It used to be said that "When America sneezes, the world catches a cold." Sometime later this century, maybe even 20 years from now that will probably be updated to "When China sneezes, the world catches a cold." But I don't see how we are there yet.

The domestic consumer economy is still 70% of US GDP. International trade only accounts for about 15% of GDP. So it should take a really, really major dislocation of that international trade to overcome domestic strength.

This morning's negative durable goods report is yet another reminder that the shallow industrial recession is real. Rail shipments are down YoY, truck shipments are down YoY, the regional Fed indexes are negative, industrial production and capacity utilization are down. That seems to have become widely accepted. I hasten to add that it showed up in February in the Weekly Indicators and has been there relentlessly since -- another reason not to wait for the lagging monthly reports.

At the same time, housing, cars, real retail spending and real personal consumption expenditures have continued to power ahead. And that is the problem for scenarios whereby the US imports a global recession.

I have read a number of articles over the last several months, including one this past week, all of which can be summarized as follows:

1. China is undergoing a downturn.

2. This has spread to China's suppliers, who are undergoing worse downturns.

3. ?????

4. This will bring about a US recession.

This is the "underpants gnomes" theory of how the US will import a global recession (if you don't know what this meme is, Google is your friend). None of the articles had any detailed or credible explanation of what step 3 is. It is all vagueness and hand-waving.

The weakness in the Oil patch, and generally in the industrial exporting sector will continue and will send ripples out into the wider pond, including layoffs and cutbacks in manufacturing, leading to I suspect one or more monthly employment reports that will be under 100,000 by the end of this winter.

But there is no reason to think that those ripples will be enough to overcome the positive ripples out from housing construction and vehicle production. And there is reason to believe that, contrary to expectations that the gas price dividend will peter out this fall, the US consumer is in the process of getting yet another boost, as gas prices are still over $.80 less than they were ago, and look like they will break below $2.02 (last January's bottom) before they seasonally bottom out this year:

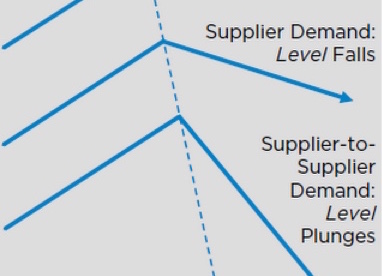

The below is a graphic I cribbed from ECRI. They used it to explain how a consumer slowdown to propagate into a supplier recession, but the converse is just as valid:

Until someone comes up with a credible scenario for Step 3, all we have is the Doomer version of the Underpants Gnomes.