by Michael Doshier, Vice President, Retirement Marketing, Franklin Templeton Investments

Many investors who lived through the Global Financial Crisis of 2007-2009 still might bear some scars, according to Franklin Templeton’s annual Retirement Income Strategies and Expectations (RISE) survey. The survey explores individuals’ attitudes and expectations about retirement and how prepared people feel regarding their future. One of the main takeaways in this year’s survey is how many Millennial investors in particular remain focused on short-term market volatility, even though the markets have been able to bounce back. Michael Doshier, vice president, retirement marketing, offers highlights from the survey and examines how reactions to severe market shocks may impede us from reaching our long-term investment goals.

The Global Financial Crisis ended nearly eight years ago and yet the scars still run deep for many investors, at least according to findings in Franklin Templeton’s Retirement Income Strategies and Expectations (RISE) survey.1 Now in its sixth year in the United States, the survey aims to gauge individuals’ attitudes toward retirement and preparedness for the future. The survey spans multiple generations and includes current retirees who offer their wisdom about saving for retirement and the realities they now are facing.

This year’s survey held a few surprises with regard to the way people approach retirement and how different generations think about investing for it.

What we found particularly interesting about this year’s RISE survey is how strong fears of short-term market fluctuations seem to be in the minds of many investors, especially many younger ones.

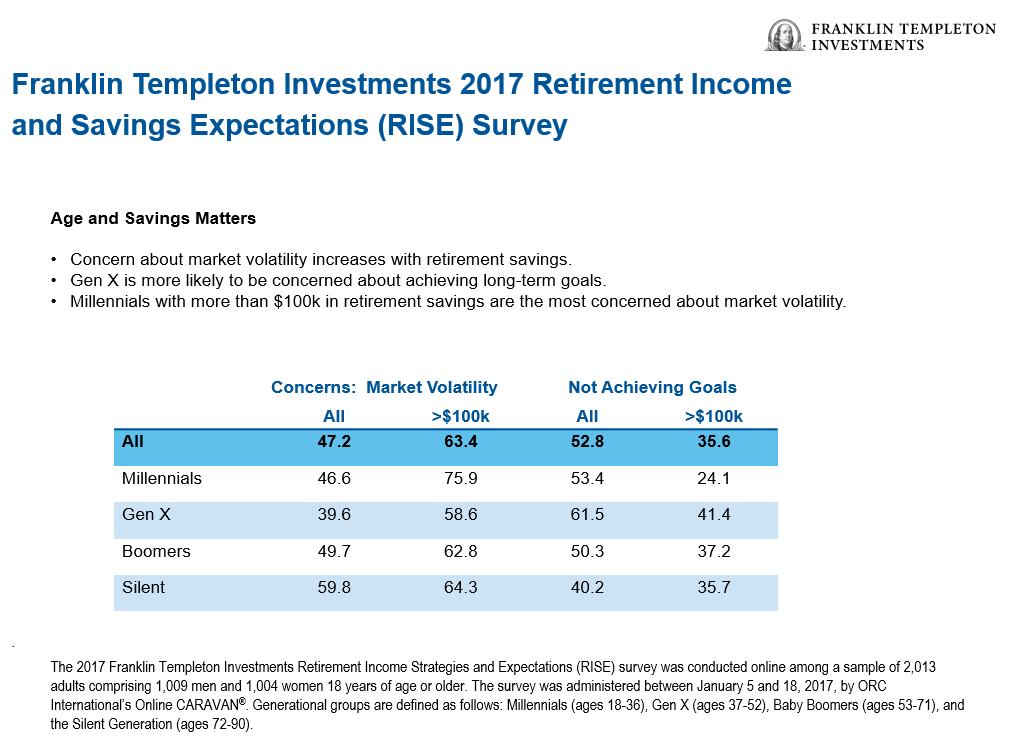

According to the RISE survey, all respondents were almost equally as concerned about short-term market volatility (47%) as they are about not achieving their long-term retirement investment goals (53%).

Across generations, Millennials were more preoccupied with short-term risks (47%) than GenXers (39%). Additionally, Millennials with more than $100,000 in retirement savings were even more anxious about short-term volatility (76%) than the other generational groups: GenXers, Boomers and the Silent Generation. Since younger investors intuitively would have a longer time horizon to invest and meet retirement goals, it struck us as a surprise that given their survey answers, Millennials appeared to be more risk averse.

