by Mawer Investment Management, via The Art of Boring Blog

Stanislav, now an analyst on our Canadian equity team, was fifteen when his family decided to move from Kazakhstan to Russia.

A tall, thin boy with dark hair and a focused expression, he belonged to a family of Russian restauranteurs.

Growing up in post-Soviet Kazakhstan and later Russia, Stanislav received an education in money that would seem alien to North American children. As a child, he overheard stories of shortages in currency, rapid inflation and people’s savings becoming worthless overnight due to valuation. It was not uncommon where he lived for people to buy electronics and food (whatever was available) as soon as they were paid because no one wanted to risk keeping it in savings. Few trusted that money would keep its worth in the future…because it rarely did.

As Stanislav recounts in one story:

“I remember that my family never played the lottery but one time my mother did and she won, to our surprise.

The crazy part was that the amount printed on the ticket was meant to be a big sum, enough to buy a refrigerator, but since it coincided with a period of rapid devaluation, the ticket became almost worthless by the time my mother received it.

She said it was not even worth the trouble to cash it in because of its meager value and the trouble of doing so.”

Imagine winning the lottery and not even bothering to cash it in because it wouldn’t be worth your time! That’s quick erosion of purchasing power.

Currencies play a major role in our lives. They impact what and how much we can buy, how we think about savings, and even where we go on vacation. Currencies impact us day-to-day and over the long run. And as the experience of post-Soviet Russia illustrates, they can have a big impact on our lives at times.

Unfortunately, the topic of currency is also one in which there is a great deal of confusion and indifference. Many people think about currency risk about as often as they do their appendix, i.e., never, unless there is a problem. And even those who do care about currency risk often struggle to wrap their heads around the topic given its complexity.

However, currency risk is important enough that everyone should have some understanding of it. It is important to know what it is, the ways it can impact us, and what, if anything, we can do about it.

Currency Risk

Coincidentally, the year that Stanislav’s family moved to Russia was also the year of Russia’s 1998 financial crisis. In 1998, Russia’s economy was in a precarious position. At the time, Russia maintained a fixed exchange rate, and was struggling to maintain it at its lofty levels. Chronic fiscal deficits and low productivity undermined the country’s creditworthiness and stalled growth. Meanwhile, foreign exchange (FX) reserves were running painfully low, a result of the 1997 Asian financial crisis and a global weakening of crude oil prices. The situation was worsened when President Boris Yeltsin suddenly dismissed PM Victor Chernomyrdin and his entire cabinet on March 23, 1998, sparking a political crisis and further inflaming investor concern.

Capital began to flow out the country, gradually at first and then at an alarming rate. The central bank of Russia soon found itself unable to keep the ruble propped up and, on August 17, 1998, was forced to accept a massive devaluation. The ruble fell over 50% and Russia defaulted on most of its debt. As a result, inflation soared to over 80% for many goods. Asset prices collapsed. Overnight, it became much more costly to live in Russia.

Russia’s 1998 financial crisis is a good example of the potential pain that can be caused by dramatic shifts in exchange rates. When currencies fall precipitously, individuals lose their purchasing power, many companies go bankrupt because they can no longer pay their foreign-denominated debt, and countries can fall into recession. Conversely, when currencies spike dramatically, companies can become uncompetitive globally because similar foreign companies become cheaper to do business with, individuals can lose jobs, and whole industries can be hollowed out. In short, sharp moves in currency often bring about painful adjustments.

This is currency risk: the potential loss due to shifts in exchange rates. Theoretically, currency risk is the probability of any event that causes pain or loss because of fluctuating exchange rates. It could relate to the risks faced by an individual, a company or a country. For the purposes of this discussion, we will focus solely on the risks that can accrue to the individual.

Currency risk can negatively impact individuals in two important ways: (1) the loss of purchasing power, and (2) the impact on one’s investment portfolio. We have already seen the devastating results that can be caused from the loss of purchasing power in the example of 1998 Russia (and, as Canadians, we know how painful a low Canadian dollar can be when we want to plan a trip to the U.S.), so let’s take a closer examination of how it can affect an investment portfolio.

