Two Approaches to Managing Volatility in High Yield - Context

by Fixed Income AllianceBernstein

February 14, 2017

These are uncertain times in markets, and that creates a dilemma for investors who need high levels of income but can’t stomach a high level of risk. We have a solution. Actually, we have two.

Investors who need income know it’s impossible to avoid risk altogether. And with global growth gaining traction and the Trump administration pushing deregulation, tax cuts and infrastructure spending, maintaining exposure to high-yielding “risk” assets makes sense.

Even so, there are plenty of things that could upend the current growth trajectory and provoke market turbulence. Antiestablishment parties could win upcoming French and German elections. Or President Trump could double-down on his immigration and trade policies—or simply spook markets with his rhetoric.

In other words, investors shouldn’t expect uninterrupted tranquility this year. That can be unsettling for investors because high-income investments such as high-yield corporate bonds or emerging market assets are usually the first to sell off when volatility spikes.

Yet pulling out of high-income sectors entirely isn’t an option for most investors, particularly when income is so hard to come by. Fortunately, staying exposed and limiting your risk aren’t mutually exclusive.

The key is finding a way to understand and manage the two major risks that bond investors face: interest-rate risk and credit risk. There are two paths investors can take.

Limit Duration—and Prioritize Quality

First, investors can shorten duration and focus on quality. Over time, high-quality, short-duration bonds have dampened portfolio volatility and held up better in down markets.

Duration is a measure of a bond’s sensitivity to changes in its yield. In general, bonds are highly sensitive to yield changes—when yields rise, prices fall. The shorter the duration, the less damage a rise in yields will do.

That’s important, because valuations in many parts of the high-yield market are stretched today, so there’s plenty of room for yields to rise. Average yields declined sharply last year and credit spreads—the extra yield that high-yield bonds offer over comparable government bonds—are hovering around their lowest level in more than two years. If faster-than-expected inflation obliges the Fed to quicken the pace of interest-rate hikes this year, that could slow economic growth. In that case, high-yield spreads could rise in a hurry.

But a short-duration strategy by itself isn’t enough. That’s because the primary risk for short-duration high-yield bonds is credit risk. And with many parts of the high-yield market in the later stages of the credit cycle, avoiding low-quality, CCC-rated “junk” bonds is critically important.

The Barbell Approach

Another way to manage volatility involves pairing high-yield credit with high-quality government bonds. Interest-rate sensitive US Treasuries and other high-quality government bonds, tend to perform well when growth slows. High-yielding credit assets, on the other hand, usually shine when economic growth accelerates and interest rates rise.

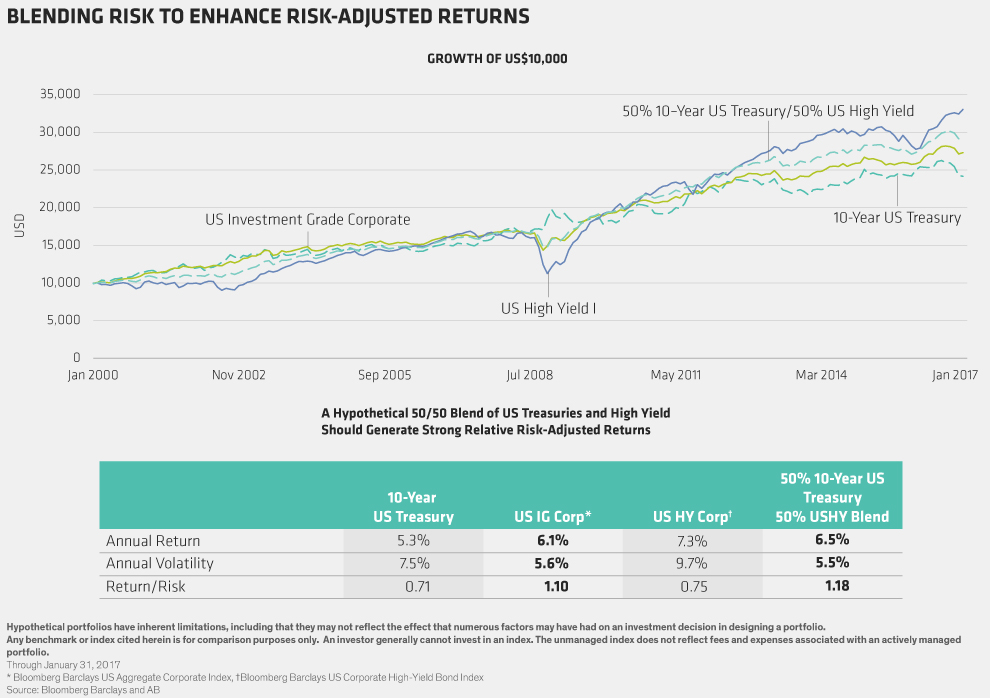

Combining these into a balanced barbell approach can help a bond portfolio weather most market environments. As the following display illustrates, a hypothetical 50-50 blend of the US 10-year Treasury and the Bloomberg Barclays US High-Yield Corporate Bond Index would over the past 16 years have delivered better risk-adjusted returns than portfolios invested solely in Treasuries, investment-grade corporate bonds or high yield.

Short-duration and barbell strategies can, like all strategies, lose money in down markets—but they generally lose less than strategies with higher interest-rate sensitivity and additional credit risk.

How investors choose to balance returns, risk and downside protection will vary depending on individual needs and comfort levels. The important thing is that it is possible to limit portfolio volatility when markets get messy without giving up altogether on your income goals.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein