Is Banking Going Back Into the Shadows?

by Carl Tannenbaum, Asha Bangalore, Ankit Mital, Northern Trust

Summary

- Is Banking Going Back Into the Shadows?

- Some Caution Around Commercial Lending

- Saudi Arabia Plans For Life Beyond Oil

We're pretty close with our neighbors. We like to go out as a group several times a year, and the conversation is always lively.

At a recent dinner, the fellow next door didn't have enough cash to pay his portion of the bill. He asked if I could lend him the difference. Of course, I said yes; but not before asking him to read a long series of fair lending disclosures and pledging his house as collateral.

Long-time readers of our work know that many of my openings are highly stylized (or just plain made up). But there are some who wish that the fictitious scene described above would become reality. There is an increasing amount of lending being done in our economy without the benefit of traditional intermediaries, and it has generated a lot of buzz. To supporters, this represents disruption in an industry that desperately needs it. To detractors, it raises the potential for abusive practices and increases systemic risk.

Interest rates have been very low for a long time now. One of the stated intentions of the policy was to encourage investors to be somewhat less conservative, placing their capital in areas that would be more helpful to economic growth. The concern surrounding this strategy is that some investors will end up in asset classes that are not the most comfortable for them, creating the potential for instability.

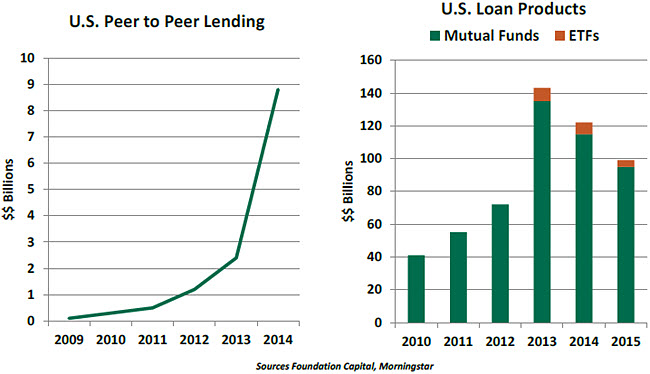

Given the search for yield, it is not surprising to see momentum behind peer to peer (PTP) lending, platforms where borrowers and lenders intersect directly. Hosts (like LendingTree.com) use data mining techniques to assess creditworthiness, providing some assurance of the ability to repay. Once a match has been made, an online depository facilitates the transaction.

The new mediums like to say that they are free of all of the legacy costs that burden traditional banks (too many branches, too much red tape), which allows lending at lower rates. Savers are drawn to returns that are well in excess of traditional certificates of deposit.

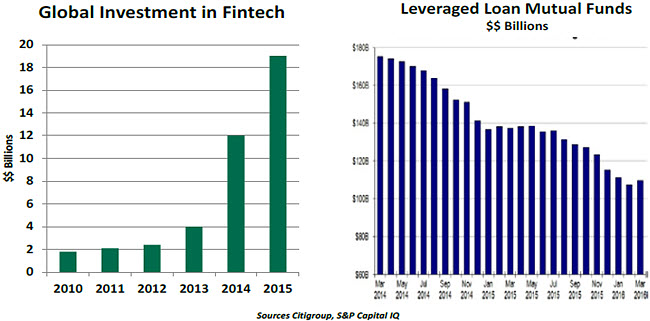

On a larger scale, asset managers are assembling pools of business and consumer loans to form mutual funds or exchange traded funds (ETFs). These structures have the benefit of pooling, meaning that the failure of a single loan is spread broadly across the owners of the fund. These vehicles currently contain nearly $100 billion in assets.

It is important to note that this sort of nontraditional lending is still a very small share of the total private credit outstanding in the United States. (Loans and leases on U.S. bank balance sheets total almost $9 trillion.) But these forms of alternative financing are growing rapidly, and have attracted the attention of financial supervisors.

It is important to note that this sort of nontraditional lending is still a very small share of the total private credit outstanding in the United States. (Loans and leases on U.S. bank balance sheets total almost $9 trillion.) But these forms of alternative financing are growing rapidly, and have attracted the attention of financial supervisors.

Lending through traditional channels is subject to regulation that is intended to protect both borrowers and lenders. The effective interest rate (inclusive of fees) must be calculated properly and disclosed to the borrower, and there are usury laws that prevent demands for excessive interest. Banks are required to lend into areas where they take deposits, offering credit somewhat more democratically. And they are required to hold capital against the potential for losses to prevent financial contagion.

