Caveat Depositor

by Eric Sprott & Shree Kargutkar, Sprott Asset Management

“If there is a risk in a bank, our first question should be: ‘Ok, what are you the bank going to do about that? What can you do to recapitalise yourself?’ If the bank can’t do it, then we’ll talk to the shareholders and the bondholders. We’ll ask them to contribute in recapitalising the bank. And if necessary the uninsured deposit holders: ‘What can you do in order to save your own banks?’” – Jeroen Dijsselbloem, March 26, 2013 1

A deal has just been struck with Cyprus. However, it was not the deal that Cyprus saw other countries receive. This was not the deal received by Greece, Italy and Spain. There were no bailed out banks in the aftermath. There was no transfer of risk from over-levered banks to the taxpayers. The risk was pushed back onto the banks. Their equity was wiped out. Their bondholders were wiped out. Their uninsured depositors saw their accounts raided for additional liquidity. It wasn’t just that the rules of the game had changed, the game itself changed. By raiding the depositors’ accounts, a major central bank has gone where they would not previously have dared. The Rubicon has been crossed. Going forward, this is expected to be the “template” for dealing with risky, over-levered banks and the countries which support them.

For the first time since the crisis began, we are faced with a new paradigm, or a “template”, for how a major central bank will address weakness in the financial sector. While the old template involved “bailing out” through transfer of risk from the corporate sector to the taxpayer, the new template calls for “bailing in”, whereby the risk is contained within the affected institution at the expense of equity holders, bond holders and finally the depositor.

How does the new template affect you?

This “template” is already being applied to the “too big to bail” banks in other developed countries around the world. A statement in the joint paper published by the FDIC and the Bank of England in December 2012 reads:

“An efficient path for returning the sound operations of the G-SIFI to the private sector would be provided by exchanging or converting a sufficient amount of the unsecured debt from the original creditors of the failed company into equity. In the U.S., the new equity would become capital in one or more newly formed operating entities. In the U.K., the same approach could be used, or the equity could be used to recapitalize the failing financial company itself—thus, the highest layer of surviving bailedin creditors would become the owners of the resolved firm…. Such a resolution strategy would ensure market discipline and maintain financial stability without cost to taxpayers”.2

Note the lack of the phrase “uninsured depositors” in this context, which opens the doors for both insured and uninsured depositors to be affected. In a similar vein, Canada’s recently released budget addresses the same problem. Page 144 of Canada’s Economic Action Plan 2013 reads:

“The Government proposes to implement a – bail-in regime for systemically important banks. This regime will be designed to ensure that, in the unlikely event that a systemically important bank depletes its capital, the bank can be recapitalized and returned to viability through the very rapid conversion of certain bank liabilities into regulatory capital. This will reduce risks for taxpayers.”3

Likewise, New Zealand’s Open Bank Resolution policy allows for a “bail in” of afflicted banks by wiping out the equity holders first, the bond holders second and finally forcing a haircut on the depositors.4

Over-levered banks are not a recent development. We are faced with a banking crisis, seemingly once every generation. In a majority of cases, the bad banks were allowed to fail and newer, stronger banks took their place. However, the recent modus operandi of the central banks and policy makers allowed over-levered banks to get even bigger, rewarded risk taking with bailouts and let the inherent problem of unsustainability fester.

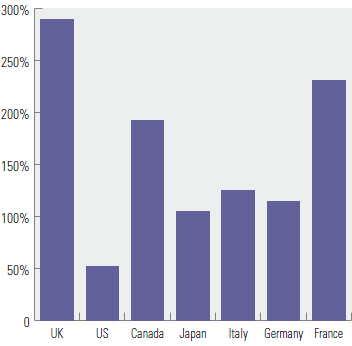

CHART 1: BANKS ASSETS – COUNTRY GDP

Source: Capital IQ, CIA Factbook

We carried out the exercise of taking the largest banks, or in other words, the “too big to fail” banks in the G7 countries and added up their assets in relation to the host country GDP. For the layperson, a typical bank’s assets are primarily composed of the loans they have originated while the liabilities are primarily composed of deposits they have accepted. With the exception of the US, all G7 countries have banking systems that have become larger and in some cases dwarfed their respective economies.

Governments around the world are finally beginning to realize the gravity of the risk that exists in their banking sectors. The EU has decided to build upon the new template of the “bail-in” regime. The US, UK and Canada have all followed suit. This puts the onus squarely upon the depositor. The depositor is a lender to the financial institution that he banks with. However, most depositors naively assume that their deposits are 100% safe in their banks and trust them to safeguard their savings. Under the new “template” all lenders (including depositors) to the bank can be forced to “bail in” their respective banks. Several G7 countries already have provisions that allow troubled banks to be bailed in using depositor accounts. We have been vocal about our concerns over the state of the global financial system for the better part of the decade. The Greek tragedy is now being played out in Cyprus with a new twist as depositors have been unwillingly turned into sacrificial lambs. Given the size of the banking sector in most G7 countries and the burgeoning government debts, the ability of the governments to bail out their banks is severely constrained, especially considering the political headwinds that exist today. For this reason, we strongly believe that real assets trump a fiat currency in a “savings” account. It is not our intention to be alarmist here, merely to say, “caveat depositor”.

Footnotes:

1 Import Export Stats – US Census Foreign trade: http://blogs.ft.com/brusselsblog/2013/03/the-ftreuters-dijsselbloem- interviewtranscript/

2 http://www.bankofengland.co.uk/publications/Documents/news/2012/nr156.pdf

3 http://www.budget.gc.ca/2013/doc/plan/budget2013-eng.pdf

4 http://www.centralbanking.com/central-banking/official-record/2257939/rbnzarticle-

says-open-bank-resolution-helps-keep-banks-in-line

Copyright © Sprott Asset Management