Thoughts on the growth prospects for the world’s second-largest economy, its red-hot housing market and weakening currency.

by Stephen Green, Economist, Capital Group

Key Takeaways

- China's economy can sustain its momentum through June, supported by government stimulus, infrastructure projects and housing development

- Demand for commodities and construction equipment should be supported by credit growth

- The Chinese renminbi will likely further depreciate against the U.S. dollar amid external pressures

The list of problems that China faces is not short. Its economy isn't growing as fast as it once was, monetary authorities are battling capital flight, debt is mounting and the new U.S. president is talking tough on trade. Here is how I see things shaping up for China in 2017.

Stimulus Effects Still Feeding Through the Economy

I am more optimistic than most about the direction of the Chinese economy. The consensus view is that China's economy will lose momentum in the first quarter of this year as the red-hot housing market cools and government stimulus wears off. There is also the risk of tense trade relations with the U.S.

That said, in my view China's economy can continue to grow along its current trajectory in the first half of the year, which is 6.5% according to official government figures.

Here's why: There are enough new investment projects in the pipeline to support economic growth during the first half of 2017. Construction firms, for instance, reported order growth of greater than 30% during the first nine months of 2016. This included a mix of big and small projects, ranging from real estate to infrastructure and manufacturing. The good news is projects tend to last two to four years. And by my count, this activity marks the greatest acceleration in new project starts since 2009. This should be supportive for commodity prices and global mining companies through the first half of 2017.

There is a lot of skepticism out there right now about private sector capital expenditures, too — but there are early signs capex is recovering, with real interest rates down and some sectors showing obvious capacity shortages.

To be sure, I do expect growth to slow in the second half of this year, especially with mortgage credit slowing and home sales having flattened.

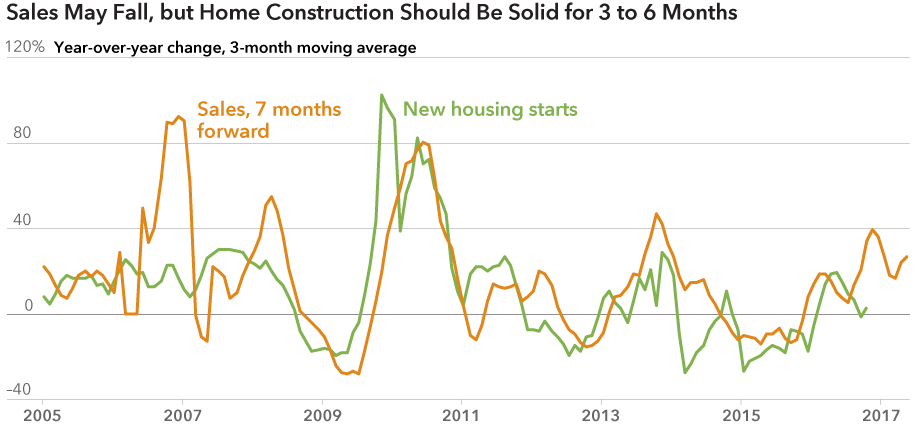

Pockets of Strength in the Housing Market

There is a lot of bearishness about China's housing sector.

Home sales skyrocketed in 2016, as did prices, with approximately $1.4 trillion in new housing sold. Worried about a property bubble, government authorities are curbing incentives and rolling out buying restrictions as well as stricter lending requirements in some larger markets.

This is certainly impacting activity in China's 30 largest cities, where sales fell 20% year on year in November. The market's expectation now is that new housing starts will fall, denting gross domestic product growth and demand for commodities such as iron ore, copper and cement.

I agree that sales will slow, but not to the degree that most suspect.

Outside of the 30 largest cities, sales remain stronger due to affordability and the absence of government purchase restrictions. Immigration into smaller cities from surrounding rural areas will continue, pushing up the urbanization ratio from its current 55% level to nearer 70% to 80% over the next two decades. A lot of urban households want to upgrade their apartments, too. Interest rates also remain low, which should continue to support sales across most markets. Furthermore, we have moved past the horror stories of ghost cities. Inventories continue to shrink nationally and housing stock in the bigger cities is at pre-glut levels. Inventories remain high in many smaller cities, though, so this is still a challenge.

