Fed Model, Buybacks, and M&A (excerpt)

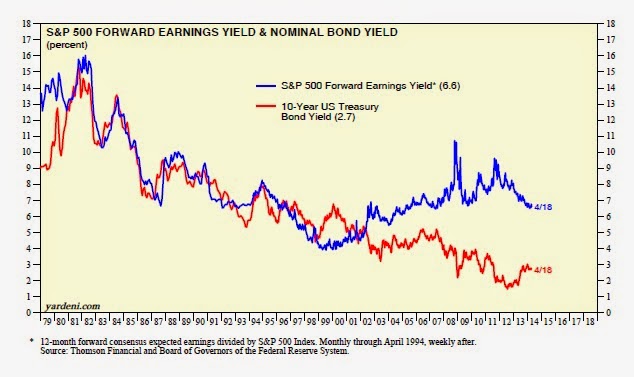

Previously, I’ve argued that as long as the forward earnings yield of the S&P 500 exceeds the corporate bond yield, buybacks are likely to continue. This is a variation of what I called the “Fed Stock Valuation Model (FSVM),” which I discovered buried in the Fed’s Monetary Policy Report of July 1997. It showed a close fit between the earnings yield and the 10-year Treasury bond yield from 1982 through 1997. That’s just about when the model stopped working as a useful investment tool. It did show that the S&P 500 was overvalued during the late 1990s. But it has been significantly undervalued ever since then according to the model, which never gave a sell signal in 2007 or 2008. (See the Wikipedia article on the Fed Model.)

The model has been more useful for explaining corporate financial behavior. The corporate finance yield spread between the S&P 500 forward earnings yield and Moody’s seasoned Aaa corporate bond yield has been positive since 2004 and is currently 237bps. When it is positive, company managements can get a better return on their cash by repurchasing their shares than by investing it in fixed-income securities.

Alternatively, their companies can benefit by borrowing the money to buy back some of the company shares. Last year, nonfinancial corporations’ net new issuance of bonds totaled a record $640 billion. Some of those proceeds funded buybacks. (Although the Aaa yield applies to only a handful of corporations, it is pre-tax. So it should still be a good proxy for corporate borrowing rates after taxes, in my opinion.)

The corporate finance version of the FSVM suggests that companies can also benefit by using their cash or borrowed money to fund M&A when the forward earnings yield of the combination exceeds the corporate bond yield.

Today's Morning Briefing: M&A Mania? (1) Here we go again. (2) Fed Model not a good market timing tool, but it does explain corporate buybacks. (3) Forward earnings yield vs. corporate bond yield. (4) Companies using inflated stock prices as M&A currency. (5) Software and R&D accounting for more of capital spending. (6) Macroeconomic vs. microeconomic models of inflation. (7) Competitive model explains a lot. (8) Yellen’s tools aren’t working. (9) Stocks should grind higher this year. (10) So far, 2014 is reminiscent of 2013, when defensive stocks outperformed until the end of April. (More for subscribers.)

Copyright © Dr. Ed Yardeni