by Lance Roberts, Clarity Financial

Lately, there has been a lot of chatter about the “Return Of Animal Spirits” as the catalyst to drive markets higher…and higher…and higher. But exactly what does that mean?

Animal spirits came from the Latin term “spiritus animalis” which means the breath that awakens the human mind. Its use can be traced back as far as 300BC where the term was used in human anatomy and physiology in medicine. It referred to the fluid or spirit that was responsible for sensory activities and nerves in the brain. Besides the technical meaning in medicine, animal spirits was also used in literary culture and referred to states of physical courage, gaiety, and exuberance.

It’s more modern usage came about in John Maynard Keynes’ 1936 publication, “The General Theory of Employment, Interest, and Money,” wherein he used the term to describe the human emotions driving consumer confidence. Ultimately, the “breath that awakens the human mind,” was adopted by the financial markets to describe the psychological factors which drive investors to take action in the financial markets.

The 2008 financial crisis revived the interest in the role that “animal spirits” could play in both the economy and the financial markets. The Federal Reserve, then under the direction of Ben Bernanke, believed it to be necessary to inject liquidity into the financial system to lift asset prices in order to “revive” the confidence of consumers. The result of which would evolve into a self-sustaining environment of economic growth.

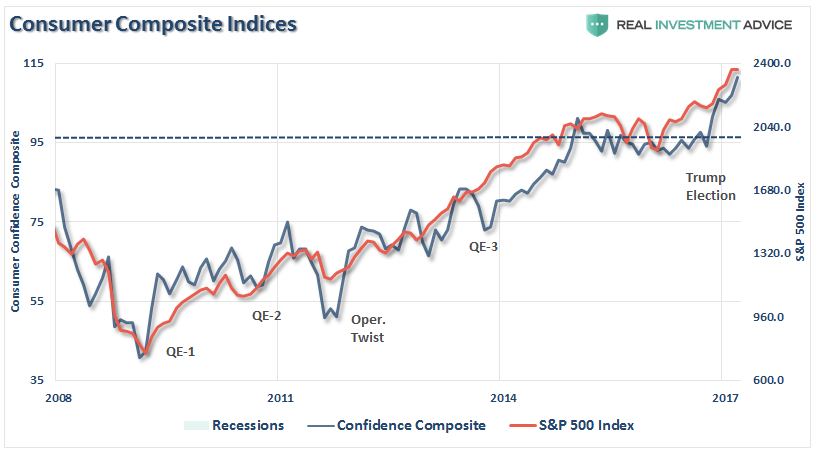

Ben Bernanke & Co. were successful in fostering a massive lift to equity prices since 2009 which, in turn, did correspond to a lift in the confidence of consumers. (The chart below is a composite index of both the University of Michigan and Conference Board surveys.)

