by Jesse Felder, The Felder Report

“It just doesn’t matter.” This is the mantra of the bulls who, no matter what bearish evidence is presented, simply insist, “earnings don’t matter. Valuations don’t matter. Margin debt doesn’t matter. Market breadth doesn’t matter.” You name it and they defame it. I was recently told by a bull who was dead serious that, not only do none of these things matter, there is an invisible magical force more powerful than any of these them which ensures stocks will continue to march higher. I was dumbfounded.

These are only a small sampling of the refrains from the “it just doesn’t matter” chorus that is the rallying cry for all the bulls buying even the slightest dips in the stock marketright now. I actually agree with this sentiment much of the time. Certain aspects of the market or individual indicators like these don’t usually matter to the market, as they say, until they matter. But when is that? Ironically, I believe that they typically begin to matter just when everyone begins to believe that they won’t matter ever again (just another version of “this time is different”) – which is right about now.

It’s simple contrarianism at work. The more popular an idea or chart becomes the less likely it is to “work.” Take the popularity of “sell in May,” for example. It’s become so popular over the past few years that it’s just stopped working. Ironically, now that the bulls begin to mock the concept it may just start to work again. The same goes for, “[fill in the blank] doesn’t matter.” As soon as everyone begins to believe something doesn’t matter to the markets, the markets will shortly prove them wrong.

So let’s take a look at each to see how they actually might begin to matter to the stock market today. As Fred Hickey recently wrote, even respected strategists like Well Fargo’s John Manley insist earnings don’t matter. This can be true over the short run when the market is a voting machine. However, over the long run, as Ben Graham famously said, the market is an earnings weighing machine. But even over the short run, the market is constantly assessing and discounting the future growth of earnings:

The chart above shows that slowing future earnings growth doesn’t currently matter to the market but that this is also a rare divergence that is likely to be rectified sooner rather than later. (If the forward p/e were to catch up the decline in estimated earnings growth, as indicated in the chart, stocks would fall about 35% fairly quickly.)

The Financial Times recently ran an article insisting valuations don’t matter. This is something I hear from naysayers all the time. I guess this just depends on your methodology and time frame. Pure trend-followers care nothing about valuations nor do short-term traders. For everyone else, though, valuations are the best possible measure of potential risk and reward and are very highly correlated to future returns. The simple fact that it is so popular to deny this iron law of the markets may be the greatest contrarian warning signal there is.

It’s also become popular to defame the concept of market breadth. Breadth simply measures the participation rate of a given trend and assumes the trend is strongest when there is the greatest degree of participation. Waning participation in a trend is sign that it’s losing momentum. There are many ways to measure breadth and I believe the greater variety used, the more meaningful the message.

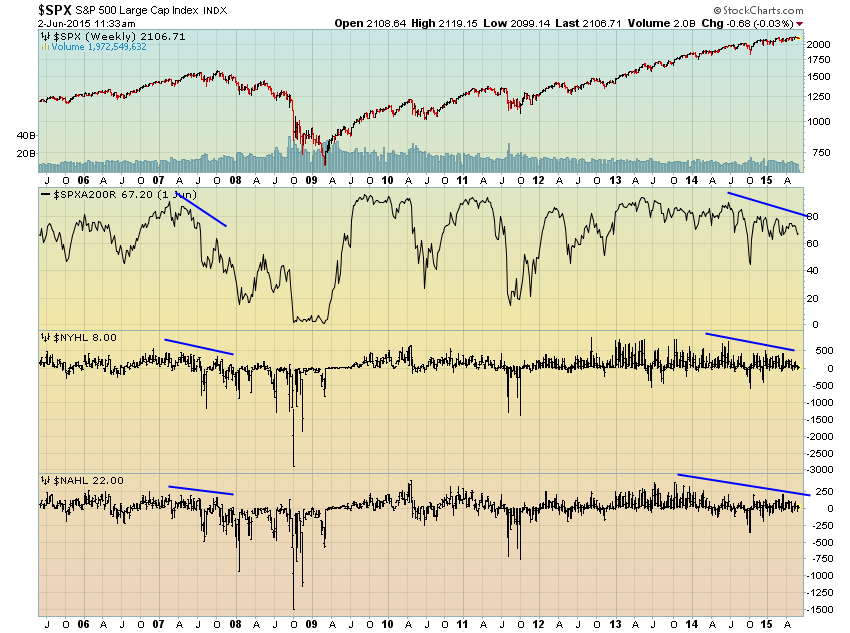

The chart below shows the S&P 500 along with the percentage of stock trading above their own 200-day moving averages and new highs and new lows on the New York Stock Exchange and the Nasdaq. Individually, these indicators are not very effective. When all three begin to wane in the face of rising stock prices, however, it has been a bad sign for stocks going forward.

Additionally, bond market risk appetites and volatility are both diverging from stocks at this point, too.

It’s easy to argue any one of these is not very meaningful on its own. Each can send many “false positives,” as my friend Jason Goepfert likes to say. Having said that, when they all point the same way, it’s hard to make the case that they “don’t matter.” In the past, this has been a very clear sign that stocks are running out of steam. Again, the fact that it’s become popular to deny this truth is a sign that it could be about to prove its worth once again.

Dow Theory is another concept related to market breadth that has been widely dismissed recently. I wonder, however, if those dismissing it have seen this Nautilus study. Over the past 50 years we have only witnessed a similar divergence between the Dow Industrials and the Transports on two prior occasions. Those marked the stock market peaks of 1973 and 2000.

Finally, a few popular bloggers have recently published pieces claiming margin debt is another useless metric. The common response to the famous margin debt chart is, “that’s been true for years and it hasn’t mattered.” Saying margin debt doesn’t matter is the very same as saying that supply and demand don’t matter to an asset’s price. It’s asinine. Nothing matters more to price than supply and demand!

As a clear indication of potential supply and demand for stocks margin debt is absolutely critical to prices. Extreme levels of margin debt clearly indicate very little potential demand left for stocks and very high potential supply and vice versa.

From a purely statistical perspective, margin debt is very meaningful. As I recently wrote, margin debt relative to GDP is very highly correlated to future 3-year returns in the stock market. In the past, the current level of margin debt has led to stock market declines of about 60% over the coming 36 months. Once again, the fact that it has now become so popular to dismiss margin debt as meaningful means that we are likely approaching a tipping point.

I just can’t stress enough how the sentiment surrounding an indicator can be far more important than the indicator itself. I have found this to be especially true with chart patterns. The more eyeballs there are on a given pattern the less likely it is to work. A chart pattern is most effective when it is ignored, dismissed or simply missed by the masses.

Right now the masses are ignoring, dismissing or simply missing a wide variety of meaningful signals suggesting the stock market is likely in the process of forming a major top. To me, this makes these signals that much more poignant.

Copyright © The Felder Report