Many Investors Still Fear Stocks: Good News for Markets?

The economy and the stock market are no longer depressed, yet the share of U.S. adults who own stocks remains at multi-year lows. Russ explains why investors haven’t yet fully embraced equities and what this could mean for longer-term stock market performance.

by Russ Koesterich, Portfolio Manager, Blackrock

During the bull market of the last five years, U.S. stocks, as measured by the S&P 500, have generated total returns of 233%. So, you would think most investors would be embracing equities.

But while stocks represent a larger share of household financial assets than they did five years ago, the share of U.S. adults who own stocks remains stuck at multi-year lows.

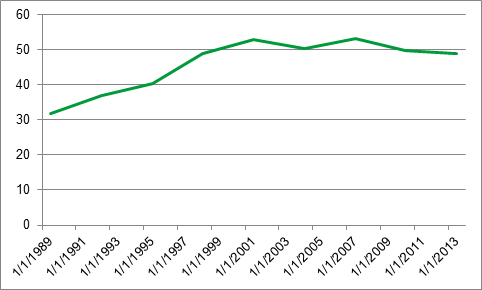

At the beginning of September, the Federal Reserve (Fed) published its 2013 edition of the Survey of Consumer Finances. Even as the S&P 500 was closing in on 1,600 last year, well above its March 2009 lows, the report revealed that the share of U.S. households holding stocks actually declined to 48.8% in 2013 from a high of 53.2% in 2007, as the chart below shows.

The Share of U.S. Households Holding Stocks

Source: Fed Survey of Consumer Finances

Similarly, Gallup surveys also show a decline in investor stock holdings. According to these polls, during the decade before the financial crisis, roughly 60% of U.S. adults held stocks in their financial portfolios. But since the bull market kicked in five years ago, that ownership share has averaged around 55% – among the lowest ownership percentages since the survey began in 1998.

This shouldn’t come as much of a surprise. Factors that explain the reticence to embrace stocks include:

- Two stock market routs in a decade have altered investors’ return and volatility assumptions for the asset class, as well as their preference for risky assets. This is especially true among 30- to 50-year-old investors who haven’t had the benefit of experiencing more stable market conditions during their investing lifetimes.

- The Fed’s bloated balance sheet and unusually accommodative monetary policy have created a sense among some investors that the subdued expansion may be somewhat artificial.

- High government debt levels as a share of U.S. annual economic output, combined with concerns over long-term entitlements and U.S. political dysfunction, have led investors to focus on potential cracks in the economy’s foundation.

- Geopolitical risk and worries about the economic outlook overseas have convinced otherwise optimistic investors to take a more guarded stance.

- Stubbornly high levels of structural unemployment and wide gaps in incomes limit the universe of potential savers who can own stocks.

To be sure, the Fed’s Survey of Consumer Finances data is from last year. To the extent that equities have continued to move higher since then, it’s possible that stock ownership has gone up since the end of 2013.

At the same time, while the Gallup data and the Fed’s survey data show declining stock ownership since the peaks in 2000 and 2007, Americans still own far more stock than they did in the late eighties and early nineties when equity investing was just becoming more widespread.

In addition, when you look just at the first decade of the millennium, equity holdings appear more static. Despite two market crashes during that period, the share of investors holding stocks barely cracked.

So, what’s behind the longer-term trend toward more equity ownership as well as the static stock holding levels during the aughts?

- Strategic asset allocation frameworks, which form the core of modern wealth management, generally call for at least some exposure to stocks, except in the most conservative portfolios.

- Historically low interest rates make government bonds appear much more expensive than stocks, also implying a lower discount rate for stocks and thereby supporting prices.

- Investors looking to save for – and generate income during – retirement may see stocks as a necessary investment in a low-yield world.

The upshot is that the longer-term shift toward equities coupled with the more recent caution among investors could actually be good news for markets.

U.S. equities are clearly more fully valued these days, but they’re not in a bubble. Though many Americans today remain cautious and unwilling to increase their equity holdings, the fact that more U.S. investors haven’t lost faith in stocks suggests that there is further upside potential for equity markets, assuming continued economic expansion, modest earnings gains and even normalization of Fed policy. As such, I continue to expect that global stocks can move higher this year, and I prefer them to cash and bonds.

If Americans’ ownership of stocks were nearing a prior peak, I might be concerned. But with that not the case, my concern is that more Americans aren’t participating in today’s rally.

Russ Koesterich, CFA, is the Chief Investment Strategist for BlackRock and iShares Chief Global Investment Strategist. He is a regular contributor to The Blog and you can find more of his posts here.

Kurt Reiman is a Global Investment Strategist at BlackRock who works directly with Russ Koesterich. He contributed to this post by providing research and investment insights.

Sources: Linked to throughout Post, BlackRock research

©2014 BlackRock, Inc. All rights reserved. iSHARES and BLACKROCK are registered trademarks of BlackRock, Inc., or its subsidiaries. All other marks are the property of their respective owners.

iS-13573

Copyright © Blackrock