Behavioral finance offers a possible explanation of what may be going on here. “Loss Aversion” can be a strong force when it comes to making investment decisions.

Of course, no investor wants the value of their investments to decline, but markets don’t always go straight up. Many investors react on emotion to short-term market volatility, cashing out of their investments instead of sticking out the dips. While such actions may seem like a rational response, sometimes the perception of “safety” can come at a cost. Cash—particularly at today’s low interest rates—doesn’t typically keep pace with inflation, so that money in the bank may actually be losing value over time. And when the markets recover, you’ve likely lost the ability to capture those longer-term gains.

This fun video outlines the concept further.

While our survey showed Millennials have a relatively high degree of confidence in meeting their retirement goals, this generation has the lowest percentage who have saved for retirement. Of course, the fact that they are younger than others surveyed certainly plays a part, but again behavioral finance offers a possible explanation as well.

There is also something called “present bias” wherein many people tend to focus only on the present, and not see the bigger picture. That $5 latte in the morning may be a pleasurable treat, but is it costing you a more secure retirement? What if you pooled that $5 per day into an investment vehicle instead? You may not get as much immediate gratification from saving for a long-term goal, but in my opinion, the delayed gratification of a secure future seems much more satisfying.

The short-term focus of many younger investors no doubt results from their experiences living through some dramatic market and economic cycles as they were coming of age. They may have had difficulty finding full-time employment when they graduated from college. They may have seen their parents suffer investment losses or sinking home values.

There could be more loss aversion within the Millennial generation because of how they experienced the market as adults. Combined with present bias, it may have created this situation of risk-aversion that we have seen show up in their RISE survey answers.

It often takes some outside help to overcome these emotional biases that may prevent us from reaching our investment goals, and this is one reason why working with a financial advisor can be beneficial.

The Good News

Though some fears persist, our 2017 RISE survey reflects general improvements in respondents’ confidence toward retirement from our 2016 survey. Again, perhaps surprisingly, Millennials were more likely to believe their retirement will be better than that of previous generations. So, if younger investors are concerned about short-term volatility and may not be investing enough as a result, where does this confidence come from?

We can only guess. But, we do know from the RISE survey that confidence in one’s ability to successfully invest for retirement increases among those working with a financial advisor compared with those who have never worked with one (87% and 53%, respectively). Similarly, 95% of those working with a financial advisor considered this partnership important to retirement planning and successfully generating income while in retirement.

This year’s RISE survey findings reflect the internal struggle that confronts most Americans who are trying to balance risk tolerance with short- and long-term retirement investment goals for themselves and their families.

The good news is that if an investor stays the course, continues to save and invest with a long-term focus and works with an advisor, his or her stress level may lessen—at least according to our RISE survey responses. The annual RISE survey has consistently revealed people working with a financial advisor have less stress and anxiety about retirement—and this year was no exception.

When you work with an advisor, you’ll feel better because advisors generally lead to better behaviors—and hopefully less stress for you when it comes to your financial future.

You can learn more about the various aspects of behavioral finance and how certain human emotions and responses may be holding you back from reaching your goals in our brochure, “Six Barriers of Investment Success.”

This communication is general in nature and provided for educational and informational purposes only. It should not be considered or relied upon as legal, tax or investment advice or an investment recommendation, or as a substitute for legal or tax counsel. Any investment products or services named herein are for illustrative purposes only, and should not be considered an offer to buy or sell, or an investment recommendation for, any specific security, strategy or investment product or service. Always consult a qualified financial professional or your own independent financial advisor for personalized advice or investment recommendations tailored to your specific goals, individual situation and risk tolerance.

Franklin Templeton Investments (FTI) does not provide legal or tax advice. Federal and state laws and regulations are complex and subject to change, which can materially impact results. FTI cannot guarantee that such information is accurate, complete or timely; and disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information.

Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

To get insights from Franklin Templeton Investments delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_US and on LinkedIn.

What Are the Risks?

All financial decisions and investments involve risk, including possible loss of principal.

_________________________________________________________________

1.The 2017 Franklin Templeton Investments Retirement Income Strategies and Expectations (RISE) survey was conducted online among a sample of 2,013 adults comprising 1,009 men and 1,004 women 18 years of age or older. The survey was administered between January 5 and 18, 2017, by ORC International’s Online CARAVAN®. Generational groups are defined as follows: Millennials (ages 18-36), Gen X (ages 37-52), Baby Boomers (ages 53-71), and the Silent Generation (ages 72-90).