Perspective on Recent Market Selloff Triggered by China Woes

Market Update With Portfolio Managers

by Tim Armour and Rob Lovelace, Capital Group

August 2015

Perspective on Recent Market Selloff Triggered by China Woes

Global stocks have tumbled in recent days amid investor concerns about slowing economic growth in China. A sharp decline in Chinese stocks and a surprise currency devaluation have further stoked fears that the outlook for China is deteriorating, and events there could hurt its global trading partners, including Japan, Europe and ultimately the United States. China lowered interest rates and eased reserve requirements on banks in an attempt to calm investors and stimulate the economy, and developed markets appeared to stabilize midweek. Against this backdrop, portfolio managers Tim Armour and Rob Lovelace share their thoughts on the unfolding events:

Global stocks have tumbled in recent days amid investor concerns about slowing economic growth in China. A sharp decline in Chinese stocks and a surprise currency devaluation have further stoked fears that the outlook for China is deteriorating, and events there could hurt its global trading partners, including Japan, Europe and ultimately the United States. China lowered interest rates and eased reserve requirements on banks in an attempt to calm investors and stimulate the economy, and developed markets appeared to stabilize midweek. Against this backdrop, portfolio managers Tim Armour and Rob Lovelace share their thoughts on the unfolding events:

• China now accounts for roughly 15% of the world’s gross domestic product and therefore has a greater impact than ever before on the global economy.

• The most significant catalyst of the selloff was China’s unexpected decision to devalue its currency, delivering a shock to financial markets.

• Developed economies with significant trade links to China — including Australia, Hong Kong, Japan and Europe — must deal with the potential decline in export activity.

• Offsetting some of these negatives are lower oil and commodity prices, as well as potentially lower interest rates, which could provide a boost to the global economy.

What are your thoughts on the recent market volatility sparked by China?

Tim: We’ve had a six-year bull run in the U.S. and rising markets in most other parts of the world. The U.S. markets were fairly valued and valuations were stretched for some companies and sectors. So this market correction is not unexpected. Having a correction periodically is healthy for the markets, as it removes pockets of excess.

Rob: U.S. stocks have had a strong run. There has been a bit of a “hope” rally in Europe and Japan, though emerging markets haven’t had much of a rally at all. That’s a big difference compared to before the 2007–09 global financial crisis. All areas of the global capital markets have not rallied indiscriminately. That is why I think this correction is not a repeat of the global financial crisis, but rather more akin to the market downturns we experienced in 1994 and 1998.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. 1

What are your views on the U.S. economy and interest rates?

Tim: The U.S. economy is not growing as strongly as many expected in the second half of the year. The data has been mixed. Even then, the expectation has been that the Federal Reserve will increase interest rates sooner rather than later. My view is that the Fed still needs to go ahead with raising rates, because near-zero interest rates lead to investors taking undue risk. It will be healthy for the economy over the long term for short-term interest rates to gradually start moving higher. It directs capital flows to areas where there are adequate returns and it allows banks to earn some interest margin, which contributes to a stronger financial system.

Was China the real catalyst in this market selloff, or was it a combination of factors?

Rob: In my view, it is primarily China. For a while, China was the only piston firing in a global economic engine that includes the U.S., Europe, Japan and all the other emerging markets. Until about three years ago, China’s economy was growing rapidly. It was the only major economy to power right through the financial crisis and keep on moving forward. Then the U.S. economy started to pick up and, for a time, there were two major economies contributing to global growth. The hope was that Europe and Japan would follow. We haven’t seen solid evidence of that yet. So when China started to slow down, you can see why investors reacted very negatively.

So, yes, I think events in China definitely triggered this market selloff. If China goes from slow growth to no growth, or a real recession, then that will have a very real negative effect on the global economy. As the second-largest economy in the world, China’s impact is much bigger today than it ever has been. By comparison, at the height of the Japanese “economic miracle” in the 1980s, Japan accounted for less than 10% of global gross domestic product. Today, China accounts for roughly 15% of world GDP. That is why concerns about China are spilling over into other parts of Asia — especially Japan — as well as Europe and ultimately the U.S.

