2018 has been a tough year to navigate financial markets. What’s the outlook ahead? Richard shares three market themes to focus on in 2019.

It has been a tough year to navigate financial markets. We have seen more than $6.9 trillion shaved off global market cap since the equity market’s peak in January, and many equities have sold off despite strong earnings reports. We may end 2018 with a rare event: negative annual returns for both stocks and bonds. The culprits: uncertainty over trade disputes, late-cycle concerns and tighter financial conditions.

Where to next? Roughly 100 BlackRock investment professionals recently gathered for two days to talk markets and the outlook for 2019. A major takeaway from our discussions: Three themes are likely to shape markets in 2019, as we write in our 2019 Global investment outlook.

Theme 1: Growth slowdown

We see a slowdown in global growth and corporate earnings in 2019, with the U.S. economy entering a late-cycle phase. Our BlackRock Growth GPS has been trending lower across the U.S. and euro-zone, pointing to a slower pace of growth in the 12 months ahead. We see U.S. growth stabilizing at a much higher level than other regions, even as the fading effects of domestic fiscal stimulus weigh on year-on-year growth comparisons. This underscores our preference for U.S. assets within the developed world. We expect the Chinese growth slowdown to be mild, as the country appears keenly focused on supporting its economy via fiscal and monetary stimulus.

Slowing growth and the impact of tariffs make for a more cautious corporate outlook, with global earnings growth likely to moderate. In the U.S., the expected slowdown partly reflects a higher hurdle versus 2018 when corporate tax cuts provided a big boost to company earnings. U.S. earnings growth estimates look set to normalize from a heady 24% in 2018 to 9% in 2019, consensus estimates from Thomson Reuters data show. This is still above the global average. Emerging markets (EM) are set to maintain double-digit earnings growth, led by China as its tech sector recovers and a pivot toward economic stimulus supports its economy. The U.S. and EMs remain our favored regions, as we see U.S. and EM companies best positioned to deliver on expectations. Yet we expect muted returns for both stocks and bonds in 2019 against a backdrop of slowing growth.

Read more market insights in our latest Global investment outlook.

Theme 2: Nearing neutral

We see the process of tightening financial conditions pushing yields up (and valuations down) set to ease in 2019. Why? U.S. rates are en route to neutral—the level at which monetary policy neither stimulates nor restricts growth —and the Federal Reserve looks likely to pause its tightening process. Our analysis pegs the current U.S. neutral rate at around 3.5%, a little above its long-term trend. While uncertainty abounds over where neutral lies in the long run, our estimate sits in the middle of the 2.5% to 3.5% range identified by the Fed. We currently see a rate near the top of this range needed to stabilize the U.S. economy and debt levels. Yet we expect the Fed to become more cautious as it nears neutral. As a result, we expect the FOMC to pause its quarterly pace of hikes amid slowing growth and inflation in 2019. We see the pressure on asset valuations easing as a result. Europe and Japan will likely take only timid steps toward normalization. We don’t expect the European Central Bank to raise rates before President Mario Draghi’s term ends in late 2019.

Theme 3: balancing risk and reward

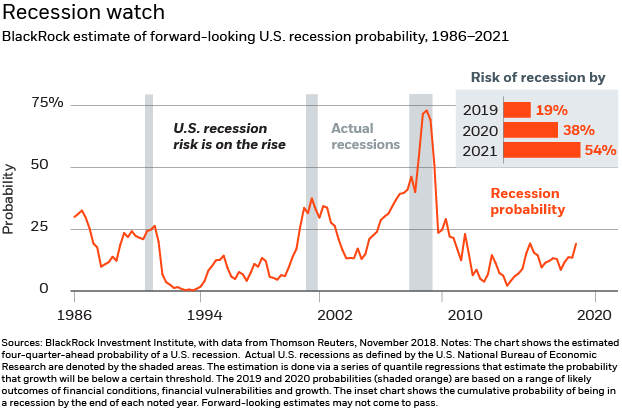

Recession fears are joining trade as a key market worry in 2019. Markets are vulnerable to fears that a downturn is near, even as we see the actual risk of a U.S. recession as low in 2019. Still-easy monetary policy, few signs of economic overheating and a lack of elevated financial vulnerabilities point to ongoing economic expansion in 2019. Yet the odds are set to rise steadily thereafter by our analysis, with a cumulative probability of more than 50% that recession strikes by end-2021. See the chart below.

Trade frictions and a U.S.-China battle for supremacy in the tech sector also loom over markets. We see trade risks more fully reflected in asset prices than a year ago, but expect twists and turns in trade negotiations to cause bouts of anxiety. Increasing uncertainty points to the need for quality assets in portfolios—but also potential for upside should market fears about trade ebb in 2019.

We advocate a barbelled approach for carefully balancing risk and reward: exposures to government debt as a portfolio buffer, twinned with high-conviction allocations to assets that offer attractive risk/return prospects. Quality has historically outperformed other equity style factors in economic slowdowns, our analysis shows. We see EM equities as good candidates for the other end of the barbell. What to avoid? Assets with limited upside if things go right, but hefty downside if things go wrong. We see many credit and European assets falling into this category.

Richard Turnill is BlackRock’s global chief investment strategist. He is a regular contributor to The Blog.