Start talking about inflation risks again to clients

by David Allison, CFA, CIPM, CFA Institute

Three Reasons Why It Is Still a Good Time to Talk about Inflation

Finally! The fearmongers who loudly and incorrectly predicted hyperinflation after the financial crisis have crawled back into their caves.

This summer’s commodity swoon and the US dollar’s recent strength have helped beat down inflationary concerns in the United States to the point where they are almost nonexistent. But does this mean it’s time to put conversations about inflation risk on the back burner?

Questions like this illustrate a major flaw in the way many investors approach protecting their portfolios against inflation risk: Discussion starts only after rising inflation is already a problem and inflation hedges are expensive. Below are three reasons why now is a good time for investors and their advisers to talk about protecting portfolios from an unexpected dose of inflation.

1. The Importance of Managing Client Expectations

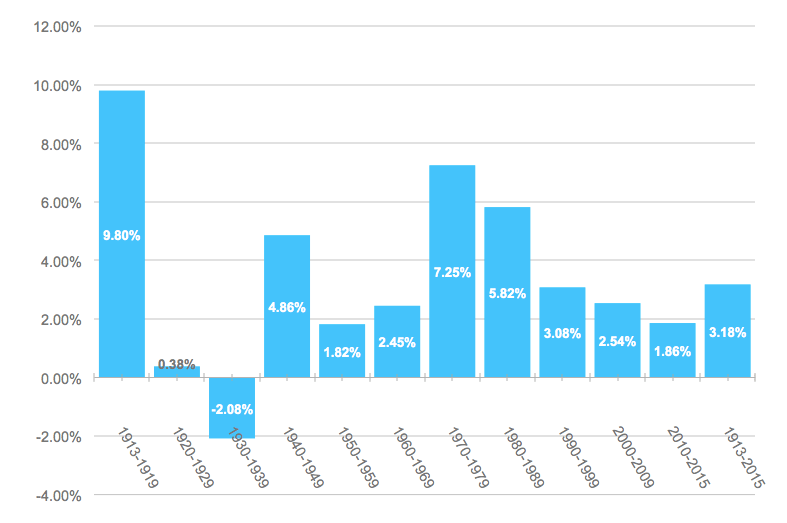

Investment advisers in the United States should consider that investors’ expectations about inflation and their corresponding willingness to own long-term bonds may be skewed by more than two decades of muted inflationary pressures. Research suggests that the most recent period of price stability has created complacency about inflationary risk — as investors who experienced the higher inflation rates of the 1970s and 1980s start believing high inflation is a thing of the past and newer generations of investors, who have never experienced elevated inflation levels, start to emerge.

Average Annual Inflation by Decade

Unexpected inflationary episodes pose a serious threat to investors by potentially altering the risk characteristics of their investment portfolio and reducing the purchasing power of their savings. For this reason, managing investor expectations about inflation risk is very important. Advisers should be clear when talking to investors about inflation in today’s environment. For example, vague statements, such as “I am not concerned about higher inflation,” may be misleading. Depending on past macroeconomic experiences, the investor’s definition of high inflation could be very different from the adviser’s. Also research indicates that people have a tendency to think about money in nominal terms, which means investors might underestimate the impact even a modest amount of inflation will have on their long-term purchasing power.

Regardless of where inflation is headed, it is always a good time for investment advisers to manage expectations by talking to investors about how different levels of inflation might affect the performance of their investment portfolio and financial plan.

2. Popular Inflation Hedges Are Historically Cheap

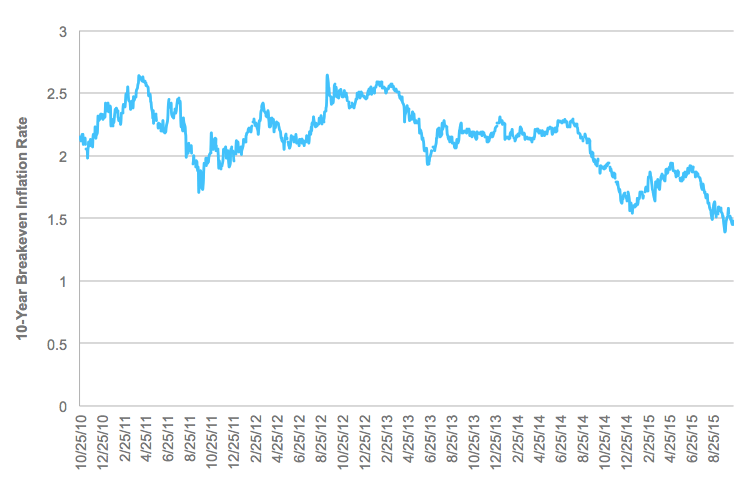

The best time to talk about buying protection is when no one else expects they are going to need it. The 10-year breakeven inflation rate, or the spread between the yield on a 10-year Treasury bond and the yield on a 10-year Treasury Inflation-Protected Security (TIPS), now stands at around 1.5%. This suggests bond investors expect the US inflation rate will average a paltry 1.5% over the next 10 years, which is below the long-term average inflation rate of around 3% and the Fed’s target rate of 2%.

10-Year Breakeven Inflation Rate over Time

The bond market’s multi-year low inflation expectations might spell opportunity in TIPS for investors who count hedging against an unexpected rise in inflation as part of their investment strategy. It is also worth noting that many commodities and commodity-related equities, which are popular inflation hedges, are currently trading close to multi-year lows.

3. Inflation Influences the Stock-Bond Correlation

For many investors, the allocation between stocks and bonds is the cornerstone of their risk management strategy. Fortunately, over the past few years, stocks and high quality bonds have tended to move in opposite directions, making bonds a powerful hedge during recent stock market sell-offs. But investors shouldn’t hang their hat on such a negative stock-bond correlation in the future, especially if inflation surprises to the upside.

Research shows that periods of negative stock-bond correlations have historically been short-lived and tend to occur when low and stable inflation is combined with uncertain economic growth and market volatility. This is similar to the environment investors have experienced for much of the new millennium. In contrast, the stock-bond correlation was mildly positive from the mid 1960s all the way to the late 1990s. During much of this period, inflation uncertainty dominated investors’ concerns and large changes in inflation expectations helped drive stock and bond returns in the same direction. For an interesting perspective on this period, check out Warren Buffett’s 1977 Fortune article, “How Inflation Swindles the Equity Investor.”

It’s always possible for inflation to heat up to a level where it becomes a top concern for investors. The hurdle for an inflation surprise is set low and an unexpected rise in inflation could eventually result in stocks and high quality bonds moving more in tandem. This risk is likely underappreciated by investors, especially after the negative stock-bond correlation of the recent past.

Conversations about inflation risk may be difficult to start in today’s economic environment. But investors and their advisers would be better served having a difficult conversation now, rather than a panicked one later. Inflation is still a credible risk that should be respected. An unexpected rise in inflation could alter the behavior of many unprepared investors at exactly the wrong time. Use the points above to start a conversation about inflation risk today.

What are some of the ways you address inflation risk in today’s economic environment? Please feel free to share your thoughts below.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

Please note that the content of this site should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute.

Image credit: ©iStockphoto.com/Mak_Art

Copyright © CFA Institute