by Pater Tenebrarum via Acting-Man blog,

Positioning Indicators at new Extremes

We are updating our suite of sentiment data again, mainly because it is so fascinating that a historically rarely seen bullish consensus has emerged – after a rally that has taken the SPX up by slightly over 210% from its low. Admittedly, a slew of such records has occurred in the course of the past year or so, and so far has not managed to derail the market in the slightest– in fact, since 2012, only a single correction has occurred that even deserves the designation “correction” (as opposed to “barely noticeable dip”).

While a number of positioning and survey data show a bullish consensus that easily dwarfs anything that has been seen before, this consensus is not reflected in expressions of exuberance by the broader public. “Anecdotal” sentiment seems more cautious and skeptical than the quantitatively measurable kind. Most likely this is because the vast bulk of the middle class has been so thoroughly fleeced in the last two boom-bust sequences that it finds itself in dire straits in spite of the reemergence of major asset bubbles across a wide swathe of assets. This includes by the way an astonishing revival of the bubble in real estate prices – see e.g. this 330 square foot shack in San Francisco, which recently sold for $765,000:

Yes, that tiny dark-brown thingy situated on a steep road sold for $765,000. The real estate bubble is back.

(Photo credit: SFARMLS)

Moreover, with the broad US money supply (TMS-2) having nearly doubled since 2008 and other major central banks inflating their money supply as well at breakneck speed, there has been more than enough “tinder” provided the world over to drive asset prices higher. This by the way makes a complete mockery of the constant refrain of central bankers that we are allegedly threatened by “deflation”. The inflationary effects of their monetary pumping are simply showing up in asset prices rather than consumer goods prices – ceteris paribus, a rapid inflation of the money supply always leads to prices rising somewhere in the economy.

Bubble Trouble

There is of course a “danger” that this asset price bubble will burst rather spectacularly once monetary inflation slows down sufficiently (it will probably never be reversed again in our lifetime, but a slowdown is already underway). In light of the current rare extremes in positioning, sentiment and leverage, the eventual denouement of the current bubble should be a real doozy. Note that in every respect one can possibly think of – with the sole exception of household debt – systemic leverage is at new all time highs (not only in absolute terms, but relative to everything, including the size of the known universe), and is likewise positively dwarfing anything that has occurred before.

Specifically relevant for financial markets are record highs in margin debt, record highs in hedge fund leverage, as well as record issuance of junk debt in recent years, which in turn has given rise to systemic leverage once again vastly increasing in the credit markets on the part of investors as well. To the latter point, note that financial engineering that is specifically aimed at enabling the taking of extremely leveraged positions is back with a vengeance as well – however, at the same time, the markets for the underlying debt instruments have become quite illiquid due to new banking regulations that hinder proprietary trading activities by banks (for a more detailed discussion of these topics see “A Dangerous Boom in Unsound Corporate Debt” and “Comforting Myths About High Yield Debt”).

In light of all these considerations, it is truly remarkable how little concern there is. Even former skeptic Hugh Hendry is these days talking about the alleged “omnipotence of central banks” which money managers are forced to surrender to (this view strikes us actually as an example of the “potent directors fallacy” – see also this comment by EWI on the topic). While we certainly have some understanding for his perspective – after all, as a fund manager, he cannot afford to “miss” an asset boom, or he will soon be out of a job – we do think he may be underestimating the potential for a capsizing of the happy ship that could well happen in an unseemly hurry, for currently unanticipated reasons. With “reasons” we actually mean “triggers” – the reasons are already discernible and perfectly clear: we listed most of them above. All that is still needed is a trigger that alters the perceptions of a critical mass of observer-participants.

In short, bubbles don’t burst because of a “black swan”: rather the swan – often a combination of events that makes it impossible to identify a single trigger – is a diffuse trigger mechanism that sets into motion what is already preordained. It is the famous “one grain too many” that is put atop a giant sand pile – however, it is the sand pile that is the problem, not the one grain. This is also why precise timing of a bubble’s demise is so difficult – it is unknowable what exactly will actually lead to the change in perceptions that ultimately provokes the unwinding of the leverage that has been built up.

