Well stocks appear to be ready to see some fresh air as many major indices are testing prior highs or have already broken out. When this type of price movement happens the first thing I do is turn to the market internals and measures of risk taking to see if there are signs of confirmation. I’ll dive into some of these today in this Technical Market Outlook.

Trend

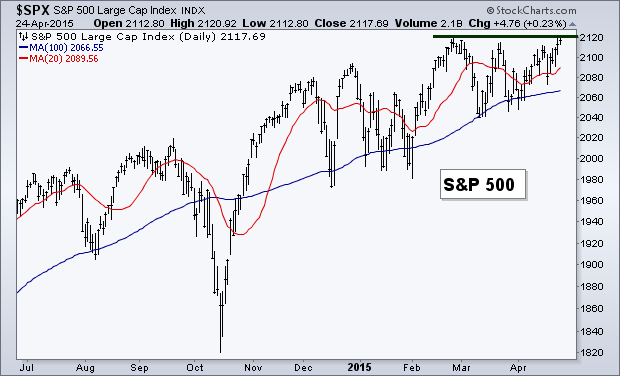

What better place to start than the trend of the S&P 500 ($SPX). For the bulk of 2015 we have seen this major U.S. index rise and then quickly fall back to its 100-day Moving Average before making another attempt to advance. Each move created a slightly higher high and higher low, which is positive for trend followers, albeit the progress has been slow and choppy.

Small(er) Caps vs. Large Caps

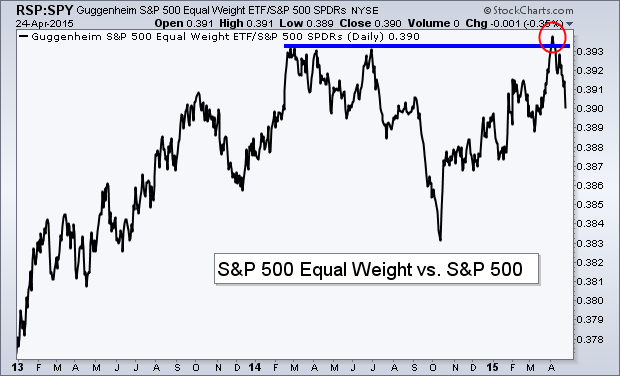

There are different ways to look at the ratio between small and large cap stocks. How you define ‘small’ is the key. In this chart I’m not looking at actual small caps but the smallest stocks in the S&P 500 ($SPX). The cap-weighted index is often controlled by what the largest of its holdings does. This can hide what the majority of the stocks are doing and in turn, not revealing any possible signs of weakness. By looking at the ratio between the Guggenheim S&P 500 Equal Weight ($RSP) and the cap-weighted SPDRs S&P 500 ($SPY) we can see which one is leading, the larger portion of the index or the smaller capitalization companies.

In this chart we can see that the ratio between RSP and SPY has created a false breakout of its prior high set in 2014. When the black line is rising the smaller cap stocks are leading the overall index, a possible notion that traders are taking on more risk as they show preference for smaller company’s stocks. As the S&P 500 is just a few points away from a new high, the smaller portions of the index are beginning to drag.

Breadth

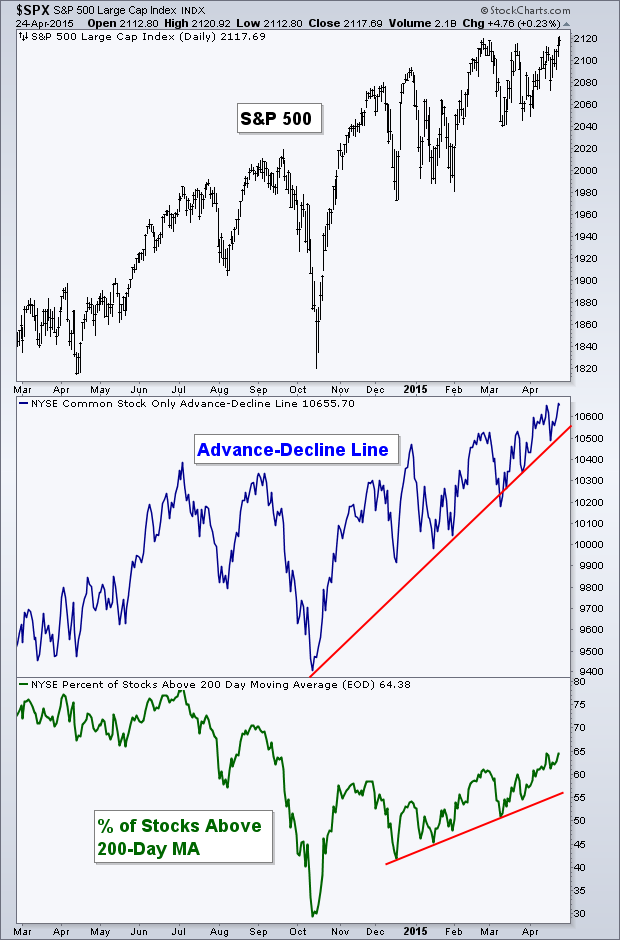

Breadth

One of the more bullish charts for the advance in stocks right now is that of the Advance-Decline Line, a measure of breadth for the market. The Common Stock-Only NYSE Advance-Decline Line has continued to confirm the up trend in U.S. stocks. The A-D line for the S&P 500 also is very close to breaking out like its respective index. The Percentage of Stocks Above Their 200-day Moving Average has also made good progress as it digs itself out of the down trend that had been created. While not near its high, this breadth indicator has begun an up trend of higher lows and higher highs. From a breadth perspective, things appear positive for stocks.