Along those lines, new housing starts should continue to grow for the next three to six months, I think. Historically, housing accounts for twice the commodities demand of infrastructure, so I am watching this closely. While cautious, developers appear to be building more again.

Source: Capital Group

Currency Pressures, but No Big Devaluation

The Chinese renminbi is under pressure from capital outflows, the prospect of faster U.S. interest rate increases in 2017, and worries that President Donald Trump will follow through on his pledge to slap tax penalties on imports. Despite these headwinds, I think there is a limited chance the People's Bank of China will stray from its stated policy of steady depreciation and will pull the trigger on a big one-time devaluation. There are just too many risks for Beijing in that course of action — and this year, especially, no one has incentives for taking that risk.

If the U.S. dollar stays strong, I do anticipate more aggressive measures by the PBOC to combat capital flight, making it more difficult for individuals and companies to move money outside China. The central bank will also keep tapping foreign currency reserves to prop up the renminbi, which fell more than 6% against the U.S. dollar in 2016. Reserves currently stand at $3 trillion. While some $2 trillion is liquid and available for use, in my view Beijing would get very nervous if reserves shrank by a billion during the course of the year. I expect the renminbi to weaken some 6% against the U.S. dollar this year, but there are risks. Until dollar strength abates, it's going to be a bumpy ride for the renminbi.

Source: MSCI, RIMES. As of 12/31/2016.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not distribute the MSCI data or use it as a basis for other indices or investment products.

Get Ready for China's Biggest Turnover in Political Leadership in a Generation

In the fall, China's 19th National Party Congress will convene, during which five of the seven members of the Politburo Standing Committee — the inner sanctum of power — are due to retire. Maybe it turns out to be only four retirees — we'll have to see. Close to half of the Politburo (25 members who influence policymaking) will also be reshuffled due to retirements and promotions, while the Central Committee will see large numbers of its 205 fulltime members step aside. That makes it a huge year politically. What unfolds will shape the country's economic priorities for the next five years.

For President Xi Jinping, this is a prime opportunity to strengthen his political clout. For one, I do not expect Xi to name a successor, thus setting himself up for a third term that would run through 2027.

There is also a possibility a new premier will be named. That person could be Wang Qishan, a current member of the Politburo Standing Committee who spearheaded the unprecedented anti-corruption campaign. If he fills that role, he would be responsible for economic policies.

This would have several implications: Wang is believed to be market-friendly, and would have the bureaucratic power to push some tough reforms through. This may include a major recapitalization of the big state-owned banks to flush out the bad loans, and privatizing some of the debt-heavy state-owned enterprises. That said, any such program would have to be approved by Xi — and his real intentions are very hard to read, though there is much evidence to suggest he believes that strong party control of the economy is vital to China's continued rise.

About Stephen Green

Stephen Green is an economist at Capital Group, responsible for covering Asia. He has 12 years of investment industry experience and has been with Capital Group for two years. Prior to joining Capital, he was head of research for Greater China at Standard Chartered Bank, in Beijing, Shanghai and Hong Kong. Before that he ran UK think tank, the Asia Programme at Chatham House. He holds a PhD in government from the London School of Economics and a first-class honours degree in social and political sciences from Cambridge University. Stephen is based in Hong Kong.

Stephen Green is an economist at Capital Group, responsible for covering Asia. He has 12 years of investment industry experience and has been with Capital Group for two years. Prior to joining Capital, he was head of research for Greater China at Standard Chartered Bank, in Beijing, Shanghai and Hong Kong. Before that he ran UK think tank, the Asia Programme at Chatham House. He holds a PhD in government from the London School of Economics and a first-class honours degree in social and political sciences from Cambridge University. Stephen is based in Hong Kong.

Copyright © Capital Group