Keeping Your Balance as Rates Rise

As we noted in a previous blog, we’ve found that investors can minimize risk and earn relatively high income by pairing rate-sensitive assets such as government bonds with growth-oriented credit assets in a single portfolio and letting their managers adjust the balance as conditions change.

A key benefit of this approach, known as a credit barbell strategy, is that it helps investors avoid leaning too far in either direction—and overexposing themselves to a single risk.

For example, when investors see bond yields rise as sharply as US Treasury yields did between November and March, they often do the following two things:

First, they reduce duration—or interest-rate risk—in their core bond portfolios, which focus on investment-grade debt and include a healthy share of government bonds. Higher rates reduce the market value of these securities.

Second, they take more credit risk in their high-income allocation, as high-yield bonds, emerging-market debt and other credit assets tend to outperform when growth and interest rates rise.

Rising Rates Don’t Have to Derail Returns

US bond yields’ upward momentum has stalled recently. But let’s face it: if the economy keeps improving, the Federal Reserve will keep raising rates and yields will probably resume their climb. If the European Central Bank ends quantitative easing later this year, European yields may rise, too.

In other words, expect plenty of investors to stick to the script.

Here’s the problem: cutting back too drastically on interest-rate-sensitive assets such as Treasuries or mortgage-backed securities can make a fixed-income allocation less diverse—and less stable.

It can also cost investors income. Sure, government bonds, mortgage-backed securities and even many investment-grade corporate bonds are highly sensitive to rising interest rates. But as these bonds mature, their prices drift back toward par. That means investors can reinvest the coupon income in newer—and higher-yielding—bonds.

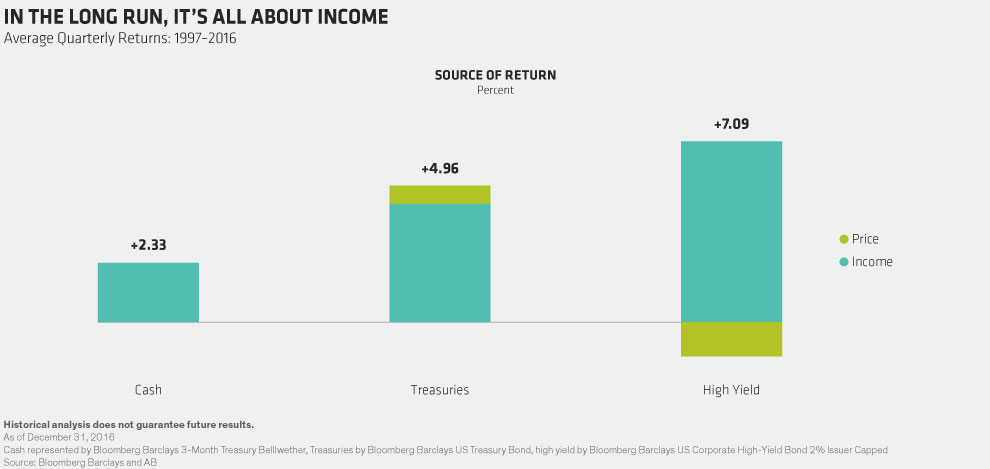

As the Display below shows, income accounted for nearly all the average quarterly return of US Treasuries over the last 20 years—a period when yields fell sharply and prices rose. High-yield bonds, of course, relied even more heavily on income to drive returns—price movement was a negative.

This illustrates why rate-sensitive assets should always have a seat at the asset-allocation table. It also helps to explain why a skilled active manager who pairs them with return-seeking assets such as high yield and adjusts the balance as needed has the potential to produce relatively high returns.

Credit Risk: Don’t Overdo It

Meanwhile, investors who lean too heavily toward return-seeking assets might be taking on more credit risk than they want at a time when many corporate bond valuations look stretched and some credit cycles—particularly in the US—are in the twilight stage.

Also, high-yield bonds and other return-seeking credit assets are more closely correlated to equities than they are to the rest of the fixed-income universe. That means a strong tilt toward credit can lead to a less diversified investment portfolio.

None of this means investors shouldn’t adjust their interest-rate exposure in a rising-rate environment. Shortening duration might be appropriate. But it’s important not to overreact.

We’ve already seen that Treasuries provide diversification and income to a bond allocation. But here’s another thing to remember: rising rates eventually lead to slower growth. When that happens, credit cycles fizzle out, growth-sensitive assets struggle and interest rates eventually fall.

A credit barbell strategy allows managers to see this interplay between global interest-rate and credit cycles more clearly and to tilt slightly toward one or the other without putting investors’ portfolios out of balance.

That’s a lot harder to do when you assign your rate-sensitive and growth-sensitive assets to separate portfolios run by separate managers.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein