A Bigger Brick in the Wall of Worries

by David Merkel, Aleph Blog

I have my list of concerns for the economy and the markets:

- Unexpected Global Macroeconomic Surprises, including more from China

- Student Loans, Agricultural Loans, Auto Loans — too much

- Exchange Traded Products — the tail is wagging the dog in some places, and ETPs are very liquid, but at a cost of reducing liquidity to the rest of the market

- Low risk margins — valuations for equity and debt are high-ish

- Demographics — mostly negative as populations across the globe age

- Wages in the “developed world” are getting pushed to the levels of the “developing world,” largely due to the influence of information technology. Also, technology is temporarily displacing people from current careers.

But now I have one more:

7) Nonfinancial corporations, once the best part of the debt markets, are beginning to get overlevered.

This is worth watching. It seems like there isn’t that much advantage to corporate borrowing now — the arbitrage of borrowing to buy back stock seems thin, as does borrowing to buy up competitors. That doesn’t mean it is not being done — people imitate the recent past as a useful shortcut to avoid thinking. Momentum carries markets beyond equilibrium as a result.

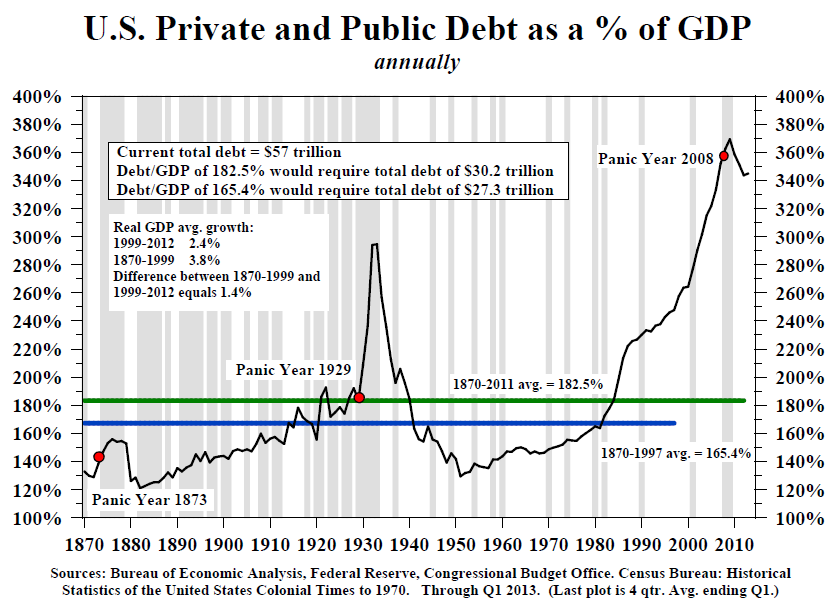

If the Federal Reserve stimulates by duping getting economic actors to accelerate current growth by taking on more debt, it has worked here. Now where is leverage low? Across the board, debt levels aren’t far from where they were in 2008:

As such, I’m not sure where we go from here, but I would suggest the following:

- Start lightening up on bonds and stocks that would concern you if it were difficult to get financing. How well would they do if they had to self-finance for three years?

- With so much debt, monetary policy should remain ineffective. Don’t expect them to move soon or aggressively.

- Fiscal policy will remain riven by disagreements, and hamstrung by rising entitlement spending.

- Long Treasuries don’t look bad with inflation so low.

- Leave a little liquidity on the side in case of a negative surprise. When everyone else has high debt levels, it is time to reduce leverage.

Better safe than sorry. This isn’t saying that the equity markets can’t go higher from here, that corporate issuance can’t grow, or that corporate spreads can’t tighten. This is saying that in 2004-2006, a lot of the troubles that were going to come were already baked into the cake. Consider your current positions carefully, and develop your plan for your future portfolio defense.

Copyright © Aleph Blog