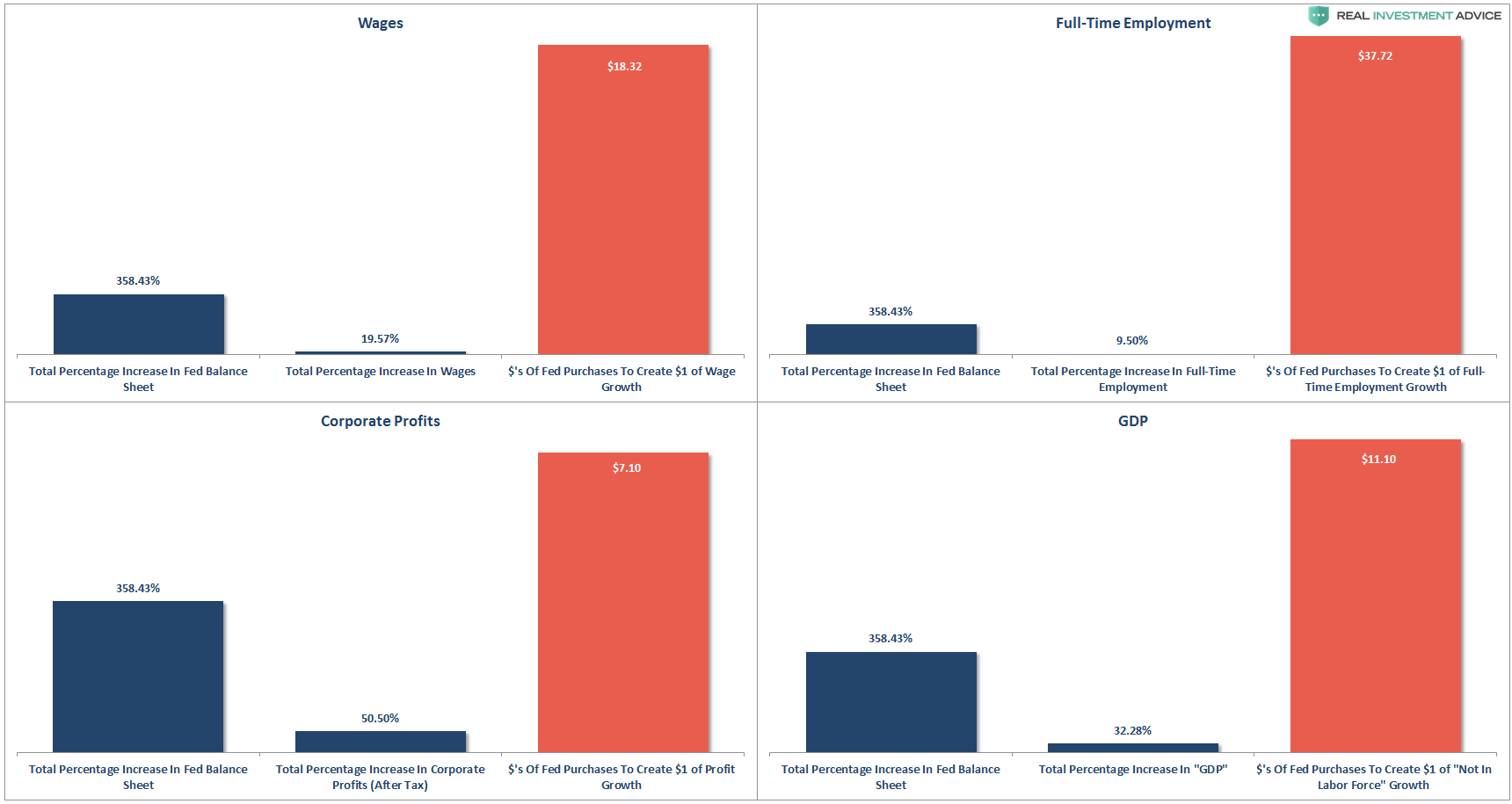

Unfortunately, despite the massive expansion of the Fed’s balance sheet and the surge in asset prices, there was relatively little translation into wages, full-time employment, or corporate profits after tax which ultimately triggered very little economic growth.

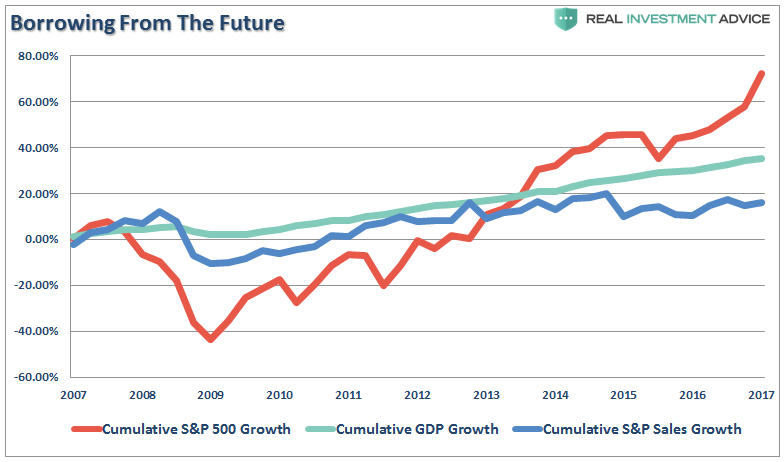

The problem, of course, is the surge in asset prices remained confined to those with “investible wealth” but failed to deliver a boost to the roughly 90% of American’s who have experienced little benefit. In turn, this has pushed asset prices, which should be a reflection of underlying economic growth, well in advance of the underlying fundamental realities. Since 2009, the S&P has risen by roughly 220%, while economic and earnings per share growth (which has been largely fabricated through share repurchases, wage and employment suppression and accounting gimmicks) have lagged.