At some point down the road, a Zimbabwe or Venezuela type very rapid devaluation of money may emerge. In this case asset prices would become solely a function of monetary debasement. It is important though to keep in mind that things don’t just move from the present state to the Venezuela type state from one day to the next – not to mention that it may not happen at all, if central banks in developed nations alter their policies in time. Assuming for argument’s sake though that it does eventually happen, there will still be an interim phase during which monetary debasement will e.g. alter the perceptions of stock market investors regarding the multiples they should pay for corporate earnings. This is what happened e.g. in the 1970s: multiples contracted into single digit territory, because market participants decided that the future stream of earnings would be less valuable in real terms, and thus deserved a commensurate discount.

Sentiment Data

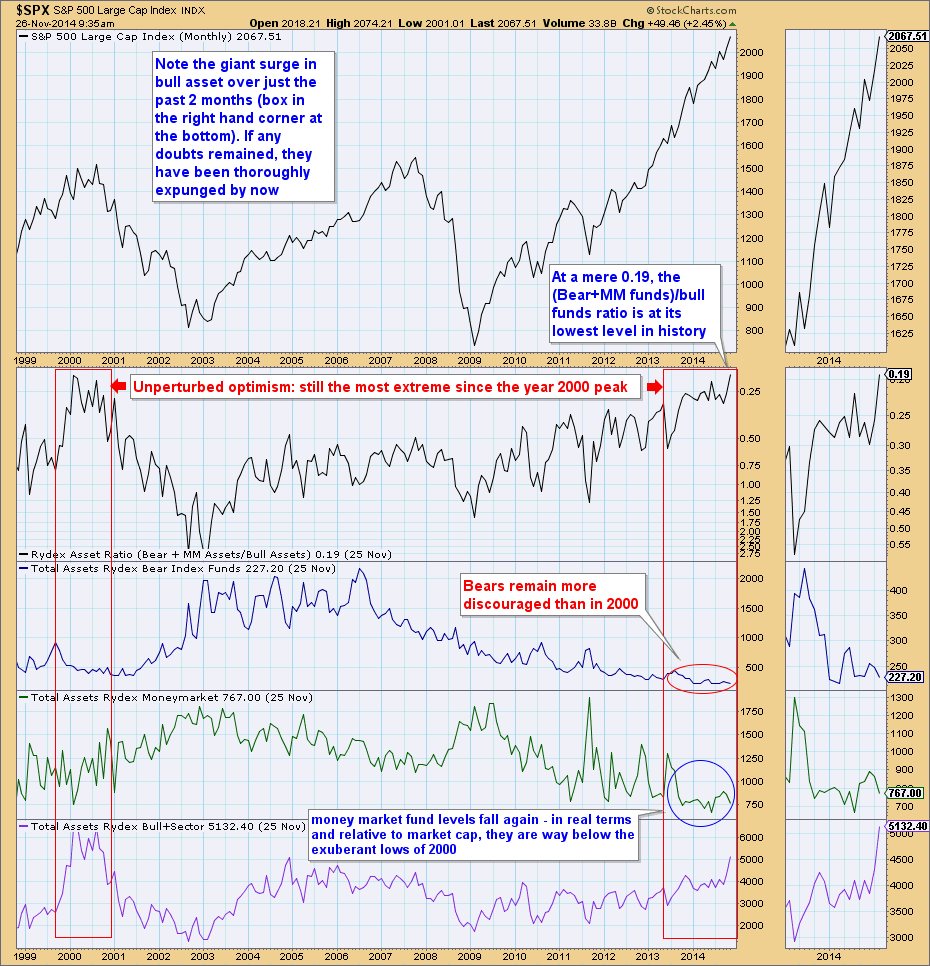

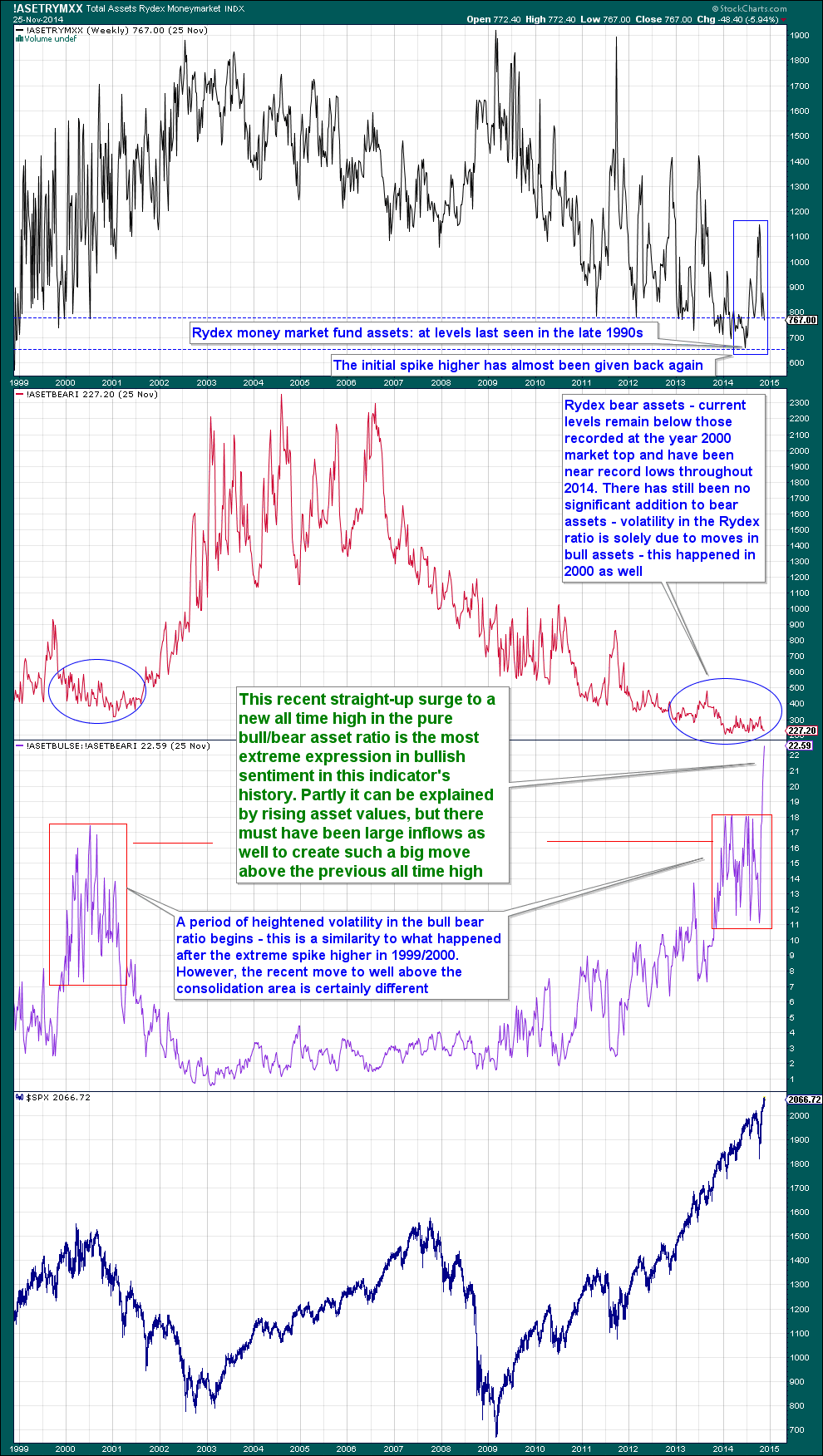

Let us move on now to our suite of data. We have on purpose decided to follow a number of data points that relatively few people usually look at, in the hope that they may therefore be slightly more meaningful. Below we show three different views of Rydex data. The first chart shows the Rydex ratio in the form (bear+money market fund assets)/bull assets, as well as the disaggregated bear, MM fund and bull assets. It is noteworthy that the ratio of bears plus fence sitters to bulls has now also declined to a new all time low (the chart is inverted).