Alternative lending structures are largely unburdened by these requirements. PTP arrangements essentially broaden the definition of lending to an acquaintance, which has traditionally been free from regulatory oversight. (Napster used this motif years ago to justify music sharing.) The banking industry is certainly interested in revisiting this interpretation, and a legal or lobbying battle on this front lies ahead. At the same time, banks are making substantial investments in financial technology to hedge their bets.

Loan mutual funds have become a locus for leveraged loans, which have been a persistent subject of regulatory concern. Leveraged loans are secured by cash flows of the underlying company, which can become impaired if economic conditions turn negative. These credits have caused challenges for banks, so there is certainly concern in some corners that this activity has moved to a channel with lower levels of oversight.

Ideally, those who lend into PTP marketplaces and those who own shares in loan mutual funds are well-informed investors who are aware of risk and able to absorb losses. But if history is any guide, there are novices mixed in with the experts. Loans are not the most transparent financial instruments, with the creditworthiness of the borrower in question. And when reversals of fortune arrive (as they inevitably will), we cannot be assured that they will be taken in stride.

A panicked response could make a challenging situation worse. Credit availability could constrict rapidly and desperate sellers could offer loans at fire sale prices. This could set a standard for similar loans on bank balance sheets, extending the contagion. Mutual funds may not be able to mark their loan books quickly enough, and may be challenged to provide the liquidity that investors have come to expect from them.

The "shadow banking system" was a villain in the 2008 financial crisis. The opaque web of off-balance sheet vehicles, conduits and derivatives allowed firms to work around bank capital requirements and take larger risks. In the aftermath of the crisis, new regulation significantly curtailed this activity.

The "shadow banking system" was a villain in the 2008 financial crisis. The opaque web of off-balance sheet vehicles, conduits and derivatives allowed firms to work around bank capital requirements and take larger risks. In the aftermath of the crisis, new regulation significantly curtailed this activity.

Alternative lending channels have some promise, but also some troubling ingredients: potentially ill-informed borrowers and lenders, intermediaries without skin in the game to encourage good underwriting, and light oversight. We need to avoid heading back into shadows so soon after seeing the light.

Past the Peak?

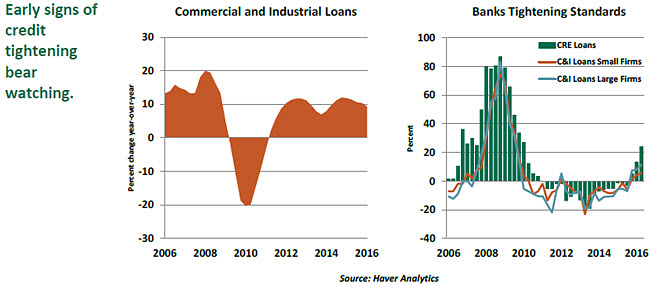

Credit conditions are powerful and magnify swings in the business cycle. Some recent developments suggest that things may be tightening up in this arena, which could hinder the expansion down the road.

The Federal Reserve's Senior Loan Office Opinion Survey of Lending Practices (SLOOS) captures bankers' views about loan underwriting standards. Bankers provide information about changes in their lending standards for major categories of loans to firms and households.

In recent quarters, bankers have signaled their intention to tighten underwriting standards for loans to businesses after nearly six years of easy lending conditions. The change in trend cannot be ignored because it has implications on the economy.

The SLOOS indicates that bankers are concerned about extending commercial and industrial (C&I) loans to both small and large businesses during the last three quarters. Relatively speaking, they look upon large firms less favorably than small firms. The net percentage of bankers tightening standards for commercial real estate (CRE) loans has risen for three straight quarters.

Tightening of credit standards is a gradual process, and it peaks during or after a recession. In the early stages, the economy continues to advance, and credit expansion does not stop. Current data are a close match to this situation.

C&I loans grew 9.3% from a year ago in the first quarter, which is higher than the historical median (7.8%, last 40 years). In the first quarter, CRE loans advanced 10.4% on a year-to-year basis; this reading exceeds the median of the last 12 years for which data are available.

Our research indicates that there are long lags between tightening of standards for business loans and the actual impact on loan growth. In particular, the peak of tightening standards occurs six quarters before the low point of C&I loan growth. The lag is longer for CRE loans (about 10 quarters). So there is no need for immediate concern, but this trend bears close watching in the quarters ahead.

The Rising Son

Saudi Arabia has a small population (just 29 million people), but it casts a big shadow over the global economy. So when the country recently announced plans to remake itself, it generated interest from around the world.

