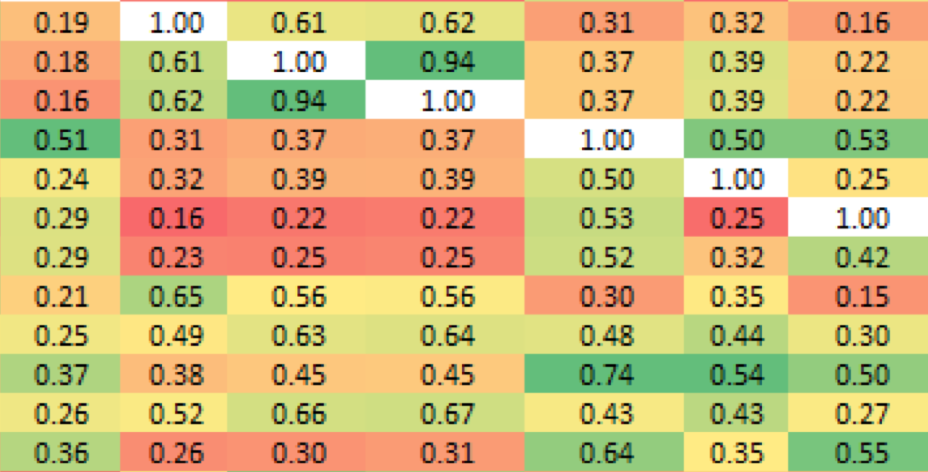

The grid below is a correlation matrix of most major stock markets around the world. It quickly shows the correlation of daily returns between any two country stock markets, and it's heat-mapped to show which countries are most or least correlated with each other. There are two matrices shown: one for the period from the start of the US bull market to present and one for the last year. So...what does it all mean?

Correlations give us an idea of how similarly two markets perform. For instance, since the start of the bull market, Canada and the US have had a 0.78 correlation. This implies that if one market is up 1%, the other would usually be up by about 78 basis points. The more positive the correlation, the more likely the two indices will move together. A correlation of zero would imply that there is no relationship between two markets, while a correlation of -1 implies that when one market moves up by 1%, we could expect the other to be down by 1%. It's important to note that these aren't absolute statements! Correlations measure past relationships over periods of time, and aren't by any means an absolute predictor of what happens on any given day in the future, now, or in the past. They are an indication, not a definitive statement.

Looking at the first matrix, there are a couple of notable patterns. First, the US has very few "middle of the road" correlations: only three countries have correlations between 0.60 and 0.30. The correlation between the US and Canada is one of the highest of any pair of countries on the map, and 9 countries have correlations above 0.60 with US stocks. The US is least correlated with Asian markets; China-US and Japan-US are two of the three least correlated markets on the grid.

Generally speaking, correlations are highly regional; Australia's most correlated markets are Hong Kong, Japan, Singapore and South Korea, all of which are also developed Asia-Pacific markets. Meanwhile, the UK is most correlated to other European markets such as France, Germany, Spain, Sweden and Switzerland. The three most-correlated pairs are all European and specifically English: UK-France, UK-Germany, and UK-Switzerland.

Please click the image below to enlarge.

The second matrix paints a slightly different picture from the longer-term matrix above it. In aggregate, the average correlation of this matrix falls from 0.46 to 0.40 when looking at the more recent time frame instead of the whole US bull market. We see this as a healthy move, as higher correlations imply a world driven more by binary outcomes: "risk on" when policy makers intervene to end a crisis and "risk off" when another one rears its ugly head. Improvement in Europe (we view the Ukrainian crisis as a temporary speed bump, not a serious threat to the region like periphery issues in Spain/Italy/Greece were), stabilization in Washington DC, and Chinese financial market liberalization (even with the temporary uptick in volatility it brings) are all positive steps forward from where the outlook was five years ago. The single largest decreases in correlation between the entire bull market and just the last year are US-Brazil (-0.28), US-Mexico (-0.25) and Switzerland/UK-Brazil (-0.21). Broadly speakng, Asia-Pacific markets have decoupled from the Western Hemisphere, with correlations between Japan and Brazil or Malaysia and Brazil as low as 0.01 and 0.03 respectively; meanwile most major Western markets such as Canada, France, Germany, the US, Spain, and Switzerland have a correlation in the single digits with China.

China's economy has deccelearted recently, and its returns have been the worst of any major stock market over the course of the bull market (see this chart from our bull market anniversary post). Meanwhile most of the developed world has been on a massive rally. Whether the drop in Asia-Pacific correlations will continue is largely dependent on China and Japan. If China can stave off a financial crisis (likely, in our view) and Abenomics is ultimately succesful (less likely), we may see correlations rise from these low levels in the future.

Copyright © Bespoke Investment Group