THIRD QUARTER 2017

Unhedged European and EM Equities Bargain Priced For Limited Time

by David Wolf, Portfolio Manager, and David Tulk, CFA, Institutional Portfolio Manager, Fidelity Investments Canada

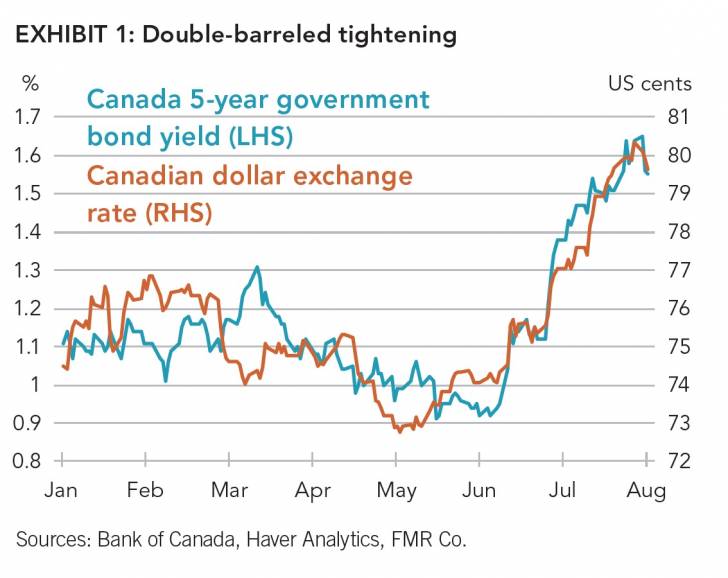

An abrupt hawkish shift in tone from the Bank of Canada has culminated in the first increase in the overnight lending rate in nearly seven years, causing both the Canadian dollar and bond yields to reprice higher (see Exhibit 1). The Bank’s decision reflected a considerable upgrade in their assessment of Canada’s economic prospects. Our own outlook has been far more cautious, and has been reflected in a material underweight to Canadian assets across our multi-asset class funds. The Bank’s recent actions, and the financial markets’ response to them, make it more likely that the downside risks to Canada’s economy we’ve been concerned about will be realized on the visible horizon. As a result, we are diversifying further from the domestic market into unhedged foreign assets. We discuss the rationale for this decision below.

The addition of Bank of Canada tightening as a headwind to the Canadian economy has strengthened our conviction in the risks to the performance of domestic assets, and the resulting short-term squeeze higher in the Canadian dollar has made unhedged foreign assets that much cheaper on a relative basis.

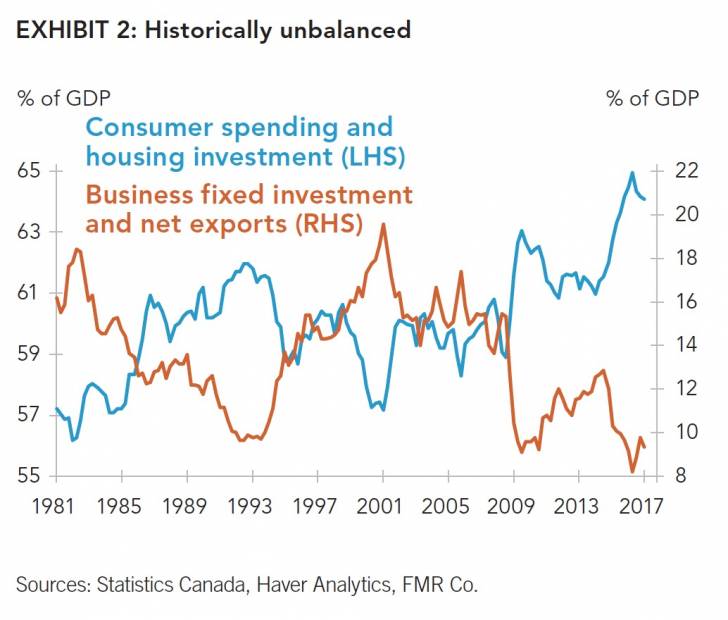

The combination of very accommodative monetary policy and a sluggish global recovery has left the Canadian economy severely unbalanced. Household spending, notably on housing and consumer durables, has been pretty much the only game in town in recent years, while more productive sectors of the economy such as business investment and exports have stagnated (see Exhibit 2). The ratio of household debt to personal disposable income in Canada remains near its record high, while the valuations of the Toronto and Vancouver housing markets – together representing roughly half of the national housing market by value – have become increasingly detached from local fundamentals.

Both the U.S. and Europe have demonstrated in recent years that the balance sheet repair that is required following a debt boom can represent a multi-year headwind to economic growth. That process still lies ahead in Canada, and its beginning looks to be coming into focus. The combination of tighter regulations from the federal, BC and Ontario governments (including those targeting foreign capital) and emergent concerns surrounding lower-tier mortgage lenders had already begun to affect the price and availability of credit in Canada, and more broadly to shift the psychology in the housing market. The recent jumps in longer-term interest rates around the Bank’s rate hike will add to the pressure.

In our view, it is likely that this cocktail of tightening will bring to an end the outsized contributions of household spending to Canadian growth. The housing market doesn’t have to go down for that to happen – it just has to stop going up. And there is clearly risk of a much worse outcome, as the reaction of a levered market to even a small shift in conditions is inherently unpredictable. Since the Bank last tightened, house prices nationally are up 50%, and households have added more than $580 billion to their debt loads, even as credit creation has increasingly moved into the shadows in response to prior government attempts to curb excesses in the more regulated areas of the financial system.

