by Brooks Ritchey, Franklin Templeton Investments

In our view, pricing dislocations between companies, industries, regions and asset classes due to the impact of COVID-19 and corresponding price adjustments offer abundant opportunities for select hedged strategies. The length and depth of both the economic supply-and-demand curve adjustments are key to the richness and tenor of the opportunities.

Macro Themes We Are Discussing

Sector, Geographical and Cross-Asset Rotations in Full Swing

Even before COVID-19 affected global markets, we were expecting sector rotations, geographical movements and asset class rebalancing to occur, creating a rich environment for alpha1 generation. Today, the theme is even stronger, but due to the depth and length of the COVID-19 impact, the energy sector, as well as several industries including transportation, travel, restaurant and retail shopping now face challenges that were never part of the business plan. Technology, health care, online gaming and entertainment, and food delivery are experiencing tailwinds also not foreseen. Regional differences in social distancing, hence infection rates, will affect countries and regions in various ways. We expect interest rates and foreign exchange rates to provide a “relief valve” for pressures elsewhere, creating a viable opportunity set for managers deploying risk in those asset classes.

How Long and How Deep Will COVID-19 Impact the Economy, Consumer and Government Actions?

Clearly, both demand and supply curves are in the midst of repricing the impact of COVID-19, which we have labelled a health crisis impacting the financial and labour markets. The length and depth of COVID-19’s impact will affect the speed and degree of repricing going forward. If the global infection curves flatten and/or a vaccination becomes available, then mean reversion of risk-on repricing will quickly emerge. On the other hand, if the death count rises to unimaginable numbers, the virus mutates or the lockdown continues longer than a few months, then risk-off sentiment will likely return and be reflected in security pricing.

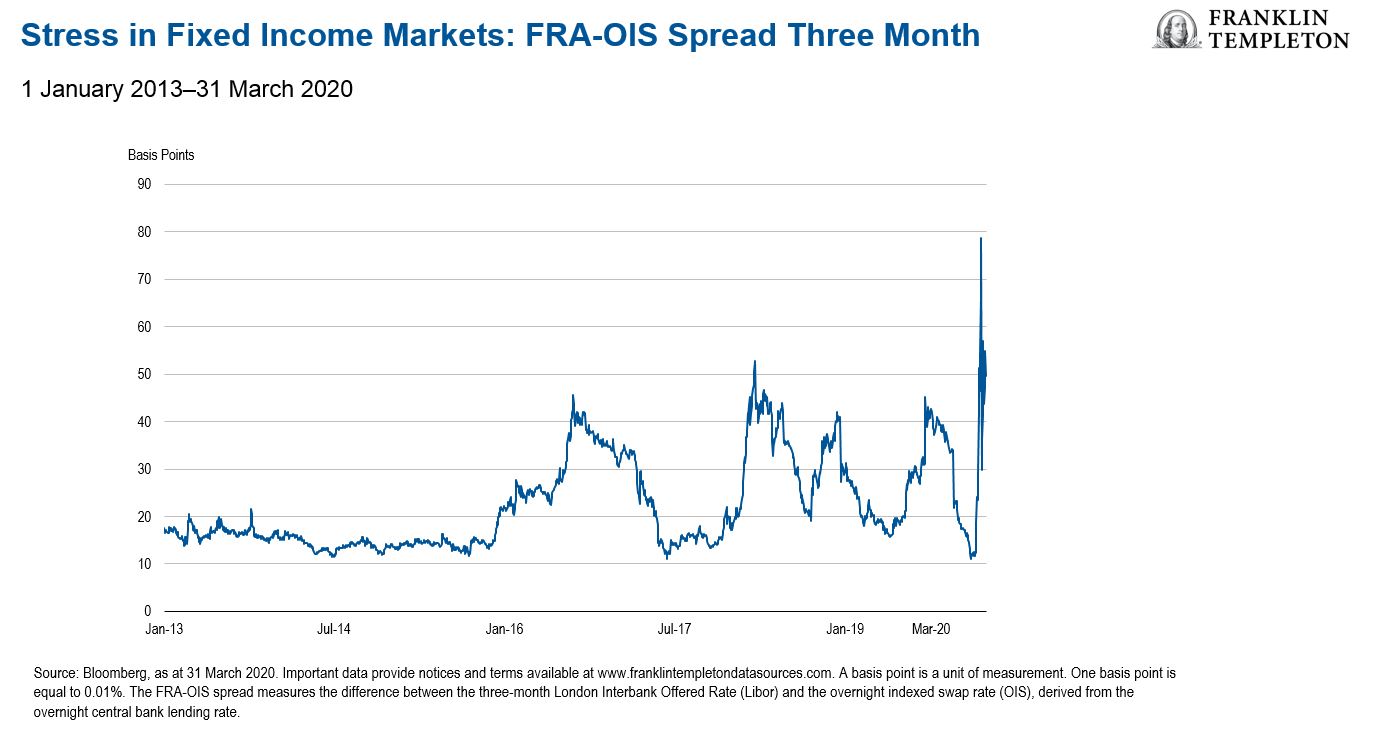

Has the Health Crisis Created a Deleveraging and Risk-Reducing Unwind?