Last month, the all-powerful Deputy Crown Prince of Saudi Arabia Mohammad bin Salman (or MbS) announced Vision 2030. It is a blueprint for life after oil. The plan seeks to promote the non-oil sector, increase the share of the private sector and streamline the government.

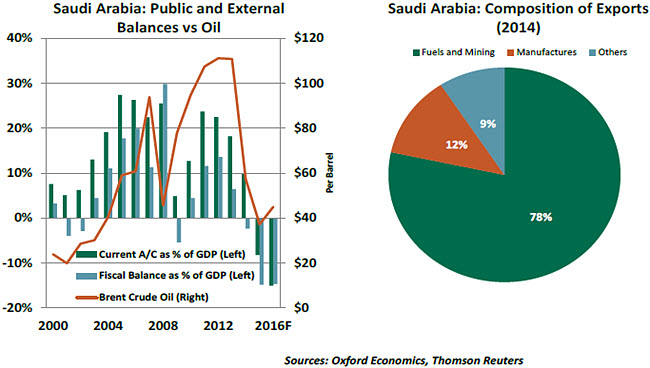

Saudi Arabia's current economic model is insufficient to provide jobs to its young and growing population or to finance its cradle-to-grave welfare system. Youth unemployment is more than 40%, while labor force participation is at just 40%. The country relies on oil for 80% of its exports and more than 90% of government revenue.

With the slump in the oil market, growth has come to a halt, while fiscal and current accounts have gone from surpluses to large deficits. Given the unsustainability, volatility and the inadequacy of a hydrocarbon-driven economy, there is little option for the Kingdom but to look beyond oil.

While ambitious, there is nothing novel about the plan. Most oil sheikhdoms face similar dilemmas. Qatar, United Arab Emirates and Bahrain announced a National Vision 2030 plan in 2008, while Kuwait announced a State Vision 2030 in 2010. Only the United Arab Emirates and, to an extent, Qatar have achieved success in developing a healthy non-oil service sector. Saudi five-year plans over the last three decades don't have much to show for. Does a similar fate await Vision 2030?

The biggest challenge for MbS will be to overturn the existing social contract in Saudi Arabia. The Saudi monarchy ensures secure and leisurely public sector jobs, and generous allowances for its population. The bureaucracy is inefficient and runs on grace and favor, rather than meritocracy. Furthermore, most of the population lacks technical expertise and an enterprising spirit. Can the Saudi workforce be relied on to take up jobs it has hitherto shied away from, and create something that the rest of the world may want to pay for?

The biggest challenge for MbS will be to overturn the existing social contract in Saudi Arabia. The Saudi monarchy ensures secure and leisurely public sector jobs, and generous allowances for its population. The bureaucracy is inefficient and runs on grace and favor, rather than meritocracy. Furthermore, most of the population lacks technical expertise and an enterprising spirit. Can the Saudi workforce be relied on to take up jobs it has hitherto shied away from, and create something that the rest of the world may want to pay for?

However, an absolute monarchy can steamroll changes, and MbS has shown signs that he can overcome policy inertia. Moreover, there is a small section made up of mostly the foreign-educated youth that seems to be ready for reform. The question is whether this change in spirit filters down to the rest of the population.

Key risks facing the plan are succession and the price of oil. MbS, 31, draws his power from his 80-year-old father King Salman, and would find it difficult to retain power in case of the latter's demise. A succession fight between the Crown Prince Nayef and MbS would most likely sabotage Vision 2030. A more optimistic scenario would see MbS build his own political base fast and pay off Nayef to give-up his claim on the throne. Secondly, when oil prices climb back up, the Saudi leadership likely will find it difficult to press ahead with politically painful reforms in the absence of budgetary pressures.

For the rest of the world, the import of these reforms is in the stability of Saudi Arabia and its role in the global energy markets. The energy policy, as is being pursued, would further diminish the role of the OPEC as Saudi Arabia doubles down on its quest of market share rather than propping up prices through the OPEC cartel. However, an economic failure, especially due to a succession fight, could severely disrupt the global oil markets and also adversely affect countries such as Egypt that are heavily dependent on Saudi aid.

The transformation of Saudi Arabia, as envisaged in Vision 2030, is a multi-generational project. Over the medium term, listing of the oil giant Aramco, rationalization of subsidies, fiscal rebalancing and the performance of the non-oil and private sector will give us some indication of progress. The world is vested in the success of the effort.

Copyright © Northern Trust