Authored by Matthew Mish, UBS Strategist

The Great Rotation debate: much ado about nothing?

The concept of the Great Rotation continues to garner significant investor attention. From a flow perspective, our own analysis and those of our colleagues across various asset classes infers there is scant evidence of a large rotation out of corporate credit or fixed income in general. In our view, the outlook for investment flows must consider both the flow and stock perspectives. To that end, we look to the corporate and foreign bond holdings as reported by the Federal Reserve’s Flow of Funds data as a barometer for market holdings given the depth of disclosure and importance of US markets in global indices.

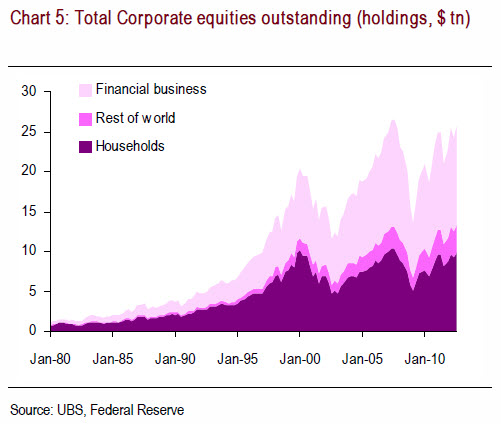

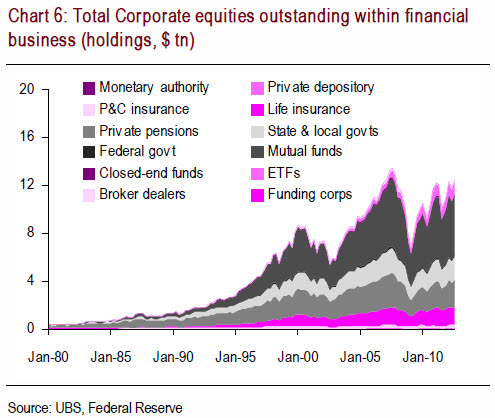

The Fed Flow of Funds data reports total amount of credit market debt outstanding is $55tn, of which the largest shares include $13tn in mortgages, $12tn in corporate and foreign bonds (foreign bonds are bonds issued in the U.S. by foreign borrowers through U.S. dealers and purchased by U.S. residents), $11tn in Treasuries and $7.5tn in agency and GSE-backed securities. The mortgage market was the last decade’s story. From 2000 to 2007, total mortgages outstanding rose from $6.7tn to 13.5tn. Since 2007, mortgages have fallen from $14.5tn to 13tn as declining holdings of ABS issuers and agency & GSE-backed mortgage pools have been largely offset by rising GSE holdings. The focus of the current debate within fixed income is more concentrated on corporate and government debt. Charts 1, 2 and Charts 3, 4 depict the growth in total debt outstanding for both sectors, respectively, broken down by, first, assets held by financials, rest of world and households and, second, sub-segments within financials.

From 2000 to 2007, total corporate debt increased from $4.8tn to $11.5tn, with outsized accumulations in rest of world and household holdings (Chart 1). Since 2007, corporate debt has risen incrementally to $12tn, with larger gains in financial business holdings. Mutual fund holdings have increased 91% to $1.7tn, while funding corporation assets have grown 643% to $0.9tn (Chart 2).

Conversely, money market assets have plunged 75% to $0.1tn, broker dealer holdings have fallen 56% to $0.2tn and private depository institution assets have declined 31% to $0.8tn. In total, the largest holders of corporate bonds are the rest of world ($2.4tn), life insurers ($2.1tn), households ($1.9tn) and mutual funds ($1.7tn).

In comparison, Treasury securities outstanding grew from $3.3tn to $5tn from 2000-2007 (Chart 3). Since 2007, Treasury debt has surged to $11.2tn, with outsized (relative) gains in household assets and large (absolute) increases in rest of world and financial holdings. Household holdings have risen 368% to $1tn, private pension assets have grown 172% to $0.5tn, and money market holdings have gained 156% to $0.5tn (Chart 4). However, the largest holders of Treasury securities are the rest of world ($5.4tn, roughly 70% of which are global central banks) and the Federal Reserve ($1.6tn).

Finally, corporate equities outstanding increased from $17.6tn to $25.6tn pre-crisis (Chart 5) and, since 2007, have not changed. Amounts are reported at market value, whereas fixed income values are reported at par value. Exchange-traded fund holdings have risen 83% to $1tn; in nominal terms, the increase roughly offsets the 9% decline to $5tn in mutual fund assets (Chart 6). Private pension holdings have fallen 16% to 2.3tn, while rest of world assets have increased 23% to 3.5tn. The largest holders of corporate equities are households ($9.9tn), mutual funds ($5tn), rest of world ($3.5tn) and private pensions ($2.3tn).

In summary, we would make a few simple observations.

First, we believe the thesis of a great rotation out of Treasury securities into corporate equities is a fallacy. The Federal Reserve and global central banks are the dominant holders of Treasuries; if they decide to sell, the money will not directly flow into equities.

Second, the thesis of a great rotation out of corporate credit into equities is complicated by three main cross-currents:

- First, the largest holders of corporate credit are a diverse bunch: rest of world investors typically pursue U.S. corporate assets for reasons other than price, namely diversification and liquidity benefits. Life insurers have income targets to meet and regulatory restrictions limit the capacity for equity investments. Both groups appear unlikely to unwind credit positions.

- Second, whilst household and mutual fund holdings could be less stable than institutional holdings, selling from households and mutual funds we believe would require the macro environment to shift significantly: either interest rates would have to rise materially (presuming global central banks will allow this to occur) or a series of unexpected shocks would need to cause a spike in market volatility, which would negatively impact high yield but high grade less so. We would note that at least one-quarter of high yield assets are directly held by hybrid funds, which can allocate between high yield and equities.

- Third, given different majority holders across fixed income and equities and investor allocations increasingly driven by regulation, new allocations to equities driven by income gains and greater consumer confidence would seem to be a more probable scenario.

In short, perhaps the Great Rotation debate is much ado about nothing?