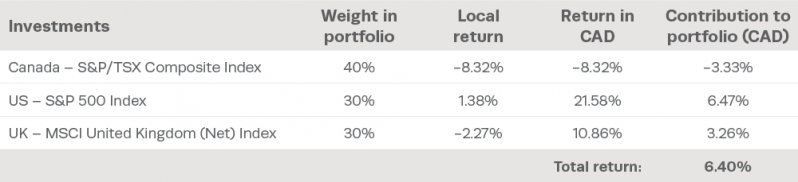

Let’s imagine that at the start of 2015 you, a Canadian investor, owned a portfolio comprised of equity investments in Canada, the U.S., and the U.K. Assuming an annual return equal to the index for each investment, your portfolio would have looked like this were the impact of currency to be excluded†:

Let’s compare this to returns when translated back to Canadian dollars:

† Local returns are calculated through FactSet Research Systems. The returns (both CAD and local) may not match other sources mainly due to different FX providers. The time period is January 1, 2015 – December 31, 2015.

Clearly, the quotational impact would be significant. In 2015, the dramatic fall in global commodity prices drove the Canadian dollar lower relative to the U.S. dollar and the British pound. An investor would have benefited from investing in U.S. and U.K. equities, in part because the returns generated in these markets outperformed the performance of Canadian stocks, but also because the U.S. dollar and the British pound outperformed the Canadian dollar.

Since currency fluctuations can have an impact on our portfolios, and more importantly, can constitute a risk to our purchasing power over time, how can we go about managing our exposure to exchange rates?

Know Your Ingredients

Just as a chef is much more likely to concoct a new recipe that is flavourful by understanding how ingredients work together, an investor will be materially better served by understanding some of the fundamentals of how exchange rates work.

In our team’s experience, it is helpful to view currency markets as systems: they have underlying structures, they contain players, and they are impacted by events. They even have forces that interact to drive the outcomes (price levels) we see.

The currency market system is both massive and decentralized. It is by far the largest market system in the world, dwarfing stock and bond markets in comparison (the market for USD is 27x larger than the U.S. stock market).1 At the same time, it is decentralized; there is no one global currency bank that clears all currency transactions. Instead, currency transactions happen among millions of players, all over the world.

Another observation we can make on this system is that it is complex. The currency market system is made up of millions of interactions. The agents that participate in this system include banks, corporations, investment funds, hedge funds, and central banks, among others. These players have their own individual purpose for transacting and usually hold a unique viewpoint on the market.

This system is also adaptive. Actors in the system react to other micro events that occur and also react to what other actors do. This results in collective and emergent behaviour. As an example, consider the adaptive qualities that emerged in the 1998 Russian financial crisis. When investors saw that capital was starting to flow out of Russia, many became nervous that the country would have a currency crisis. In turn, they began to sell their investments which put further pressure on the ruble, thereby increasing the likelihood of an actual crisis.

In summary, the currency market system is massive, decentralized, complex and adaptive. These important characteristics influence the way we must think about the system.

To Hedge or Not to Hedge

Now that we’ve outlined some of the most important characteristics of the currency market system, let’s return to the question of how investors may manage currency risk.

The most commonly cited solution for dealing with currency risk is hedging. The question is: does hedging make sense for most individuals if their primary concerns are protecting purchasing power and their investment portfolio? To spoil the punch line—probably not.

To see why this is the case, let’s examine what a hedge is in the first place. A hedge is a contract that changes who holds the risk of adverse price movements in an asset. In a hedge, the buyer pays a fee for the right to lock-in at a price they can buy or sell at a future date. The seller of the hedge takes the risk of the price movement.

For example, let’s say your child is going to a British boarding school in one year’s time. As the loving parent, you are on the hook for £20,000 in a year. Given that the current exchange rate is 1.89 per British pound, this means you will owe $37,800.

But what happens if the Canadian dollar continues its recent rapid descent and falls further to 2.50 per British pound? Then your liability would be $50,000.