The second chart shows a more detailed view of money market and bear assets, plus the “pure” bull/bear asset ratio. The latter has made a remarkable move in recent weeks – it has gone straight up without even the slightest correction, as assets deployed in bull funds have exploded higher. In terms of this data series it represents the most extreme expression of a bullish consensus ever.

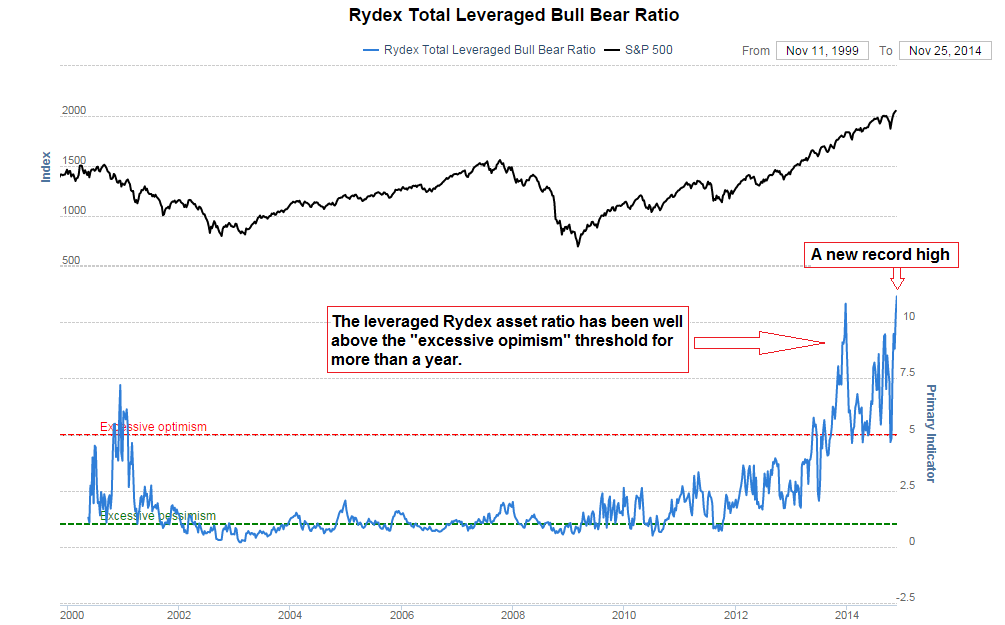

Next comes the leveraged bull/bear fund ratio, which compares assets in Rydex funds that employ leverage. Almost needless to say, it is at an all time high as well, but what is most remarkable about it is that it has spent more than a year in “excessive optimism” territory. This by the way goes to show that these data are not very useful for timing purposes. What they are useful for is this: the more time they spend in extreme territory, the more profound the move in the opposite direction is likely to be once it gets going.

