remote possibility at this point.

Somehow, Mark Carney finds time to run marathons when he is not directing the Bank of England. He may need to draw on his endurance in the coming months; there is a long and potentially bumpy road ahead.

On An Island

"Puerto Rico,

My heart's devotion--

Let it sink back in the ocean."

-- "America," West Side Story

The Territory of Puerto Rico has a unique relationship with the United States. Those born in Puerto Rico are U.S. citizens, and they can serve in the American army. But they have their own Olympic team. Bonds issued by Puerto Rico enjoy the same tax preferences enjoyed by U.S. states, but the island cannot access the debt resolution process available to U.S. states.

This last paradox has been front and center as Puerto Rico has careened into bankruptcy. The island's economy had long benefitted from incentives granted by Washington; for many years, U.S. firms had an exemption from taxes on profits earned in Puerto Rico. This led to significant amounts of industrial investment, with drug companies in the forefront.

This last paradox has been front and center as Puerto Rico has careened into bankruptcy. The island's economy had long benefitted from incentives granted by Washington; for many years, U.S. firms had an exemption from taxes on profits earned in Puerto Rico. This led to significant amounts of industrial investment, with drug companies in the forefront.

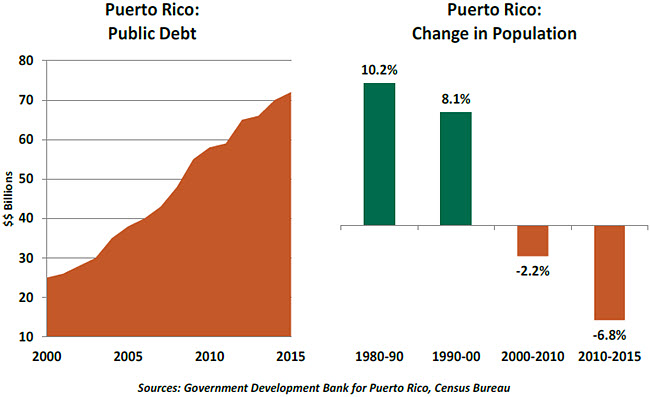

Congress voted to phase out this favorable treatment over a ten year period beginning in 1996. This had a predictable impact on investment and employment in Puerto Rico. Debt grew, taxes rose, and citizens left, a vicious cycle that eventually led to insolvency.

Last month, Congress established an oversight board to help Puerto Rico restructure its debt. It's too late to prevent bond defaults, but the action will make matters more manageable.

Does Puerto Rico establish a precedent for financially challenged U.S. states? In many ways, it is a special case; Puerto Rico was very deeply reliant on Federal tax policy, and the size of its debt relative to output is many times higher than even the most indebted state. But the case of Puerto Rico shows what happens when fiscal problems and out-migration become intertwined, triggering a competition between bondholders and citizens for scarce resources. State governments and municipal bondholders would do well to learn from this example.

Copyright © Northern Trust