Submitted by Lance Roberts of Street Talk Live blog,

The recent one month spike in interest rates, along with the mind numbing chatter about the end of the "bond bull market," has sent investors scurrying from from the bond market right into the waiting arms of a stock market correction. Besides being suckered into stocks at the market peak; individuals continue to overlook the significance of fixed income to an overall, long term, portfolio allocation model. Fixed income reduces portfolio volatility, protects principal (bonds mature at face value) and generates an income stream that contributes to portfolio performance. The most important reason to own a bond is that when it is purchased the exact rate of return can be immediately calculated to maturity. This rate of return can be very efficiently modeled into the expected rate of return a portfolio should generate over time. This is absolutely something that can not be done with a portfolio of other investments that are subject to the volatility of the stock market.

However, the recent spike in interest rates has certainly caught everyone's attention and begs the question is whether the 30-year bond bull market has indeed seen its inevitable end. The following is 5 reasons why I do not think this is the case and, from a portfolio management perspective, I believe this is a prime opportunity to increase fixed income holdings in portfolios.

International Intrigue

Money hides in U.S. Treasuries for safety when global risks are rising. As I discussed recently in "Is The Euro-zone Crisis Set To Flare Up?" there are currently many promises that have been made to the financial system by the ECB. The question is whether or not they can ultimately "cash the check." I said then that:

"While I do not have certain answers as to the where, the who or the when - I am fairly confident that it will be sooner than we currently imagine."

With yields spiking in the Euro-zone, China showing cracks on its financial front and Greece funding being threatened by the IMF it is likely that we will begin to see a rotation of excess reserves and investment dollars back into the "safe haven" of U.S. bonds to reduce default risks.

Economic Weakness

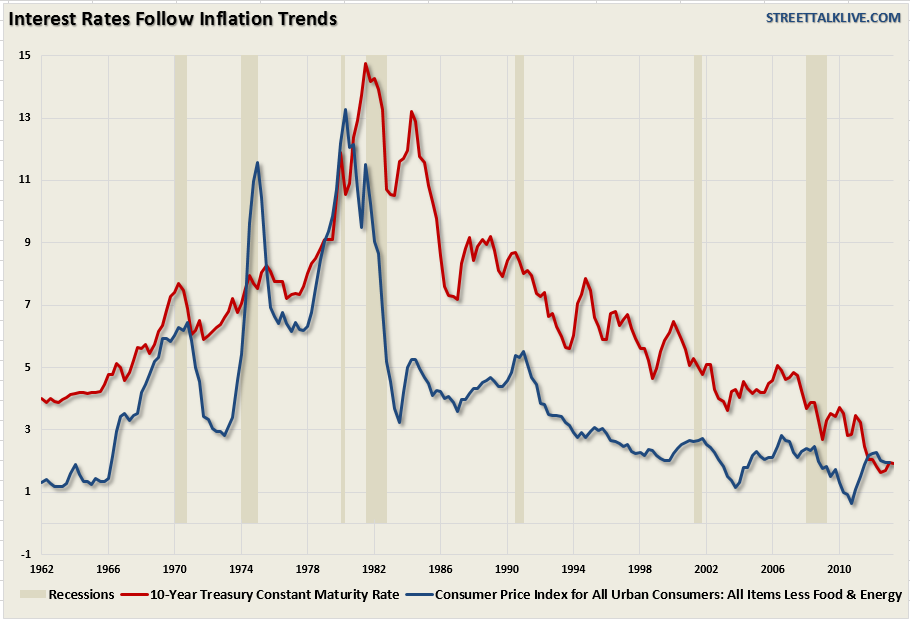

Another positive for U.S. bonds, which coincides with the international front, is domestic economic weakness. Weaker economic growth will weigh on the stock market as earnings growth continues to deteriorate which, in turn, will likely make the relative safety of bonds much more attractive. Despite much commentary to the contrary history shows that interest rates tend to follow the strength, or weakness of the broad economy. The chart below shows the annual rate of change for 10-year treasury rates and real GDP.

