by Craig Basinger, CFA, Connected Wealth, RichardsonGMP

It’s not a bubble but ETFs appear to be causing some distortions in the market

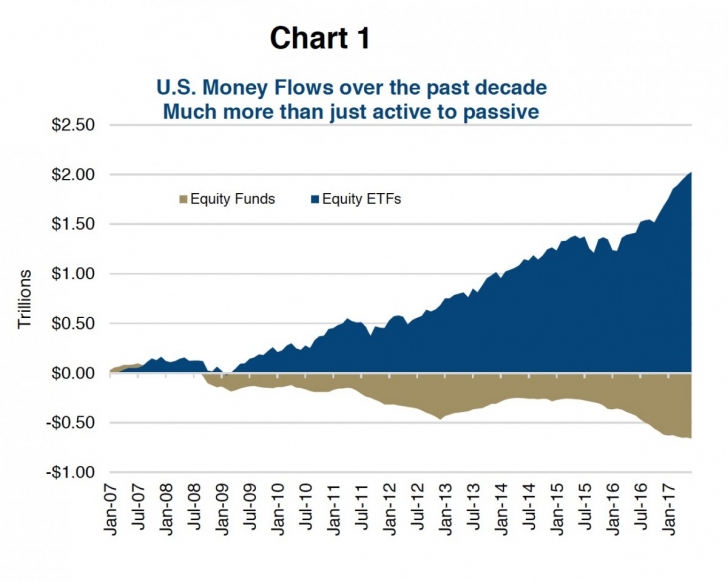

Exchange traded funds have gained in popularity over the past few decades as a great investment vehicle to get broad market exposure at a very attractive price point. This has greatly aided investors paying lower fees, which is a good thing. It has also helped speed change in the active management world. First by flushing out many of the ‘closet indexers’, those funds that just were not that different than the overall market, yet had high fees. It has also sped active managers to offer their services at a more attractive price point. Yay, lower fees again which we applaud. To give you an idea on this sea change, Chart 1 indicates the flows into equity funds (active) and equity ETFs (mostly passive) over the past decade representing over $2 trillion into equity ETFs while funds saw over $1/2 trillion leave.

You can probably see from the graph that this trend of money piling into ETFs has accelerated during the past year or so (note blue area of graph has become much steeper). We would point out that ETFs are much more than just broad market capitalization weighted indices these days, some are factor based, some are industry focused and some are now active. However, the majority of assets remain in the broad market exposure ETFs. And this has worked well for investors given strong market returns that has left most active managers trailing from a performance perspective (a trend evident in Canada and the U.S.).

As money has piled into ETFs, warnings of a bubble or a potential source of systematic risk in the market have been raised. We are not in agreement but do see distortions and pockets of potential systematic risk.