Commodities vs. Treasury’s

Commodities vs. Treasury’s

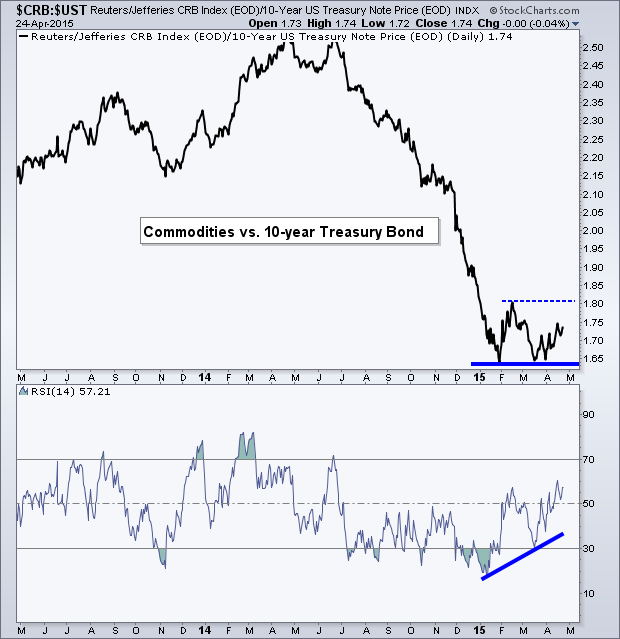

Back in December Jeffrey Gundlach did a webcast calling TIPS (Inflation-protected securities) for losers. A few days later Bill Gross did an interview with CNBC and said TIPS looked like an attractive opportunity. Once again, the Doubeline bond manager appears to be on the right side of this call as inflation has declined over the last several months. One way we can chart inflation is through the relationship between commodities and Treasury’s.

If commodity prices are rising at a faster pace than bonds, then it’s believed that inflation is also on the rise. As you can see from the ratio chart below, commodities have been under-performing the 10-year Treasury bond since early 2014, However, it seems we may be seeing a possible double bottom in this relationship, which would favor commodities over Treasury’s. At the same time momentum via the Relative Strength Index (RSI) is creating a positive divergence by putting in a higher low.

I’ll be watching to see if the ratio between $CRB and $UST is able to break above its prior high at 1.80. If this happens then we may begin seeing signs of inflation re-introducing itself. What would cause this? That’s not my concern nor on my radar. All I know is this setup may turn to be bullish for commodities after the terrible performance they have had over the last year.

Momentum

While Breadth looks bullish for stocks, momentum has been unable to produce the type of movement we’d like to see. The daily Relative Strength Index (RSI) remains in a range between 60 and 40. The MACD indicator also has been making a series of lower highs. If the S&P does rise and high a new high this week, it will unlikely be accompanied by momentum which will cause many traders to pause.

Semiconductor’s

One of my most widely shared posts was on the significance of Semiconductor’s and how they have replaced Copper as an indicator of risk-taking for the market. I was fortunate enough to have it published in the Market Technician Association Newsletter as well as the Chart of the Day at Bloomberg.

As the global economy becomes more technologically focused the market has shifted from industrial materials to ones found in just about every electronic created – semiconductors. This is why I believe this index is important to watch for signs of confirmation in equities. Up until the last few months Semi’s had been marching instep with the S&P 500. But that has changed as they are well off their high as the S&P tests its own high – creating a bearish divergence. This has historically not been a great sign for stocks. Some of the previous downturns in U.S. markets have been led by this type of lack of confirmation in semiconductors. Are we approaching the same kind of weakness?

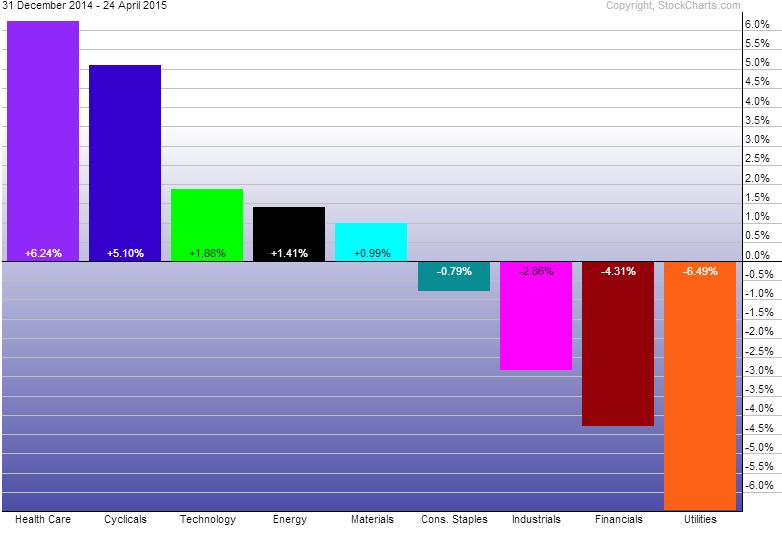

Year-to-Date Sector Performance

2015 has continued to repeat ’13 & ’14 with strength coming out of the Health Care ($XLV) sector. Consumer Discretionary (Cyclicals) ($XLY) also have been performing well as they are the second best performing sector YTD. Utilities ($XLU) and Financials ($XLF) are the two worst performers so far this year.

Disclaimer: Do not construe anything written in this post or this blog in its entirety as a recommendation, research, or an offer to buy or sell any securities. Everything in this post is meant for educational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in the blog. Please see my Disclosure page for full disclaimer. Connect with Andrew on Google+, Twitter, and StockTwits.

Copyright © Andrew Thrasher