Dis-Inflation

While the Fed currently has a target of 2% on inflation, so does Japan, it doesn't mean that the have any real control over inflationary pressures in the market. Inflation is ultimately a function of economic activity, employment and production and wages. As I discussed just recently in "Deflation: The Fed's Real Worry" the Fed's biggest fear is the negative economic impact of deflation. The headwinds facing the economy currently are structural in nature and are not something that continued rounds of liquidity injections have been able to fix.

As shown in the chart above interest rates tend to follow inflation. While interest rates have spiked in the last month, a move that has the Fed "more than a little baffled", the decline in both current inflation, as well as future expectations, will likely keep a lid on interest rates through the remainder of this year.

As shown in the chart above interest rates tend to follow inflation. While interest rates have spiked in the last month, a move that has the Fed "more than a little baffled", the decline in both current inflation, as well as future expectations, will likely keep a lid on interest rates through the remainder of this year.

Political Showdowns

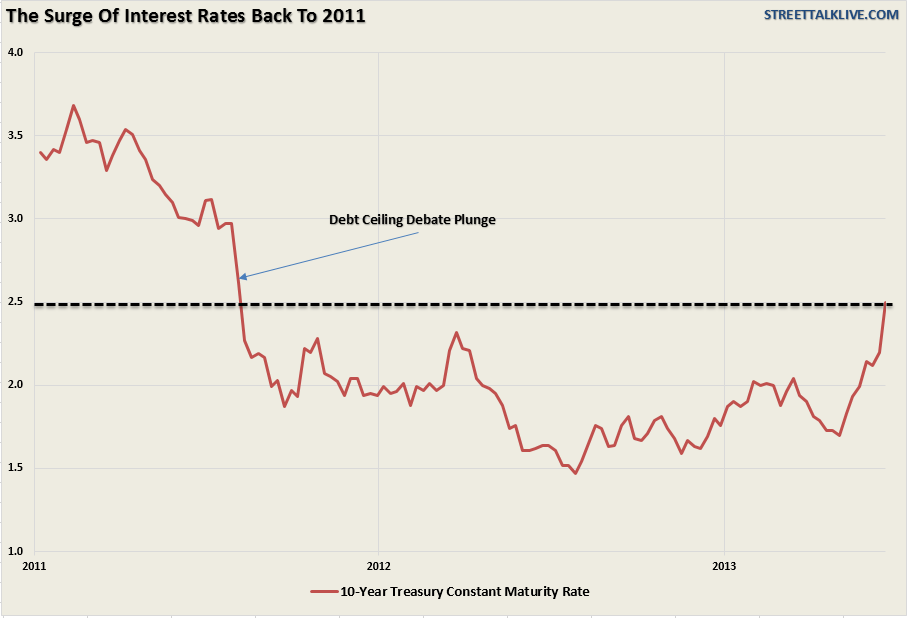

Coming soon to a "kabuki" theater near you will be the second annual revival of the "debt ceiling debate." While I am not suggesting that we will have an exact repeat of the 2011 debacle - it is quite likely that IF the threat of "debt default" begins to surface, once again, interest rates will fall as money seeks a "safe haven" against political turmoil. The chart below shows what happened to interest rates in the summer of 2011.

The recent surge, while it has been quite dramatic, has only returned interest rates back to where they were just two short years ago. With the debt ceiling debate once again looming, the Euro-crisis simmering, Japan faltering and China showing cracks in their financial armor there is only one real place left for the world to store their excess reserves in "safety."

