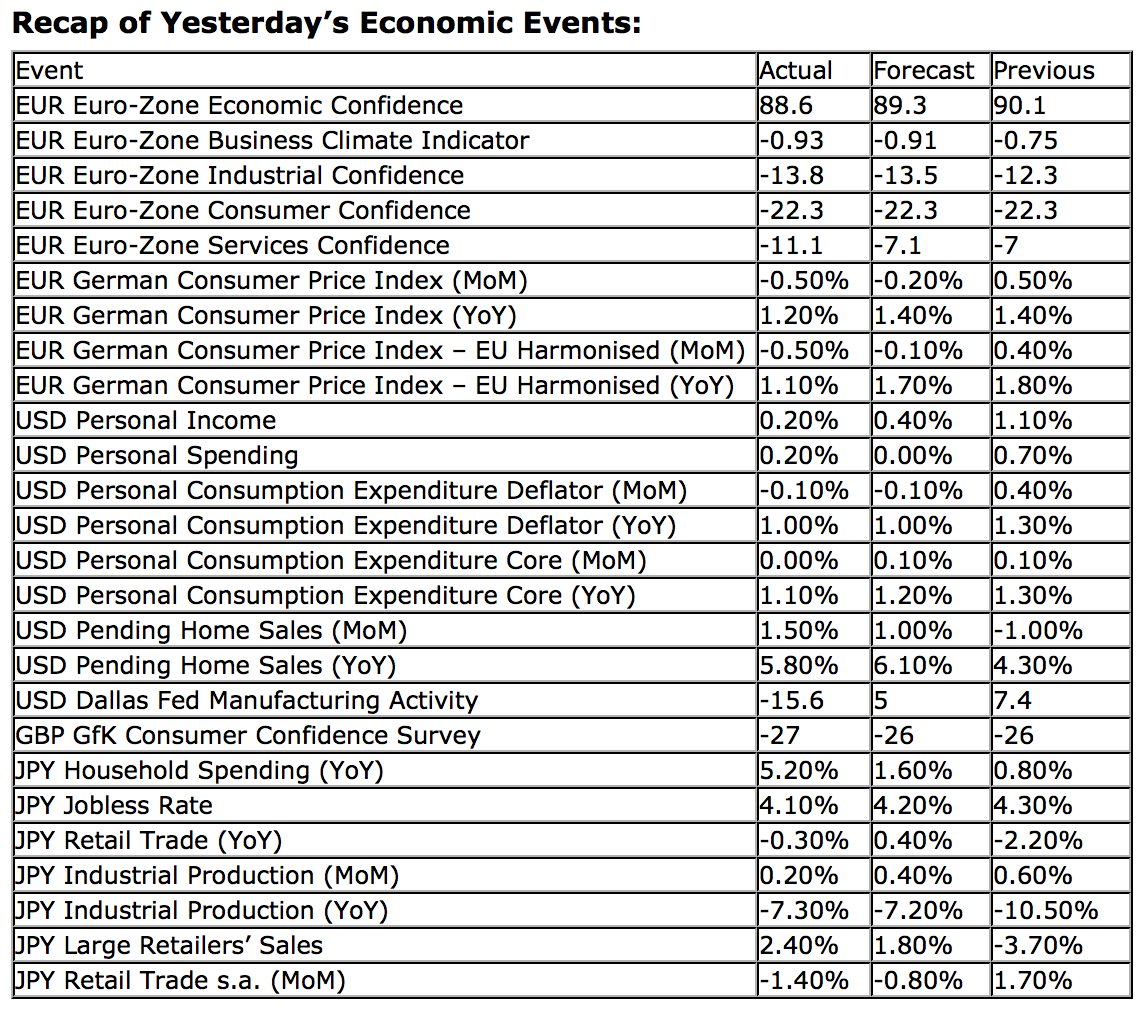

by Don Vialoux, Tech Talk

Upcoming US Events for Today:

- The FOMC Meeting Begins.

- The Employment Cost Index for the First Quarter will be released at 8:30am. The market expects a quarter-over-quarter increase of 0.5%, consistent with the previous report.

- Case-Shiller 20-city Index for February will be released at 9:00am. The market expects a year-over-year increase of 9.0% versus an increase of 8.1% previous.

- Chicago PMI for April will be released at 9:45am. The market expects 52.4, consistent with the previous report.

- Consumer Confidence for April will be released at 10:00am. The market expects 62.0 versus 59.7 previous.

Upcoming International Events for Today:

- German Retail Sales for March will be released at 2:00am EST. The market expects a year-over-year decline of 1.2% versus a decline of 2.2% previous.

- German Unemployment Rate for April will be released at 3:55am EST. The market expects an increase of 2,000 versus an increase of 13,000 previous. The Unemployment Rate is expected to hold steady at 6.9%.

- Euro-Zone Consumer Price Index for April will be released at 5:00am EST. The market expects a year-over-year increase of 1.6% versus an increase of 1.7% previous.

- Euro-Zone Unemployment Rate for March will be released at 5:00am EST. The market expects an uptick to 12.1% from 12.0% previous.

- Canadian GDP for February will be released at 8:30am EST. The market expects a year-over-year increase of 1.3% versus an increase of 1.0% previous.

- China Manufacturing PMI for April will be released at 9:00pm EST. The market expects 50.7 versus 50.9 previous.

The Markets

Equity markets posted strong gains to start the week, supported by strength in the technology sector and continued speculation that the ECB will enact a rate cut at it’s next meeting, which is set to take place on Thursday. The NASDAQ Composite closed at the highest level in over a decade, while the S&P 500 closed at the highest level on record. The large-cap index, however, failed to chart a new intraday high above 1597.35, emphasizing the significance of this level as a point of resistance. Daily volume on Monday was one of the lowest this year, suggesting conviction to the positive session was lacking.

We’ve been reporting for a number of weeks now that equity market momentum is on the decline. This is obvious when looking at simple technical indicators, such as RSI and MACD, which are diverging from the recent price action of equity benchmarks, such as the S&P 500. Another indicator to gauge momentum is the number of stocks charting new 52-week highs. Since the peak in January of 896, this indicator has been on the decline, now at 275, providing a warning signal of a pronounced correction ahead. Over the past three years, three other similar instances have been recorded whereby the number of new 52-week highs have negatively diverged from the price action of the broad equity market. Each scenario resulted in a market correction of between 7% to 20% shortly thereafter. Unless momentum improves, the expectation is that a correction of similar magnitude is imminent, likely to correspond with the seasonal risk-off period that begins in May, on average.

Seasonal charts of companies reporting earnings today:

Sentiment on Monday, as gauged by the put-call ratio, ended bullish at 0.90.

S&P 500 Index

Chart Courtesy of StockCharts.com

TSE Composite

Chart Courtesy of StockCharts.com

Horizons Seasonal Rotation ETF (TSX:HAC)

- Closing Market Value: $13.46 (up 0.60%)

- Closing NAV/Unit: $13.45 (up 0.31%)

Performance*

| 2013 Year-to-Date | Since Inception (Nov 19, 2009) | |

| HAC.TO | 5.75% | 34.5% |

* performance calculated on Closing NAV/Unit as provided by custodian

Click Here to learn more about the proprietary, seasonal rotation investment strategy developed by research analysts Don Vialoux, Brooke Thackray, and Jon Vialoux.

Copyright © Tech Talk