In mid-February, no one wanted to hold cash as money market rates were paying very little in yield, if anything, and the opportunity cost of missing out on other investment opportunities was estimated to be large—even larger if one were to borrow at historically low rates and employ leverage to enhance return on investments. The leverage unwind and “dash for cash” put central banks in the position of having to lower interest rates and buy securities from the crowd looking to unwind and reduce risk. This has created dislocation in areas of sovereign fixed income, corporate credit and structured credit, with the largest dislocation occurring in structured credit.

How Long Can Volatility Stay this High?

The best trade over the last 10 years has been to be short volatility, sell volatility spikes, and be short gamma. Numerous firms were created and prospered utilising such strategies and methodologies. COVID-19 killed these strategies in one big swoop in March 2020, putting some firms out of business and causing managers relying solely on this approach to have unthoughtful losses and at a faster rate than ever imagined. As in most risk-off scenarios, volatility rose, liquidity evaporated and correlations spiked. For all hedged strategies, this was a huge challenge to navigate such an environment.

Managers that adapted quickly fared better than those that did not. In general, convergent strategies were very challenged and divergent strategies performed better.

In Conclusion…

We think the bull run of one-dimensional passive beta2 play has ended. The current market turmoil puts active investment management in vogue again. We strongly believe that skilled active managers who have access to a full toolbox to express their views are best positioned to take advantage of a very dynamic marketplace going forward.

First-Quarter 2020 Outlook: Strategy Highlights

Hedge Fund Strategies Referenced

Long/Short Equity: A directional strategy that involves taking a long (bullish) position and a short (bearish) position in equity or equity-linked instruments. The manager takes a long position in stock that they believe will outperform, while shorting stock that they believe will underperform.

Discretionary Global Macro: Trade across a broad range of asset classes, such as equity, fixed income, currency and commodity markets, focused on seeking to exploit opportunities that emerge from underlying global economic themes. Managers typically employ a top-down approach to concentrate on forecasting how political trends and global macroeconomic events affect the valuation of financial instruments and profit from correctly anticipating movements in global markets and holding positions in virtually any asset class.

Fixed Income Relative Value: Relative value strategies focus on the price relationship between

a pairing of securities (e.g., fixed income) to identify any price anomalies and capitalise on them as the price relationship normalises.

Discretionary Global Macro

Periods of heightened volatility can provide a robust opportunity set for discretionary macro strategies, which may profit from the dislocations themselves or from the resulting mispricings. We think nimble cross-asset managers can find success in the current environment as volatility remains above stubbornly low levels endured in recent years and as macro trends continue to dominate the prevailing market narrative. Recent dislocations may also provide the foundations for an attractive opportunity set for longer-term, value-driven strategies.

Fixed Income Relative Value

Various metrics of risk and volatility in traditional fixed income are showing historic levels of stress, propagating through to even the most liquid parts of the capital markets. Significant coordinated efforts by the various central banks and regulators are now laser-focused on restoring liquidity and stability in these markets, which serve as the backbone of capital flow activity and the primary mechanism for delivering federal stimulus to the real economy. These types of dislocations and subsequent recoveries can present incredibly attractive trading opportunities for well-capitalised managers focused on relative value strategies across a broad range of capital markets.