To protect against this possibility, you could enter into a forward contract (the hedge) that gives you the right to buy British pounds in one year’s time at 1.89, so that no matter what happens to the exchange rate, you still pay $37,800. And you’ll pay a fee for this contract. This is why a hedge, in its simplest form, is also like an insurance policy. You pay a premium today to lock in a price.

Hedging makes sense when you know the amount and the timing of future liabilities. It can make sense to hedge for one liability at a future date. In the example above, you know the exact amount you will need in one year’s time for your child’s British boarding school, but not what it will cost you to convert your Canadian dollars into pounds. In this kind of situation, it could make sense to use a hedge to lock-in the amount you will pay.

It makes little sense to hedge when you do not know the timing or amount. This means that hedging makes little sense for investment portfolios, as the underlying investments are themselves exposed to multiple currencies and their own hedging programs.

As an example, consider how you would hedge an equity stake in Halma, a British company. Halma’s common shares trade in British pounds but its revenues and costs come from multiple currency sources. Moreover, Halma’s management team hedges some of its revenues already, but not all, so the “revenue” mix they report is muddled. It is difficult to successfully hedge against all these moving parts if you don’t know how much to hedge and when.

It is almost always impractical to hedge the cash flows of even one company in which you’re invested, and even more difficult for an entire portfolio. This is one of the reasons why our team has traditionally avoided hedging.

Another reason hedging is usually a poor solution for the individual investor is that we have far less grip on the potential direction of currencies than we think.

The Overconfident Doctor

I was lying on the doctor’s table in what one might call “peak discomfort.” A thin bed sheet of a robe covered my body and I shivered from the draft in the room. Nurses moved in and around me seemingly without notice. I was there for a biopsy, and I was visibly nervous, but I may as well have been a table lamp.

The doctor eventually came into the room and got down to business. As he proceeded to stick sharp, painful objects into my body, he inquired as to my occupation.

Stock analyst, I replied.

He looked up. In a moment I will remember for the rest of my life, he uttered Oh, looked down again, and proceeded to grill me on the U.S. dollar. It seemed he had some strong convictions as to the direction of the currency and was intent on telling me all about them.

As an investment professional, I have sometimes been cornered at dinner parties by those wanting a soapbox on which to proclaim their predictions about the world. But until that moment, I had never been forced to listen to these painful proclamations whilst simultaneously being poked and prodded with cold metal objects. This was new.

Predictions are made all the time concerning financial markets. Indeed, we make them all the time in our day-to-day lives. As Phillip Tetlock thoroughly examines in his book Superforecasters, each day, we make forecasts: it will be safe to cross the road now; there is no poison in my morning coffee; my spouse will pick up the phone when I call. We make these predictions because we need them to function, and often, they turn out to be accurate. But for all of the accurate forecasts we make every day, we make a lot of inaccurate ones too.

Arguably, the first step in making a prediction should be to consider whether it is even possible within the situation to make a good one. Some situations allow for good predictions to be made; others do not.

Returning to our earlier points, currency markets are complex and adaptive. They are like weather systems—difficult to predict, sometimes localized, sometimes widespread, and often volatile. In currency markets, the butterfly effect applies; meaning that there can be big outcomes down the line from seemingly innocuous events at an earlier date. This makes exchange rates very difficult to anticipate at any one point in time.

For example, let’s revisit last year’s surprise announcement by the Swiss National Bank (SNB) to abandon its peg to the Euro. At the time, the Swiss Franc (CHF) was pegged to the Euro at 1.20, a level that was probably too low given the surging demand for the Swiss Franc. In order to apply downwards pressure on the CHF and maintain the peg at its level, the SNB had been printing billions in Swiss Franc to sell in foreign exchange markets—thereby lowering the price. Eventually, the SNB deemed this intervention too costly and opted instead to abandon the peg. Overnight the CHF shot up 17% against the Euro.