Technically Opportunistic

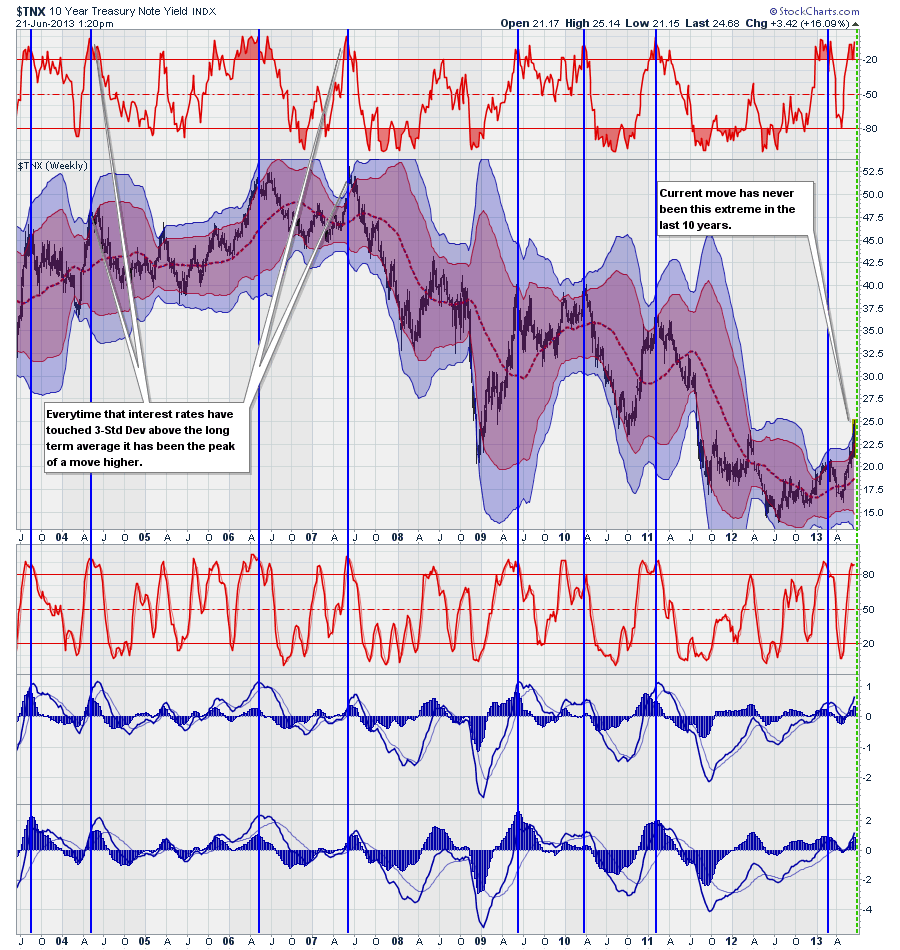

Lastly, despite all of the other commentary and rhetoric in the market as of the last month, interest rates are pushing extreme overbought levels. The chart below shows a weekly chart of interest as compared to its long term moving average. Currently, at more than 3-standard deviations overbought, the level of interest rates is unsustainable and a correction is in order. In the chart I have noted (vertical blue lines) every time that the 10-year interest rate has touched 3-standard deviations above the long term mean. In every single case, over the last 10-years, that was the absolute peak of the move higher. It is unlikely to be "different this time."

With a downside target of 1.8% currently, which is simply a retracement to the mean, there is a fairly low risk entry point for bonds at the current time. Furthermore, if the recent market "sell signal" is validated it is likely that interest rates could fall as low as 1.5%.

Bonds Look Cheap

For all of these reasons I am bullish on the bond market through the end of this year. Furthermore, with market volatility rising, economic weakness creeping in and plenty of catalysts to send stocks lower - bonds will continue to hedge long only portfolios against meaningful market declines while providing an income stream.

Will the "bond bull" market eventually come to an end? Yes, it will, eventually. However, the catalysts needed to create the type of economic growth required to drive interest rates substantially higher, as we saw previous to the 1980's, are simply not available currently. This will likely be the case for many years to come as the Fed, and the administration, come to the inevitable conclusion that we are now in a "liquidity trap" along with the bulk of developed countries. While there is certainly not a tremendous amount of downside left for interest rates to fall in the current environment - there is also not a tremendous amount of room for them to rise until they begin to negatively impact consumption, housing and investment. It is likely that we will remain trapped within the current trading range for quite a while longer as the economy continues to "muddle" along.

Copyright © Street Talk Live blog