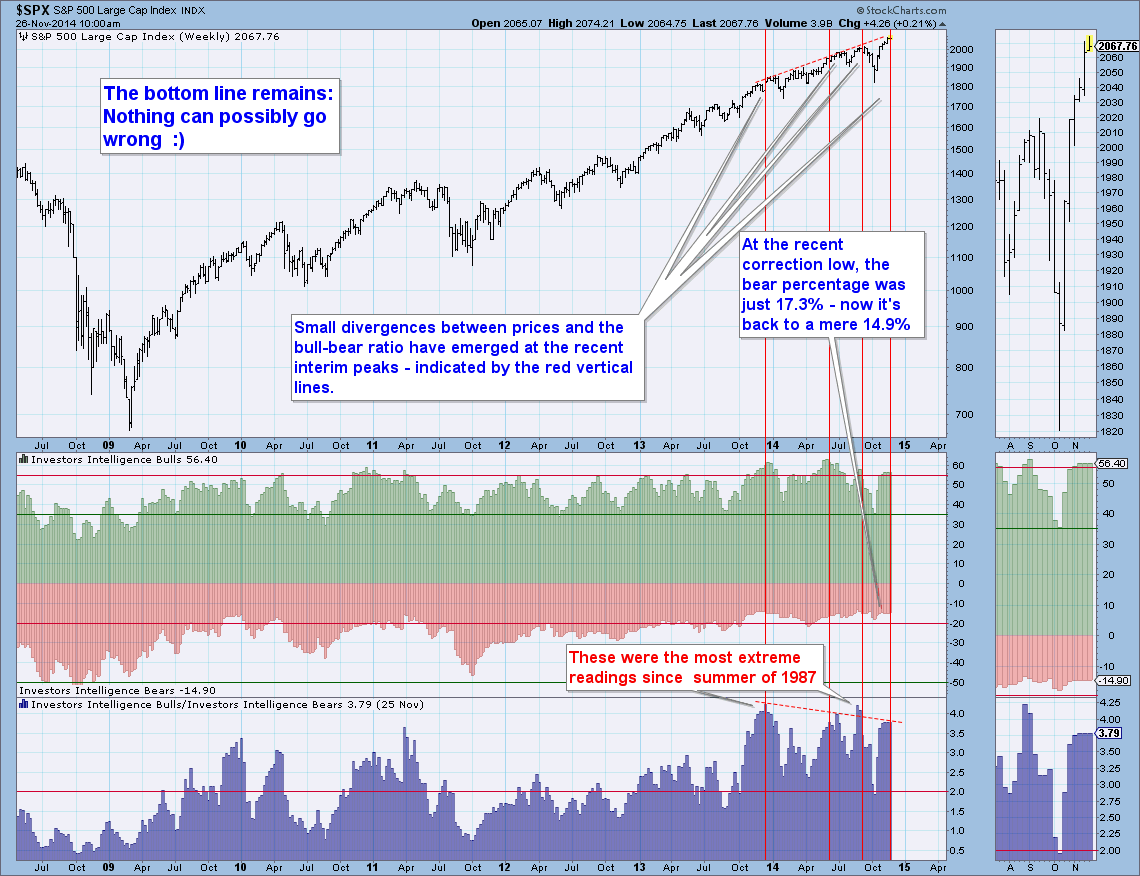

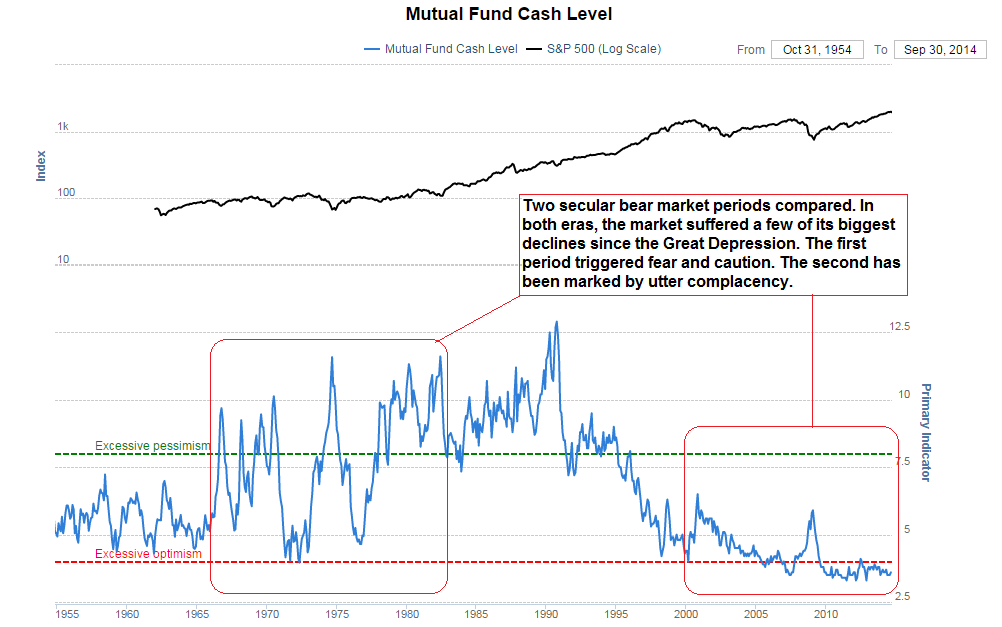

Similar considerations apply to the Investor’s Intelligence survey and the mutual fund cash-to-assets ratio which come next. We show a very long term chart of the latter – what is noteworthy is the big difference in fund manager positioning and sentiment during the period beginning in 2000 compared to the secular bear market that lasted from 1968 to 1982. The latter was characterized by extreme fear and caution, while the period since the 2000 tech mania peak shows a remarkable degree of complacency (again, we think this is quite meaningful for the long term outlook).

Lastly we also update the still growing divergences between junk debt ETFs and credit spreads versus the SPX.

Rydex: the (bear + MM funds)/bull funds asset ratio has now also hit a new all time low. This was mainly due to a huge surge in bull assets (which have increased roughly by one third in the 6 weeks since the October correction low) – click to enlarge.

A closer look at money market funds, bear assets and the “pure” bull/bear asset ratio. The latter has just made a truly stunning move. Nothing comparable has ever happened before – click to enlarge.

The leveraged Rydex bull/bear asset ratio – in “extreme optimism” territory for more than a year, and currently at a new all time high – click to enlarge.

The Investor’s Intelligence survey. The bull/bear ratio has failed to return to the 27 year high hit earlier this year twice in succession, but the bear percentage has fallen back to 14.9% – only slightly above the all time low of 13.3% recorded earlier this year – click to enlarge.

The mutual fund cash-to-assets ratio. Compare the secular bear market of 1968-1982 with the period since the year 2000 tech bubble peak. Fear and caution have been replaced by utter complacency. This is likely telling us something about what to expect in the long term – click to enlarge.