Even at the better end of this spectrum, we’re likely to ‘lose’ housing and its broader support to household demand as a driver of growth in Canada. And it’s hard to see what will replace it. The recovery in exports this cycle has already been historically weak, even with the sustained depreciation of the Canadian dollar from US dollar parity four years ago. Moreover, the 10% jump in the currency in just the past two months will represent a further setback. And while capital spending in Canada has stopped going down as the collapse in energy investment has run its course, a sustained pick-up looks unlikely. Business fixed investment has been stubbornly weak in just about every major economy; why should Canada be an exception, particularly given uncertainty surrounding access to the US market as NAFTA is renegotiated?

Thus it seems almost inevitable that as housing softens and households retrench, overall growth will slow. This can be expected to have two particular consequences relevant to our fund positioning in Canadian markets.

Sources: Statistics Canada, Haver Analytics, FMR Co.

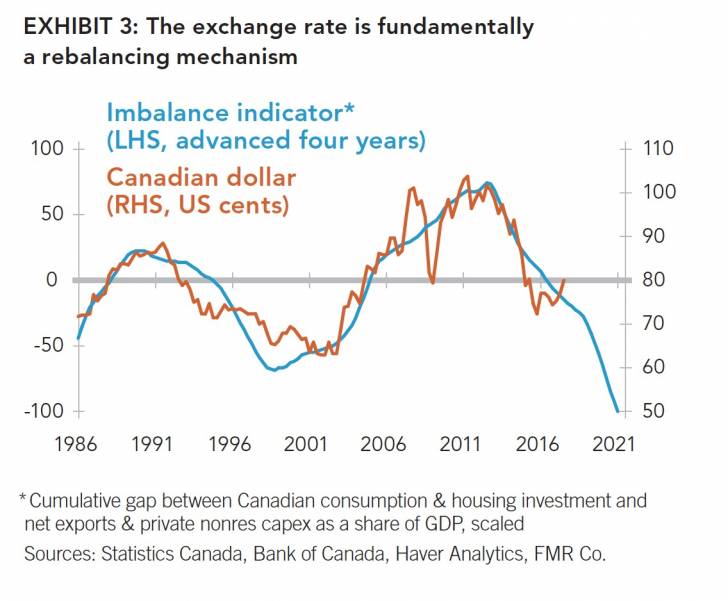

First, it will represent a headwind for the financials-heavy Canadian equity market, given the longstanding reliance of growth in bank earnings on the sustained strength of the Canadian consumer. Second, it will tend to force the Canadian dollar back down, as Canada will require a marked improvement in competitiveness to allow investment and exports to thrive as household demand comes off the boil. The exchange rate is, at its core, the primary rebalancing mechanism between foreign and domestic demand, and Exhibit 3 shows the scale of the adjustment that may prove necessary following many years of domestic excess. Note that the imbalance indicator in Exhibit 3, which we’ve shown before, is a function of the cumulative gap between the sectors of demand shown in Exhibit 2.

In sum, the addition of Bank of Canada tightening as a headwind to the Canadian economy has strengthened our conviction in the risks to the performance of domestic assets, and the resulting short-term squeeze higher in the Canadian dollar has made unhedged foreign assets that much cheaper on a relative basis. We are taking advantage by adding to our positions in foreign markets where the opportunities look most favourable, which at this stage remain outside of North America (see Tilting towards EM, Europe).

David Wolf and David Tulk, August 4, 2017

Follow Fidelity Canada on Twitter @fidelitycanada

*****

Authors

David Wolf | Portfolio Manager David Wolf is a portfolio manager for Fidelity Investments. He is the co-manager of Fidelity Managed Portfolios, Fidelity Canadian Asset Allocation Fund, Fidelity Canadian Balanced Fund, Fidelity Monthly Income Fund, Fidelity U.S. Monthly Income Fund, Fidelity U.S. Monthly Income Currency Neutral Fund, Fidelity Global Monthly Income Fund, Fidelity Dividend Fund, Fidelity Global Dividend Fund, Fidelity Income Allocation Fund, Fidelity Balanced Managed Risk Portfolio, Fidelity Conservative Managed Risk Portfolio, Fidelity NorthStar® Balanced Fund and Fidelity Tactical Strategies Fund. He is also portfolio co-manager of Fidelity Conservative Income Private Pool, Fidelity Asset Allocation Private Pool, Fidelity Asset Allocation Currency Neutral Private Pool, Fidelity Balanced Private Pool, Fidelity Balanced Currency Neutral Private Pool, Fidelity Balanced Income Private Pool, Fidelity Balanced Income Currency Neutral Private Pool and Fidelity U.S. Growth and Income Private Pool.

David Tulk, CFA | Institutional Portfolio Manager David Tulk is an Institutional Portfolio Manager at Fidelity Investments. In this role, he serves as a member of the investment management team, maintaining a deep knowledge of portfolio philosophy, process, and construction. He assists portfolio managers and their CIOs in ensuring portfolios are managed in accordance with client expectations.

For Canadian investors

For Canadian prospects and/or Canadian institutional investors only. Offered in each province of Canada by Fidelity Investments Canada ULC in accordance with applicable securities laws.

Before investing, consider the funds’ investment objectives, risks, charges and expenses. Contact Fidelity for a prospectus or, if available, a summary prospectus containing this information. Read it carefully.

The information presented above reflects the opinions of David Tulk and David Wolf as at August 4, 2017. These opinions do not necessarily represent the views of Fidelity or any other person in the Fidelity organization and are subject to change at any time based on market or other conditions. As with all your investments through Fidelity, you must make your own determination as to whether an investment in any particular security or securities is consistent with your investment objectives, risk tolerance, financial situation and your evaluation of the security. Consult your tax or financial advisor for information concerning your specific situation.

Investing involves risk, including the risk of loss.

© 2017 Fidelity Investments Canada ULC. All rights reserved.

811690.1.0