It’s Not Easy

I’ll start this post with a quote from Howard Marks, who himself is quoting Charlie Munger. I never said I was original:

I’ll start this post with a quote from Howard Marks, who himself is quoting Charlie Munger. I never said I was original:

In 2011, as I was putting the finishing touches on my book The Most Important Thing, I was fortunate to have one of my occasional lunches with Charlie Munger. As it ended and I got up to go, he said something about investing that I keep going back to: “It’s not supposed to be easy. Anyone who finds it easy is stupid.” As usual, Charlie packed a great deal of wisdom into just a few words…

… what Charlie meant is this: Everyone wants to make money, and especially to find the sure thing or “silver bullet” that will allow them to do it without commensurate risk.

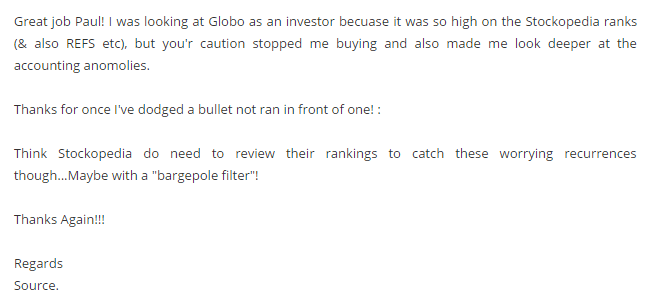

The talk of the town is the Globo situation. I have nothing to add on that front, so I won’t presume to try.

One thing I do like to watch, though, is investor behaviour in the wake of events. Many chalk losses up to bad luck, or attribute the blame to some external factor beyond their or the company’s control. Sometimes this is reasonable; often it is not. Others look to their process – how they are selecting securities – and then try to figure out what can be fixed to make sure they do not fall victim to the same mistake again.

This is a noble endeavour – a bit like the race driver who figures out, through repetition, that he needs to swing a little bit wider on the second corner to avoid clipping the dirt. There’s an appealing sense of progression in self improvement; a logic that, if you can just fix what you did wrong with every misstep, you’ll end up being a consistently profitable investor.

I think it is often a misguided one. A sample size of one is (almost) never large enough to make a decision on anything in life. This is not to say it is bad practice to try – a post mortem is often a good thing to do – but it is a mistake to put too much stock in said post mortem. Even the implication of the phrase ‘post mortem’ is false, seemingly implying that you should only think through your logic when it was ‘proven’ faulty. The fact is that the market, by its very nature, will make you wrong very often, and hopefully right slightly more often. Variance is large, and many of the winners will be winners for reasons you had not envisaged at the start. Whenever variance is large, you should treat every single data point with a large dose of scepticism and a sense of perspective. Stocks, being story driven, emotional and long-term in nature (if you’re a value investor with a decent time horizon) detract from the ability to keep that perspective.

On this vein, and as a curious observer of the discussions on Stockopedia, I noted a once-more recurring theme on many of the comments on the Globo saga. Stockopedia operate an algorithmic ranking system for stocks, whereby they rate stocks on three axes – value, momentum and quality. It trawls through the numbers and evaluates financial statements based on their similarities to a number of investing criteria which have outperformed in the past.

Unsurpisingly, Globo ranked highly on their algorithms. The headline numbers, falsified as they have now been proven, were fantastic. This leads people to ask the same questions they asked when Plus500 (another stock that ranked superbly) blew up:

These sorts of comments miss two fundamental truths.

Firstly – it is easy to fight the last war, and everyone trying not to look stupid does it. You can see this in broader markets when you consider the great efforts expended by regulatory organisations to tighten up banking systems post the financial crisis and ensure sufficient capital is available through future stress scenarios. The US have even tried to make a list of ‘systematically important financial institutions’ in the hope that identifying and imposing stricter rules will prevent another financial crisis. There will be another deep recession. It will probably not be caused by what people think it will be caused by, or what people are preparing for.

Secondly – the whole point of markets is that it is almost impossible to meaningfully profit from anything that is obvious. It is obvious, it has been priced in. You could eliminate the vast majority of dud companies with a strict set of criteria. Would it be profitable to do so? The answer to that question isn’t at all clear.

People, for perfectly understandable reasons, want one number to be able to capture everything about a company and sum up whether it is likely to be a profitable investment. When said number has a false positive, they want to fix the number to account for the error. This is a futile quest. You will end up fighting every last war, and progressively excluding more and more signal with your noise.

There really is only one answer, and it’s not really a very surprising one. You can screen, and you can use aids for finding companies to look at – ways of narrowing the ocean to a small pool in which you can fish – but you cannot outsource doing due diligence on an actual company. If you do decide to outsource said due diligence to an algorithmic screener – and for many investors (if only because most investors meaningfully underperform) this might be a good idea – what you absolutely cannot do is start to pick apart bad or good situations and try to second guess output based on that.

If not tinkering with the output of a screen sounds too light-touch to you – too hands off and unreliable – there is only one answer… actually engage in all the due diligence yourself.

Copyright © Expecting Value