The Bubble Argument

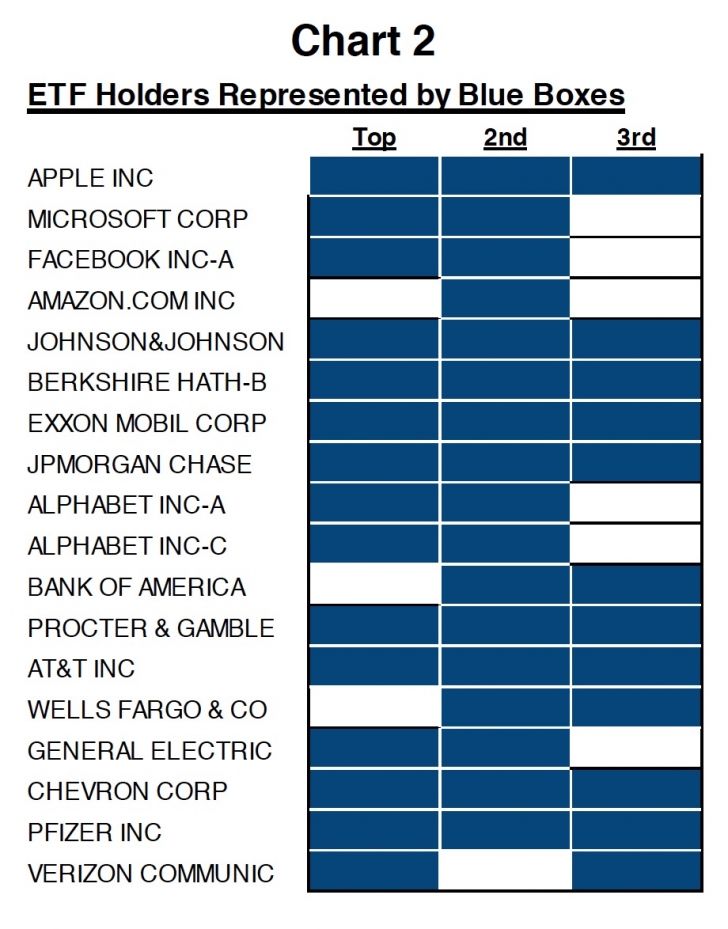

The premise behind the argument is as more money flows into ETFs, an ETF driven momentum trade in the market is created. Money goes in, ETF buys the basket of underlying securities based on the index, regardless of price, pushing prices higher, thus attracting more money chasing performance and so on. This inflow has caused the biggest 100 companies in the U.S. market, the S&P 100, to each have ETF managers Vanguard, Blackrock and State Street among their top holders (Chart 2). Given the new scale of ETFs, some are nervous and wonder what will happen in a bear market? Will the selling be as fast as the buying was? If the ETFs are selling, who will step in on the buy side? Will it cause a greater market drop?

The bubble argument can sound pretty legit, but as my lawyer friends often say, they can make any argument sound pretty legit. Chasing performance is not anything new, it’s just ETFs are the preferred vehicle this time around given those lower fees. And we should keep in mind there remains more money in active strategies than passive ETFs, by a considerable margin. Perhaps if there was a bubble bursting, it was the bubble of closet index funds that were charging higher fees.

The Distortion Argument

While we don’t buy the ‘ETF bubble’ argument, we do believe there is some price distortion and some pockets of systematic risk of which investors should be cognisant. And we threw some math at it.

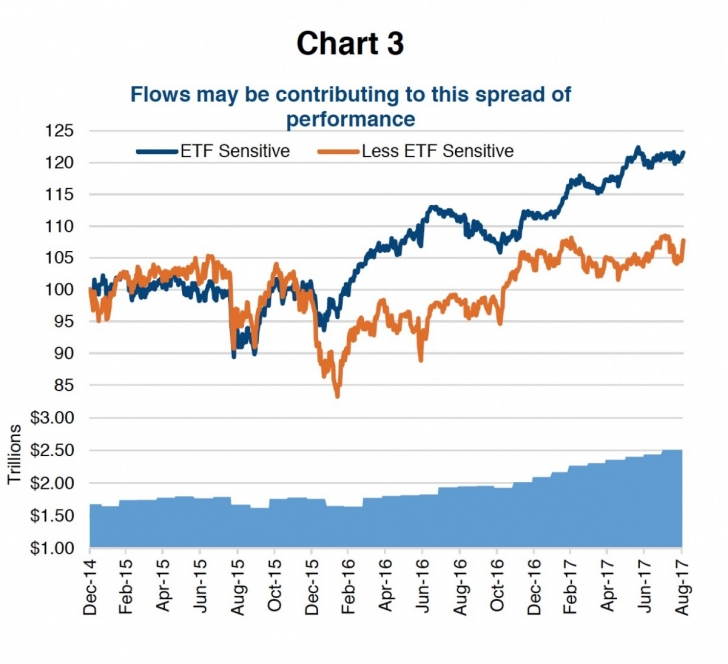

Net buying of ETFs results in money flowing into the market in varying amounts of buying across the index constituents. Since there are too many ETFs and too many indices, we had to simplify. We took the S&P 100, roughly the biggest 100 companies in the U.S. based on market cap. We then calculated how much volume per company would need to be traded given a certain inflow into the index from ETFs. We compared those volumes with the company’s historical average trading volume and sorted by this ETF flow sensitivity measure. Essentially ranking the 100 companies based on how sensitive they would be to ETF flows, given their index weight and historical trading volume. And when we say sensitive, we mean which companies may be more likely to be pushed up or down from ETF flows.