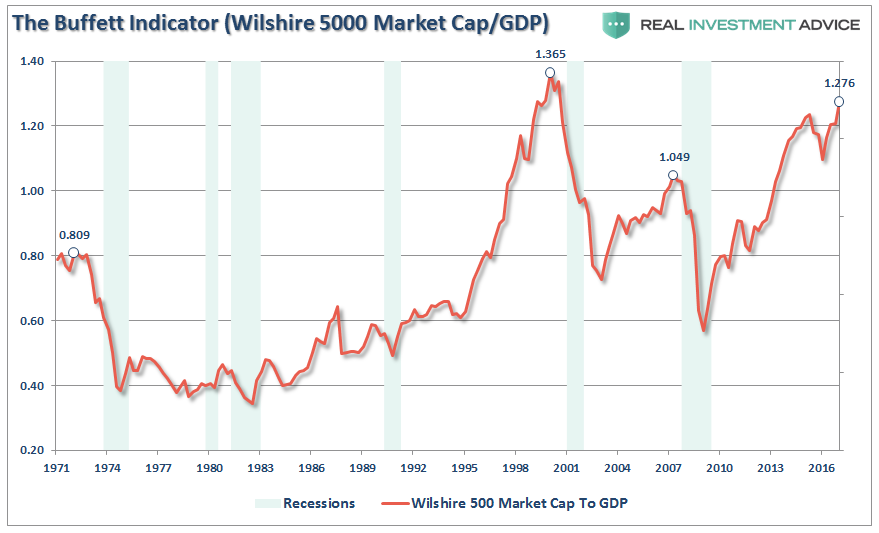

The stock market has returned almost 80% since the 2007 peak which is more than twice the growth in GDP and nearly 4-times the growth in corporate revenue. (I have used SALES growth in the chart below as it is what happens at the top line of income statements and is not as subject to manipulation.) The all-time highs in the stock market have been driven by the $4 trillion increase in the Fed’s balance sheet, hundreds of billions in stock buybacks, PE expansion, and ZIRP. With Price-To-Sales ratios and median stock valuations not the highest in history, one should question the ability to continue borrowing from the future?