This unilateral action surprised markets and had a significant impact around the world. Traders who had carry trade positions with the Swiss Franc, i.e., they had been borrowing in the low CHF currency and investing in higher returning currencies—were forced to unwind their positions. At the same time, anyone whose domestic currency was the Euro but was borrowing in Swiss Francs saw their costs increase by 17%! In fact, in an example of just how randomly connected our world has become, it caused a flurry of Polish loans to come under pressure. It seems that as many as half a million Poles had taken out mortgage loans in Swiss Francs hoping to benefit from the low interest rate environment.2

Neither investment professionals, nor my doctor, would have been likely to predict the announcement and subsequent consequences. And, given the complex and adaptive nature of currency markets, it wouldn’t have made sense to even attempt such a prediction.

That said, there are certain events that occur within the currency market system that we sometimes have the ability to forecast. There are times when we can associate probabilities around how an event will unfold, and then infer how these outcomes could influence the forces that drive currency. For example, when Russia lined up 40,000 troops on the border of Ukraine in 2014 and then proceeded to invade the country, our team noted that there was a decent probability that the international community would respond with economic sanctions. And given the likelihood of such sanctions, there was some probability that the Russian ruble would face downward pressure.

Of course, just because we made a forecast about the probability of sanctions, it doesn’t mean we had any ability whatsoever to predict the specific future price of the ruble. Our best guess was “down.”

This is an important distinction. In the currency market system, there are events and then there are prices. An event is something that happens that serves as an input, like economic sanctions against Russia. Events shape the different forces that drive exchange rates up or down. Another example of an event is if the Fed decides to raise interest rates.

While it can be difficult to forecast some of the events that would influence currency markets (because they are also often very complex), it is not altogether impossible. However, just because you might be able to predict an event’s occurrence, it does not mean that you can predict the reaction to that event. Participants in currency markets are still people—and people are unpredictable. While you may successfully predict that the Fed will raise interest rates, that doesn’t mean you know how the rest of the market will respond.

Even if you were able to anticipate an event AND be right about peoples’ reactions, you would be right generally. You would not be right specifically. You would still need to know everyone’s intentions and positions (exactly how much they intended to trade and when) and the assumption of zero “adaptiveness” to be able to reasonably predict an exchange rate level.

To further complicate our predictive ability, there are always many events unfolding all the time. Maybe you accurately predict that the Bank of Canada will raise interest rates and therefore that capital should flow into the Canadian dollar and lift it…but on the same day that they do, China’s financial system blows up and investors panic. Rather than be enticed by the interest rate hike, foreign investors see the commodity-rich Canadian economy as a proxy for a beleaguered China and they dump all their Canadian assets. You might have been right about an appreciating Canadian dollar had the hike happened in isolation. But in currency markets, there is no such thing as isolation.

Therefore, prediction within currency markets is hard and complex. This is often why it doesn’t make sense to hedge—it is difficult, if not impossible, to know where exchange rates will go precisely. It is also why a healthy degree of skepticism should be applied to anyone’s currency predictions.

Diversification and the 1/NTELLIGENCE™ approach

When hedging is not a very good option, how can individuals protect against the possibility of purchasing power loss and portfolio impact due to exchange rates?

At Mawer, the approach that we take to managing currency in the portfolio is what we call 1/N + Intelligence. This is an approach that recognizes that, with currencies, you rarely have any advantage in knowing how the outcomes will play out…and yet sometimes you do, i.e., the odds are clear enough for there to be a rational action to take.

What do you do when faced with uncertainty and a situation in which you don't have any advantage in knowing how things could play out? You diversify. Since diversification involves spreading your bets over multiple assets or investments, it means the portfolio is positioned for the possibility of multiple, and sometimes conflicting, scenarios. This is an appropriate strategy to take when we are ignorant of what is to come. Diversification is therefore our key starting point.

At Mawer, diversification begins with “1/N”, a simple approach that dates back several thousand years.3 For example, in the Talmud, it is suggested that men split their assets into 1/3 land, 1/3 businesses and 1/3 cash on hand. The idea behind 1/N is simple: hold equal weights in all the investments in your portfolio. In other words, if “N” is the number of assets that you own, then to get the weight you should hold in each investment, simply divide 1 by N. For example, if you owned Canadian, U.S. and U.K. equities in your portfolio, the 1/N approach would suggest you put one third of your capital into each.