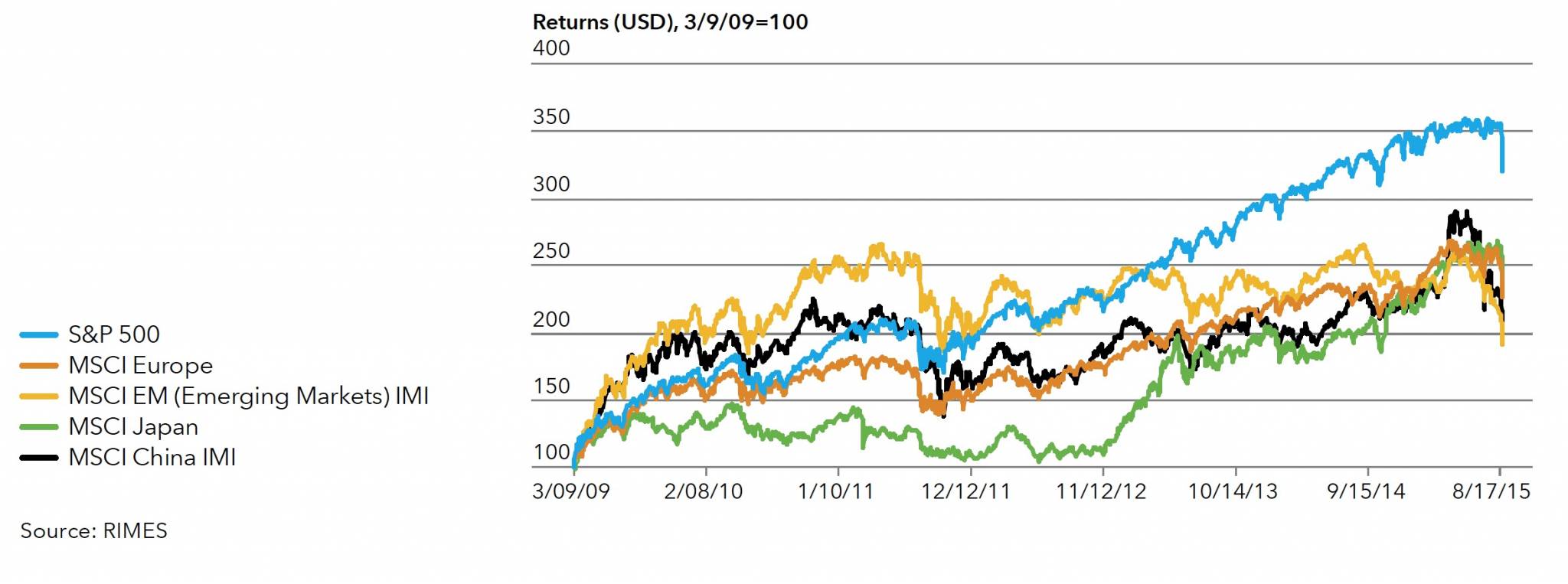

Stock Markets Have Risen Significantly Since Their 2009 Low.

The recent market selloff needs to be seen in a longer-term context. Despite short-term volatility, equity markets tend to make significant gains over longer periods. Returns (USD), 3/9/09=100

How much did the decline in China’s A-share market and the recent currency devaluation play into the global market selloff?

Rob: The A-share market is not a major part of this story. I think the rally in A-shares was driven by speculation about them being included in certain market indexes, and when they were not, the A-share market pulled back. The much bigger issue has been currency weakness in a number of emerging markets, and the decision by China’s leadership to devalue the renminbi. It was a surprise move and it spooked the market. China had to adjust its currency downward to be more competitive — but the timing, on the back of the A-share declines and a slowing economy, was viewed as a defensive move, and it made investors wonder if economic growth was actually worse than expected. That’s what unsettled markets.

What impact do you think these events in China will have on the financial system overall, and on companies that do business in China?

Rob: So far, this appears to be a market correction. We have not seen any signs of stress in the global banking system that would indicate that it is a financial crisis.

Since its financial system is tightly controlled and essentially closed, China actually does have the ability to manage a full-blown financial crisis within its own borders and not have it spill over to the rest of the world. The nodes of financial contagion are somewhat limited, but it is difficult to predict. We’ve never seen such a large, controlled economy go through a powerful cycle like this, so it is tough to say how much of it will spill over and how much of it won’t. It is important for China to undergo a correction. No economy grows without bumps, and in China, many of the excesses are getting cleaned up, including the excesses in credit.

As for the impact on specific companies, I think that is somewhat less complicated. So far, the market hasn’t been totally irrational about which companies have been hit. If you take into consideration how important China is to each company — analyze their income statements and assume a full-blown recession — I think the price decline has been reasonable.

Given the reforms that China has to implement and the challenges it faces, and given its role in the global economy, should we expect sentiment to turn anytime soon?

Tim: I see this as growing pains of an economy that is transitioning from a closed, investment-led economy to a more open, consumer-led economy. Given that China’s government still controls most of the levers — the banks, monetary and fiscal policy, many of the companies — it makes it difficult to use the tools used to analyze a classic, open- market developed economy. So we should be prepared for this transition to be rocky, but also use the turbulence to invest in strong companies along the way.

Rob: It reminds me of what many investors were saying at the bottom of the global financial crisis — that it would be a decade-long deleveraging cycle, and it could take up to 20 years in the U.S. because that is where the crisis began with the excesses in the housing and mortgage markets. It actually makes me more confident that we are getting near the bottom because of the pessimism we are hearing around China.

If China as a whole is not consuming as much as it did a few years ago, of course, it will have an impact on Japan and Europe, given how much they export to China. It will also have an impact on commodities and commodity-exporting countries like Brazil and Australia. We should remember that China’s role as an incremental buyer has been decreasing over the last few years and it’s been OK. Are there specific areas of opportunity amid this selloff, both within China and outside it?

Tim: One obvious area is the Chinese Internet companies. They are world-class companies and today their valuations look more attractive on most parameters relative to other large Internet companies, especially those based in the United States. They were at much higher valuations recently and the correction has taken them to levels where they may present opportunities.

What about the multinational companies that derive a large part of their revenues from China?

Tim: Although China’s economic growth rate is slowing, I expect that it will still be faster than many developed economies, and so the multinationals should continue to grow sales in China, and they will manage the cycle and the opportunity.

How should investors think about global and international funds in the current environment?

Rob: These situations when we are most fearful are generally the moments of greatest opportunity. In 2009, when the market was at its bottom, nobody wanted to buy. Even as it started to recover, people were not confident that quantitative easing was going to work, that the U.S. would find its way out of its troubles. No one thought that U.S. stocks would touch new highs within a few years. But that’s how it unfolded. We must go back to basics, which is that companies continue to produce goods and services that we need in our lives. For instance, airlines are running pretty full. More people are traveling and airlines have not added that much capacity.

Elsewhere, what’s happening right now in biotechnology is a once-in-a-lifetime phenomenon. The molecules that are being developed are very significant, with the potential to significantly improve the quality of life. Those are the types of trends we tend to stay focused on.

Tim: The financial system, especially in the developed economies, is much stronger than before the crisis. Capital ratios are much improved for the U.S. and European banks, and troubled assets on their books have been scrubbed and cleaned.

So we view this period of volatility as an opportunity. We have investment professionals around the world that can use this period to invest in strong companies at attractive prices.

Copyright © Capital Group