A Late Stage Event

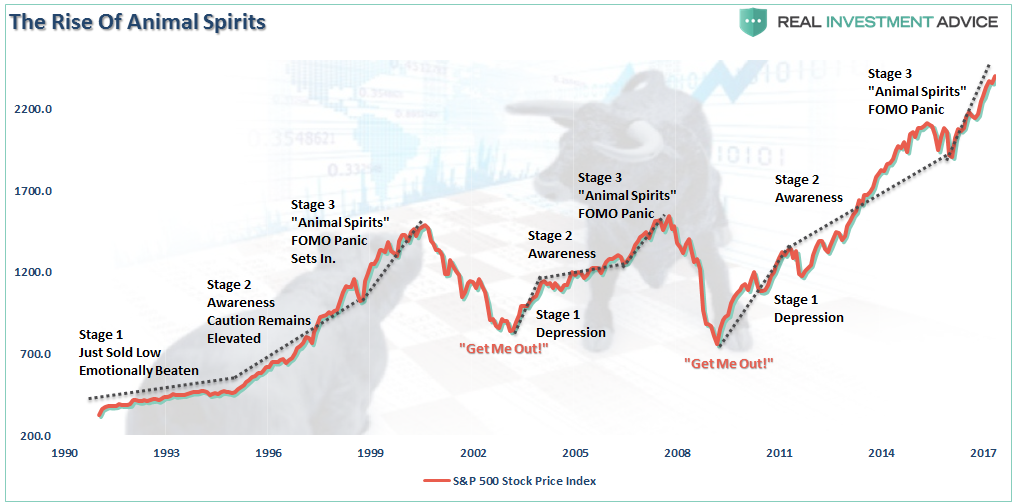

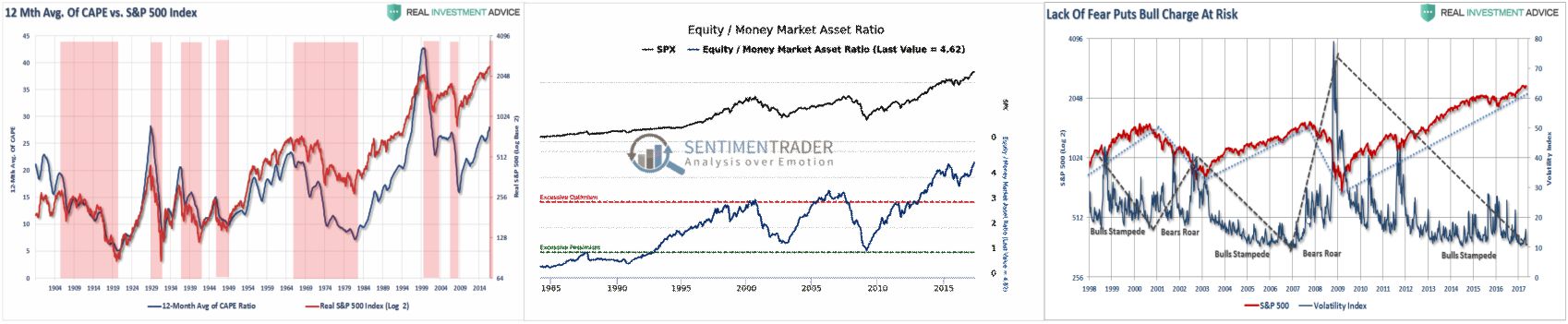

Here’s a little secret, “Animal Spirits” is simply another name for “Irrational Exuberance,” as it is the manifestation of the capitulation of individuals who are suffering from an extreme case of the “FOMO’s” (Fear Of Missing Out). The chart below shows the stages of the previous bull markets and the inflection points of the appearance of “Animal Spirits.”

Not surprisingly, the appearance of “animal spirits” has always coincided with the latter stages of a bull market advance and has been coupled with over valuation, high levels of complacency, and high levels of equity ownership.

Just last week Ed Yardeni penned a piece on this issue of “Animal Spirits.” To wit:

“So far, the current bull market has marched impressively forward despite 56 anxiety attacks, by my count. They were false alarms. I remain bullish. My long-held concern is that the bull market might end with a melt-up that sets the stage for a meltdown. The latest valuation and flow-of-funds data certainly suggest that the melt-up scenario may be imminent, or underway.”

A more anecdotal sign came from Joe Ciolli via Business Insider:

“Buy low, sell high. It’s a classic adage — one that has helped stock investors reap consistent gains for the better part of seven decades.

Until now.

Having returned 5% on average each year from 1940 through 2007, the so-called value trade has lost 2% per year over the past decade, according to Goldman Sachs data. It’s down 10% this year alone, badly lagging an S&P 500 that has climbed 8.7%.”

Since “the price you pay day is the value you receive tomorrow,” as famously noted by Warren Buffet, it should not come as a surprise that “value investing” is lagging the “momentum chase” in the market currently. But again, this is something that has historically, and repeatedly occurred, during very late stage bull market advances as the “rationalization” for a “never-ending bull market” are promulgated.

Given the length of the economic expansion, the risk to the “bull market” thesis is an economic slowdown, or contraction, that derails the lofty expectations of continued earnings growth. More importantly, it is the realization of the inability to pass the legislative agenda the markets have been banking on to support further earnings expansion that could be the problem.

The bottom line is the hunt by investors for growth over value has always set the stage for exceptionally poor returns over the subsequent decade.

Of course, the rise in “animal spirits” is simply the reflection of the rising delusion of investors who frantically cling to data points which somehow support the notion “this time is different.” As David Einhorn once stated:

“The bulls explain that traditional valuation metrics no longer apply to certain stocks. The longs are confident that everyone else who holds these stocks understands the dynamic and won’t sell either. With holders reluctant to sell, the stocks can only go up – seemingly to infinity and beyond. We have seen this before.

There was no catalyst that we know of that burst the dot-com bubble in March 2000, and we don’t have a particular catalyst in mind here. That said, the top will be the top, and it’s hard to predict when it will happen.”

Is this time different? Most likely not. This was a point James Montier noted recently,

“Current arguments as to why this time is different are cloaked in the economics of secular stagnation and standard finance workhorses like the equity risk premium model. Whilst these may lend a veneer of respectability to those dangerous words, taking arguments at face value without considering the evidence seems to me, at least, to be a common link with previous bubbles.“

While individuals are quick to dismiss the rising risks in the markets, it would be wise to remember the same beliefs were held in 1999 and 2007. Throughout history, financial bubbles have only been recognized in hindsight when their existence becomes “apparently obvious” to everyone. Of course, by that point is was far too late to be of any use to investors and the subsequent destruction of invested capital.

This time will not be different. Only the catalyst, magnitude, and duration will be.

Investors would do well to remember the words of the then-chairman of the Securities and Exchange Commission Arthur Levitt in a 1998 speech entitled “The Numbers Game:”

“While the temptations are great, and the pressures strong, illusions in numbers are only that—ephemeral, and ultimately self-destructive.”

For now, the revival of “animal spirits” can certainly continue to drive markets higher in the short-term. The only question is will you know the difference between the next “buy the dip” opportunity and the “last call for alcohol?”

Just be careful or those “animal spirits” may just wind up biting you.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In

Copyright © Clarity Financial