by Richard Turnill, Global Chief Investment Strategist, Blackrock

The Federal Reserve (Fed) proceeded down its normalization path last week, yet weak U.S. inflation data had a larger impact on rates as long-term yields fell. This disconnect doesn’t change our expectation that modestly rising U.S. rates are ahead.

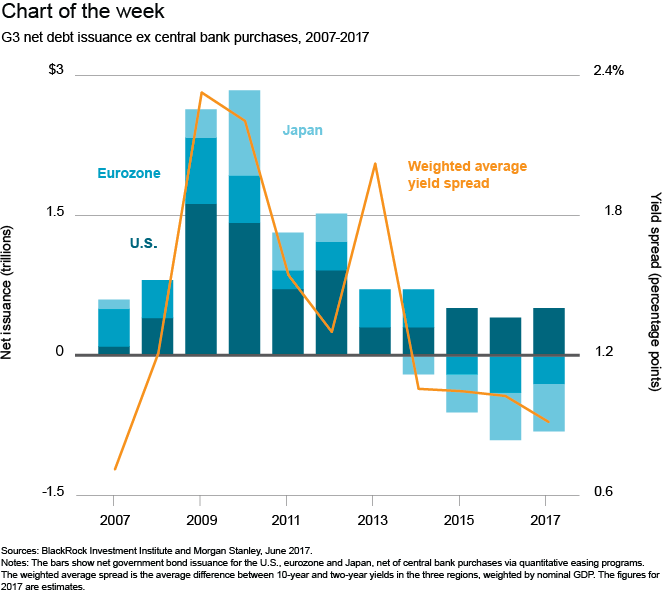

The Fed raised rates and indicated its balance sheet reduction would start this year. Quantitative easing globally decreased the amount of government bonds available for private investors, compressing the term premium—the extra yield that compensates investors for holding longer term debt. See the chart below.

The term premium collapse had a ripple effect across markets, pushing investors into riskier fixed income and inflating valuations in assets from real estate to dividend stocks—what former Fed Chair Ben Bernanke termed the “portfolio rebalance channel.” The consequences of this process reversing are uncertain—the Fed has never before used asset reductions as a tightening tool. Hence we see the central bank unwinding cautiously—akin to crossing a river by feeling the stones. The benign market reaction last week suggests that, for now, it has succeeded in avoiding another “taper tantrum.”

The recent disconnect between Fed normalization and falling long-term rates is partly a result, in our view, of markets overly focusing on softening inflation data, while the Fed focuses more on the outlook. It could persist in the near term. We see sustained above-trend global growth and stabilizing inflation ahead, meaning the impact of the Fed’s pace of normalization may be greater than bond markets currently anticipate.

Our base case is for modestly rising U.S. rates. Global demand for income, fueled by still highly accommodative monetary policy in Europe and Japan, should help limit yield spikes. Front-end to intermediate U.S. Treasuries, credit and mortgages offer little cushion against Fed normalization hiccups. We prefer duration exposure in the long end and higher quality credits for income. Read more market insights in my Weekly Commentary.

Richard Turnill is BlackRock’s global chief investment strategist. He is a regular contributor to The Blog.

*****

Investing involves risks, including possible loss of principal. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of June 2017 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

©2017 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries in the United States or elsewhere. All other marks are the property of their respective owners.

Copyright © Blackrock