by Carl Tannenbaum, Northern Trust

As expected, this month’s forecast was a little more difficult to assemble. The influence of severe storms on economic activity and economic data made it harder to discern fundamental trends. Activity lost in the current quarter will likely be made up in future quarters, but the timing of recovery remains unclear.

The winds of change to the tax code have been wafting through Washington recently. While we still do not expect major changes to the system this year, or even next, the mere possibility has had an important impact on long-term interest rates. We’ve adjusted our expectations accordingly.

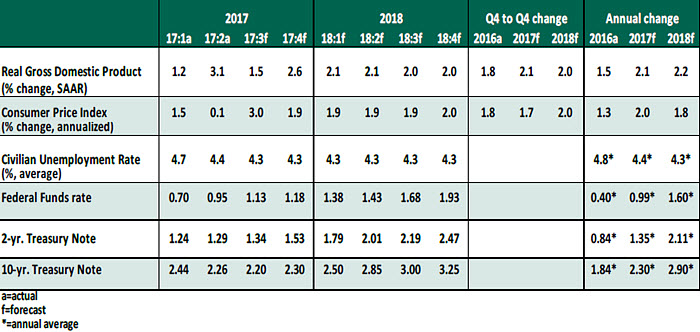

Key Economic Indicators

Influences on the Forecast

-

- We’ve reduced our estimate of third quarter growth to account for the damage done by Hurricanes Harvey and Irma. We expect to recoup the lost economic ground in the current quarter; real gross domestic product should expand at a 2.6% annual rate during the final three months of the year.

-

- Job and wealth creation continue to be strong supports for consumer spending and background for a modest degree of re-leveraging. Inventories need to be rebuilt. And the dollar has weakened since the spring, which should favor U.S. exports.

-

- The September employment report was deeply distorted by the storms that coursed through Texas and Florida. In the “establishment” survey, payrolls fell by 33,000 last month, the first such decline in more than seven years. Employment in the leisure and hospitality sector fell by more than 100,000 positions, clearly reflecting hurricane-related disruption. Fortunately, these losses should be temporary.

-

- The “household” survey showed much less interruption. The nation’s unemployment rate fell to 4.2%, the lowest level in 17 years. The labor force participation rate increased to 63.1%, highest since 2014.

-

- Wages jumped unexpectedly. Hourly earnings now stand 2.9% over their reading of a year ago, a high for this expansion. Those rooting for the Phillips curve to reestablish itself should be cautious, though; some workers may have received a temporary boost in their compensation for their assistance in hurricane recovery efforts. And those idled by the weather skew toward the lower end of the pay scale. Nonetheless, the most recent report included upward revisions to wage growth in July, which pre-date the storms.

-

- Manufacturing continues to accelerate. The Institute for Supply Management (ISM) index rose to 60.8 last month, highest in 13 years. (On the ISM scale, a reading of 50 separates advance from decline.) The auto industry has seen a sharp increase in demand, as families in Florida and Texas replace vehicles lost or damaged.

-

- Inflation took another step back last month. Price increases for a range of services continue to moderate; the core personal consumption expenditure (PCE) deflator is only 1.3% higher than it was a year ago. Overall price measures will show a brief burst in the third quarter because of a temporary increase in energy prices, but that movement should be quickly retraced.

-

- Despite the benign inflation readings, the Federal Reserve appears likely to raise interest rates again in December. The Fed’s consensus forecast shows inflation approaching the 2% target next year; concerns about financial conditions may also provide grounds to remove accommodation. Central bank speakers have sounded somewhat hawkish. Odds on a December hike have increased from 25% to 75% in the last month.

-

- After falling close to 2% at the beginning of September, the yield on the 10-year U.S. Treasury note has since risen by 30 basis points. The main impetus for the move was the budget discussions in Washington, which appear to reflect a reduced degree of deficit discipline. The Fed’s gradual balance sheet reduction will also release additional supply for private investors to absorb.

But with global demand for U.S. government bonds expected to remain strong, we do not expect a substantial increase in long-term rates during the forecast period.

The Atlantic hurricane season still has seven weeks to run. Let’s hope that the worst is past, both for the economic data and (more importantly) for residents of areas which are at risk.

*****

northerntrust.com

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2017 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Copyright © Northern Trust