Tactical Models Under Pressure As US Stocks Rebound

by James Picerno, Capital Spectator

The US stock market may be on the verge of decisively throwing off its bear-market shackles and making fools of analysts (including yours truly) who’ve been issuing cautious commentary in recent months. It’s also been clear for more than a month that a previously issued markets-based warning on US business-cycle risk has been wrong, at least so far. As yesterday’s broad-minded review of economic indicators relates, the US economy wasn’t in recession in March, based on data published to date. In the wake of the equity market’s rally in recent weeks, the call that stocks were at risk of a bear market may be about to fade too.

So it goes in the dark art/science of trying to outwit Mr. Market and look for signals in the noise. The risk of being wrong is an occupational hazard for anyone who practices investing with something other than a buy-and-hold strategy. To be fair, every model that attempts to engineer higher returns, lower risk, or some combination is subject to failure at times. It’s the nature of the beast—no one can outfox the crowd all of the time. Even if you’re right 70% of the time, being wrong in real time outweighs previous successes on an emotional level.

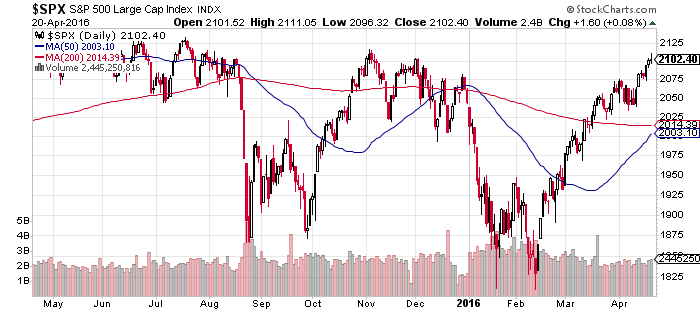

The question now is whether this we’re on the cusp of one of those times when model failure is about to spill out across the market landscape from a broad US equity perspective? The S&P 500 ticked higher again yesterday, posting another new year-to-date peak. Measured from the previous trough in early February, the index has climbed roughly 15%. In just over a month’s time, the mood has shifted from deep pessimism to exuberance. In the days ahead, analysts and investors will be under pressure to decide if the current exuberance is irrational or warranted.

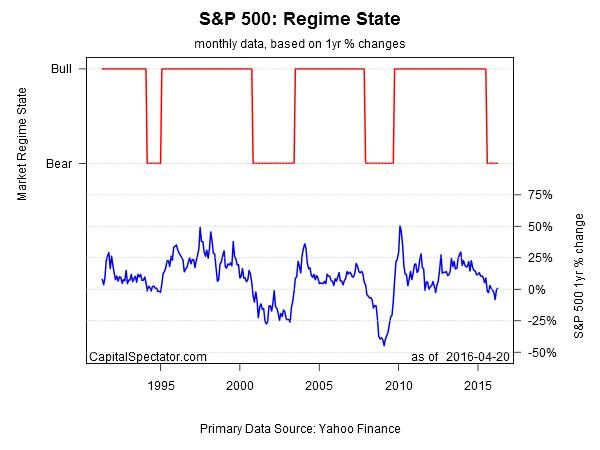

For some perspective on where we’ve been, recall that the current phase of volatility began last August, when China unveiled a surprise currency devaluation and global markets swooned in response. Bear-market signals from various models followed, including a popular tactical model that seeks to filter out noise by focusing on monthly data—current month-end price relative to a 10-month moving average–for monitoring market trends (“A Quantitative Approach to Tactical Asset Allocation”). But this model, like so many others, has been whipsawed in recent months via the monthly readings for the S&P. In the current climate, the bear-market signals have recently given way to bull readings… again. (For charts tracking various ETFs in context with this model’s signals, see Meb Faber’s updates here.)

The Capital Spectator is fair game for criticism as well in the wake of recent market volatility. For instance, an econometric application based on a Hidden Markov model that’s been discussed on these pages continues to signal that the US stock market remains in a bear market. This model has been consistently profiling a negative regime for equities since last fall, but that won’t mean much if it turns out to be wrong.

For investors who favor a buy-and-hold strategy, a hefty dose of vindication may be near. If you want to know why most efforts to generate superior risk-adjusted returns through time via various flavors of tactical asset allocation usually come to naught, recent action in the US equity market offers a real-time education.

But let’s not put a fork in the tactical models just yet. Even if the past six months have been an extended head fake for bearish signals, there’s still prudent reasons for embracing some degree of tactical models. Expecting superior results at all times, alas, is expecting too much. But that’s a subject for another day.

Meantime, back on the front lines of market action, the S&P has retraced all its losses—twice–since last August’s slide. In addition, the case for seeing an imminent recession for the US is still MIA, based on numbers in hand. But there have been worrisome signs of macro weakness in some corners of the economy—last week’s March numbers for industrial production and retail sales are the latest examples. Meantime, next week’s first-quarter GDP report is expected to deliver a tepid 0.3% rise, based on the Atlanta Fed’s Apr. 19 nowcast. Are these reports the raw material for a resumption of the bull market that was rudely interrupted last August?

We’ll have the answer shortly, perhaps within a few weeks. If the US stock market runs decisively higher from current levels, the sound you hear of crashing will be disgruntled tactical asset allocators throwing their models out the window. But that’s not yet fate.

There’s a severe round of comeuppance lurking around the next bend. The only mystery is where the axe will fall. Some of us think we already know the answer, but perhaps it’s time to roll out Robert Goldman’s famous phrase: “Nobody knows anything.” Actually, let’s rephrase that for use with market analytics: Nobody knows anything… in real time.