Junk debt (represented by the JNK ETF) compared to government debt and the SPX. Credit spreads are widening and the divergence with the stock market keeps growing – click to enlarge.

Conclusion – Real Wealth Undermined:

As noted in the title to this post, in some respects we’re in danger of running out of appropriate descriptive superlatives for the current bout of “irrational exuberance” (we’re open for suggestions). The current asset bubble is in many respects reminiscent of the late 1990s tech bubble, but it also differs from it in a number of ways. One of the major differences is that the exuberance recorded in the data is largely confined to professional investors, while the broader public is still licking its wounds from the demise of the previous two asset bubbles and remains largely disengaged (although this has actually changed a bit this year).

A few additional remarks regarding the alleged “omnipotence” of central banks: monetary pumping certainly has the power to distort prices across the economy, which includes inflating the prices of titles to capital. However, at some point there will be a stark choice – either the pumping is abandoned voluntarily, or one risks the destruction of the underlying currency system.

Moreover, there is another limiting factor in play, which doesn’t get as much attention as it probably deserves. Monetary pumping merely redistributes existing real wealth (no additional wealth can be created by money printing) and falsifies economic calculation. This in turn distorts the economy’s production structure and leads to capital consumption, thus the foundation of real wealth that allows the policy to seemingly “work” is consistently undermined. At some point, the economy’s pool of real funding will be in grave trouble (in fact, there are a number of signs that this is already the case). Widespread recognition of such a development can lead to the demise of an asset bubble as well.

Copyright © Pater Tenebrarum via Acting-Man blog