The ranked index was then broken down into two indices, ETF Sensitive and Less ETF Sensitive representing the top 25 and bottom 25. As an example Apple, which is the biggest company and receives the biggest portion of flows based on dollars, is somewhere in the middle. Sure Apple gets lots of ETF volume but it also trades a lot. On the other hand, Proctor & Gamble receives less in ETF flows but given lower liquidity is more sensitive to ETF flows.

Chart 3 is the performance over the past two and a half years of the ETF Sensitive and Less ETF Sensitive indices. The area chart on the bottom panel is total equity ETF holdings. It would appear around the time ETF assets started rising, the performance between ETF Sensitive and Less ETF Sensitive began diverging. While there may be other factors at play, it is not inconceivable that broad flows into ETFs may be inflating some companies more than others. Continued positive ETF inflows may continue to push the ETF Sensitives higher and valuations higher, while a reversal in flows could trigger a strong sell-off.

Systematic Risk

Systematic risk is really not evident in the broader equity markets due to ETF flows. Given size and market composition, we just don’t believe it supports the argument. If investors began dumping ETFs, this would not be that different than in past cycles when they would dump mutual funds.

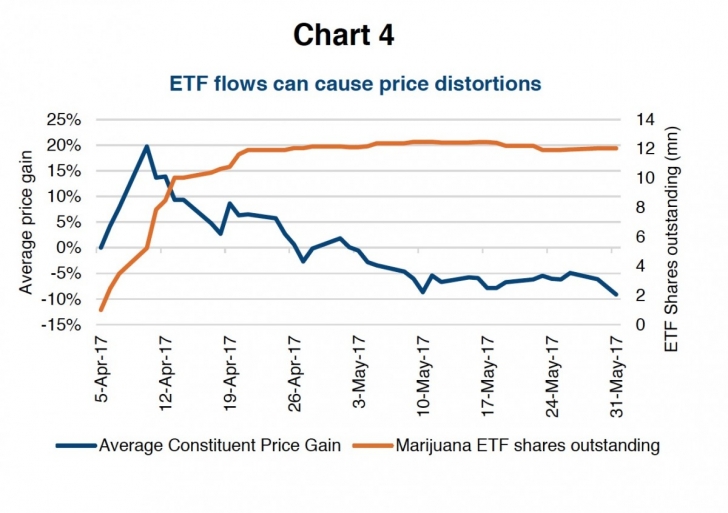

However, there are pockets that could pose risk. Some ETFs that are narrowly focused can in some cases mask illiquid markets with a more liquid ETF. If flows accelerate either in or out, this can cause a systematic problem if the underlying holdings are not very liquid. Narrowly focused industry ETFs are a good example. For instance, the money that flowed into the marijuana space certainly caused temporary price distortions in the underlying companies, given their normal lack of liquidity (Chart 4). Note the sudden rise in underlying stock prices as funds flowed into the ETF, which proved fleeting. Another example may be the high yield bond market. If there was a dramatic outflow, given bond inventories at dealers are historically low, this may cause liquidity risk.

Conclusion

The rise in popularity of ETFs is not a risk to the markets, in our view it is more a structural change. And markets are always changing over time, remember when everyone used to own individual stocks. However, there is some evidence that it is beginning to cause some price distortions as capital is flowing much more to certain companies than others. With distortion comes opportunity, notably for active managers. Understanding relative liquidity to relative ETF flows does open the door to profit from these distortions. But that is a much deeper topic than we have time for today, stay tuned.

*****

Charts are sourced to Bloomberg unless otherwise noted. This material is provided for general information and is not to be construed as an offer or solicitation for the sale or purchase of securities mentioned herein. Past performance may not be repeated. Every effort has been made to compile this material from reliable sources however no warranty can be made as to its accuracy or completeness. Before acting on any of the above, please seek individual financial advice based on your personal circumstances. However, neither the author nor Richardson GMP Limited makes any representation or warranty, expressed or implied, in respect thereof, or takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use or reliance on this report or its contents. Richardson GMP Limited is a member of Canadian Investor Protection Fund. Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

Copyright © RichardsonGMP