by Russ Koesterich, CFA, JD, Portfolio Manager, Blackrock

Portfolio Manager and Managing Director, Russ Koesterich discusses the recent volatility and how the bull market foundation is still intact.

By Russ Koesterich, CFA, JD

Unless you happen to be long a portfolio of energy stocks, you are likely keenly aware that markets have gotten off to the worst start to the year since the financial crisis. Investors have also had to navigate the most violent style rotation in years. Losses in growth have not been limited to tech; even established, profitable mega cap names are down 15% or more.

While the sell-off began with a spike in nominal and real rates, investor crowding and concerns over Ukraine have exacerbated the selling. All of this raises the question: Is recent volatility simply a typical correction or the start of a new bear market? My baseline is a correction, with stocks ending the year higher. That said, 2022 is likely to be year of modest returns and higher volatility -- both of which suggest lowering risk.

Bull market foundation still intact

At a high level the bull case for stocks rests on a few simple facts: nominal GDP (NGDP) should remain above trend, the Federal Reserve is removing excess liquidity but financial conditions are not tight, and valuations have already moderated.

Starting with the real economy, growth is slowing but is likely to remain well above trend. Combining real growth with inflation, NGDP should top 7%. This is important as earnings and revenue track NGDP. Nominal GDP of around 7% suggests earnings growth in the 15-20% range.

The pushback on the bull case is that while earnings may continue to grow, stocks are expensive, and multiples will contract as financial conditions tighten. While tight financial conditions would arguably lead to lower multiples it’s important to note that on an absolute basis financial conditions are not tight, and multiples have already compressed.

Thinking about financial condition as both the cost and availability of money, credit spreads remain narrow, suggesting availability, and real or inflation-adjusted interest rates are decidedly negative, indicating money remains cheap. Real rates should continue to normalize but at -60 basis points, real 10-year yields remain well below the post-GFC average of approximately 40 bps. In short, the Fed is looking to remove excess accommodation and tame inflation, not crush the economy.

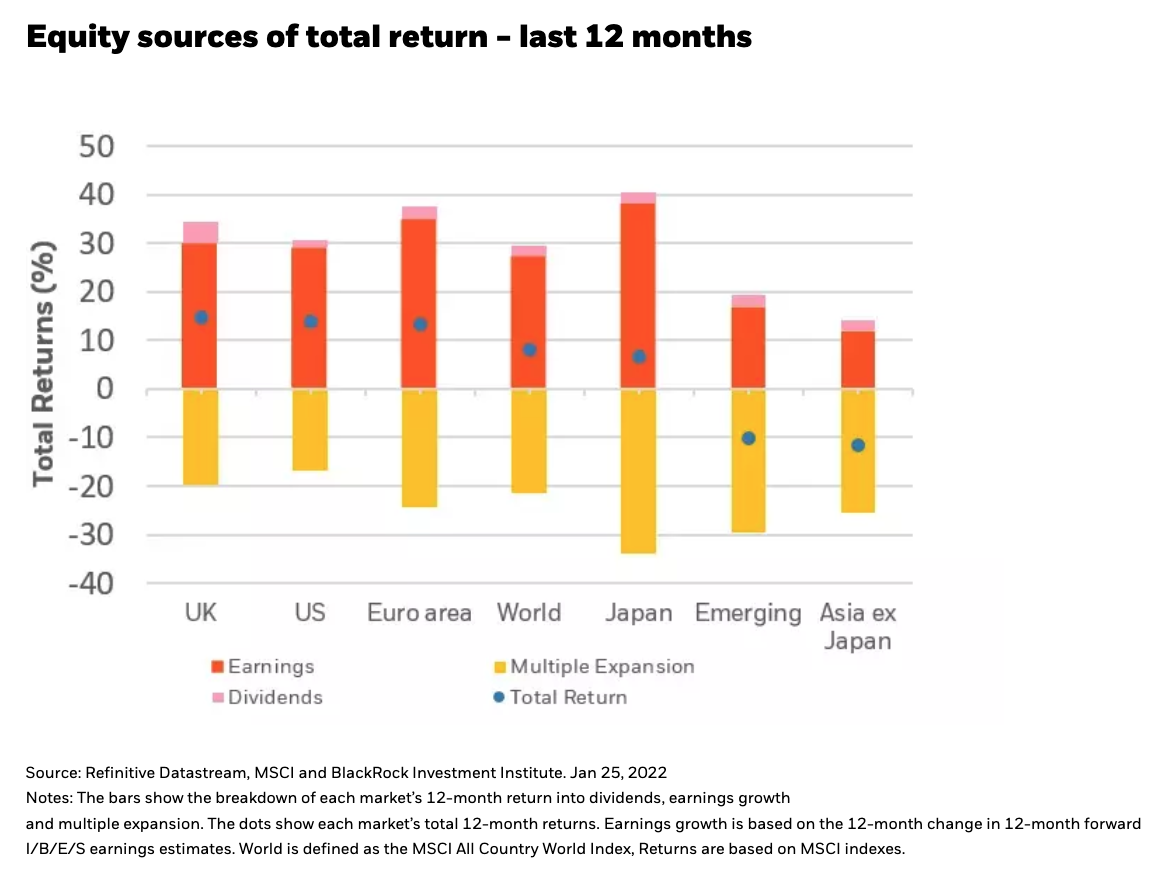

On the valuation side, multiples have been repricing for more than a year (see Chart 1). This doesn’t mean that stocks are cheap, but they are more reasonable than at the recent peak. While multiples are unlikely to expand as the Fed tightens, they should prove more resilient in the United States as the market is dominated by exceptionally profitable companies that demand some premium.

Long stocks but manage risk

With strong earnings growth and perhaps less multiple compression than many think stocks should produce decent, positive returns for the year. That said, risk is heightened and a Fed tightening cycle will keep volatility elevated, all of which suggests lower risk-adjusted returns. Bottom line: Investors should maintain an overweight to stocks and select credit, but at the margin lower their risk.

Russ KoesterichPortfolio ManagerRuss Koesterich, CFA, is a Portfolio Manager for BlackRock's Global Allocation Fund and the lead portfolio manager on the GA Selects model portfolio strategies.

Russ KoesterichPortfolio ManagerRuss Koesterich, CFA, is a Portfolio Manager for BlackRock's Global Allocation Fund and the lead portfolio manager on the GA Selects model portfolio strategies.