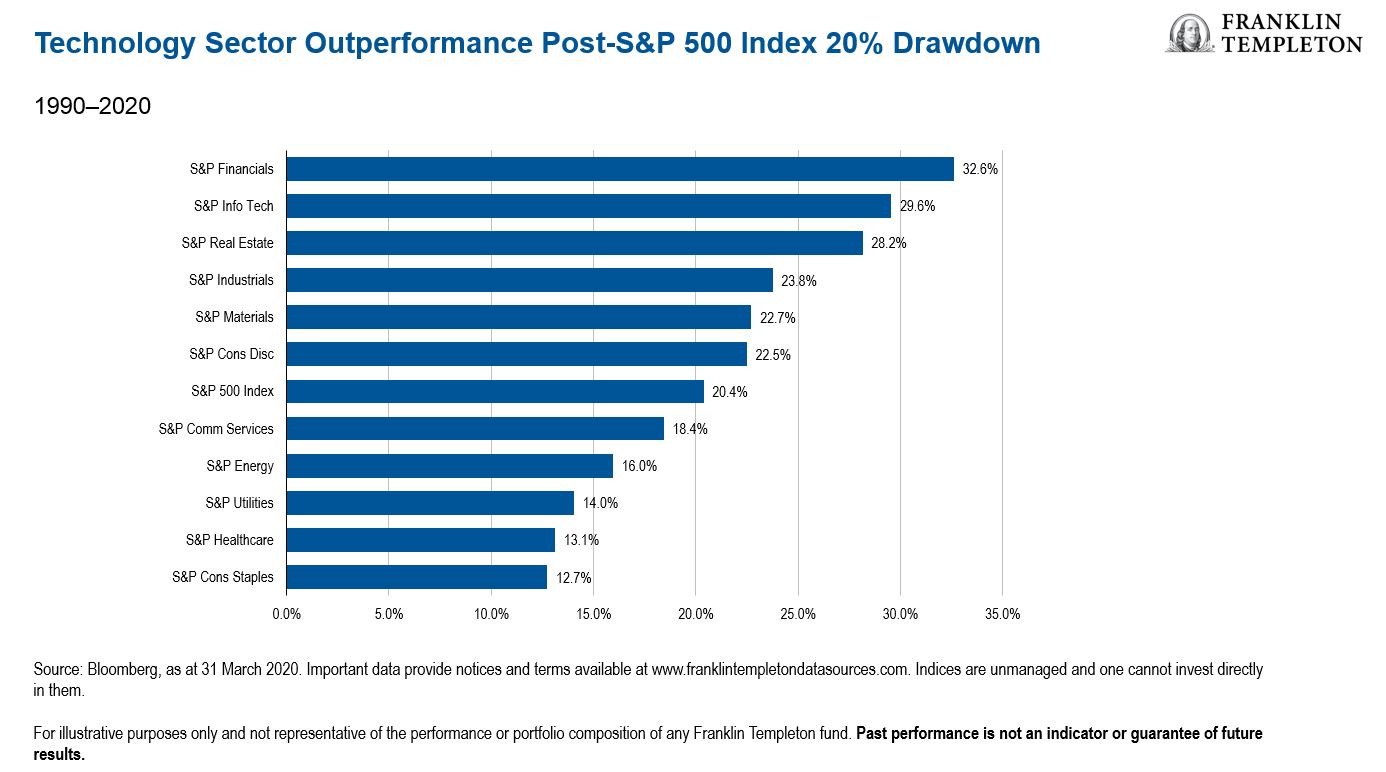

Long/Short Equity—Technology

We expect Long/Short Equity—Technology managers to be able to exploit both alpha and beta opportunities going forward. Dispersion, which is the alpha opportunity, should be broad-based across the technology sector. There are technologies that have been integral to the economy as companies have shifted to a nearly complete mobile working environment through cloud infrastructure and other remote software while other companies have seen business come to a halt.

Examples of winners vs. losers could include cloud vs. on-premises; domestic production vs. global supply chain; e-commerce vs. retail; e-payments and banking vs. ATMs and point of sale; and software vs. hardware. There is also a beta opportunity as technology companies historically emerge as winners following significant drawdowns. In the past six periods when the S&P 500 Index has sold off at least 20%, the technology sector has outperformed the S&P 500 Index in the subsequent three months as cyclical sectors outperform defensive sectors.3

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at April 13, 2020, and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

The information in this document is provided by K2 Advisors. K2 Advisors is a wholly owned subsidiary of K2 Advisors Holdings, LLC, which is a majority-owned subsidiary of Franklin Templeton Institutional, LLC, which, in turn, is a wholly owned subsidiary of Franklin Resources, Inc. (NYSE: BEN). K2 operates as an investment group of Franklin Templeton Alternative Strategies, a division of Franklin Resources, Inc., a global investment management organization operating as Franklin Templeton.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Investments are not FDIC insured; may lose value; and are not bank guaranteed.

What Are the Risks?

All investments involve risks, including possible loss or principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Investments in alternative investment strategies and hedge funds (collectively, “Alternative Investments”) are complex and speculative investments, entail significant risk and should not be considered a complete investment programme. Financial Derivative instruments are often used in alternative investment strategies and involve costs and can create economic leverage in a portfolio, which may result in significant volatility and cause losses (as well as gains) in an amount that significantly exceeds the initial investment. Depending on the product invested in, an investment in Alternative Investments may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. There can be no assurance that the investment strategies employed by K2 or the managers of the investment entities selected by K2 will be successful.

The identification of attractive investment opportunities is difficult and involves a significant degree of uncertainty. Returns generated from Alternative Investments may not adequately compensate investors for the business and financial risks assumed. An investment in Alternative Investments is subject to those market risks common to entities investing in all types of securities, including market volatility. Also, certain trading techniques employed by Alternative Investments, such as leverage and hedging, may increase the adverse impact to which an investment portfolio may be subject.

Depending on the structure of the product invested, Alternative Investments may not be required to provide investors with periodic pricing or valuation and there may be a lack of transparency as to the underlying assets. Investing in Alternative Investments may also involve tax consequences and a prospective investor should consult with a tax advisor before investing. In addition to direct asset-based fees and expenses, certain Alternative Investments such as funds of hedge funds incur additional indirect fees, expenses and asset-based compensation of investment funds in which these Alternative Investments invest.

For timely investing tidbits, follow us on Twitter @FTI_Global and on LinkedIn.

___________________________________

1. Alpha represents a mathematical value indicating an investment’s excess return relative to a benchmark. It measures a manager’s value added relative to a passive strategy, independent of the market movement.

2. Beta represents a measure of a security’s or portfolio’s volatility in comparison to the stock market as a whole; the market (or index) is assigned a beta of 1.00.

3. Indices are unmanaged and one cannot invest directly in them. They do not reflect any fees, expenses, or sales charges. Past performance is not an indicator or a guarantee of future results.

This post was first published at the official blog of Franklin Templeton Investments.