If this seems like a rather simple approach, it’s because it is. It is also effective. Although there are many solutions proposed in modern finance that attempt to address how to determine weight investments in a diversified portfolio, 1/N is arguably the best foundation we’ve seen for dealing with uncertainty and many potential outcomes.4

However, it is not always the case that you are ignorant of how the future will unfold. Sometimes, we can have an understanding of the odds that makes it reasonable to act in a situation. While you rarely know how things will play out in currency markets, there ARE times when the probabilities would suggest you should act. This is why our team pursues a 1/NTELLIGENCE™ approach. When applicable (which is not that often) adjustments are needed—this is the intelligence component.

To get a sense for how this works, imagine that you need to plan a family picnic sometime next year. While the weather system is volatile and unpredictable day-to-day, there are still some decisions you can make knowing the odds. For example, it is probably better to plan your picnic in July than January. This is because of weather patterns. While we don't know for sure what the temperature will be like on any given day in July, it is reasonable to say it will likely be warmer than in January, not only because this is the inductive evidence we experience every year, but also because we deductively can reason that the pattern should persist into the future because of the way the Earth tilts towards the sun throughout the year.

Planning a picnic in July? Pick a time of year that makes sense and then bring an umbrella just in case.

At Mawer, we build portfolios that are diversified from a currency perspective. However, the weighting across the currencies is not the same. The weighting reflects a bottom up process that emphasizes securities with the best risk-adjusted return potential. It also reflects any views we may have on large downside risks we don’t think it is prudent to take.

In short, we don’t bet on currency predictions at Mawer. Instead, we reduce our vulnerability to potential currency risks by adopting this 1/NTELLIGENCE™ approach. While this mitigates our downside, it also limits our upside. But we are willing to accept that trade-off.

But what about protecting purchasing power? For that, we need to return to Russia.

From Russia, with Love

Growing up in Russia in the 1990s, one might assume that Stanislav and his family faced considerable economic duress. But the reality was different. Despite the hyperinflation, Stanislav’s family never really suffered at the time because they were protected by the earning power of their businesses.

Stanislav’s parents owned a very popular restaurant in Kazakhstan, and later, one in Russia. Lineups were so long they often turned people away. In fact, in Kazakhstan, they used a paid ticketing system: people had to buy a ticket just to get in the door and, on top of that, they had to also pay for their food—which was expensive. But this never seemed to deter their customers who were at the upper echelons of society and included judges, police chiefs, and politicians. These customers always had disposable income and they were willing to pay to eat and be seen at this exclusive restaurant.

The Lopata’s restaurants had a steady demand and were able to pass through exorbitant inflation without facing drops in volume. In other words, they had real earnings power. This gave them some insulation from the otherwise difficult environment.

Owners of businesses with real earnings power will often be okay in difficult economic environments. The earnings power of these businesses helps to protect them from negative events, including, for example, the potential loss of purchasing power due to risks like currency-linked inflation.

How do you achieve this if you aren’t an entrepreneur operating your own business like the Lopatas? You become an owner of many diverse businesses through your investment portfolio. The portfolio is the hedge. By owning a diversified portfolio of equities denominated in foreign currencies, you protect yourself against the potential loss of purchasing power due to rapid depreciation in your home currency (like what happened in Russia).

In sum, currency can play a major role in our lives. Yet exchange rates are difficult to predict and/or control, despite our tendencies to think we can. It is therefore important to select a strategy that takes this into consideration.

1 https://www.dailyfx.com/forex/education/trading_tips/daily_trading_lesson/2014/01/24/FX_Market_Size.html

2 http://www.reuters.com/article/poland-economy-swissfranc-idUSL8N14Z258

3 DeMiguel, Victor, Lorenzo Garlappi and Raman Uppal. Optimal Versus Naïve Diversification: How Inefficient is the 1/N Portfolio Strategy? Published by Oxford University Press on behalf of The Society for Financial Studies. 2007

4 Windcliff, Heath and Phelim Boyle. The 1/n Pension Investment Puzzle. North American Actuarial Journal:Volume 8, Issue 3, 2004

This post was originally published at Mawer Investment Management