Michael Lebowitz, CFA, Clarity Financial

In “What Me Worry” we noted that the closely watched equity volatility index (VIX) was at a level of investor complacency rarely seen, not only in election years but over decades of market history. We also mentioned anxiety surrounding the upcoming election is palpable, and that equity valuations are at rarefied levels without supporting earnings and economic data. Given these factors we ended the article with the following: “The market, courtesy of complacent investors, is offering very cheap insurance for an event that has the potential to induce extreme volatility via VIX options and futures. Even if the next eleven weeks leading to the election prove to be uneventful, the VIX at current levels, as shown earlier, has been a prudent place to own protection. We recommend you consider this opportunity as a protective measure”.

Unfortunately, most professional investment managers are not adept and/or able to trade VIX futures, options or volatility in other forms to hedge their client’s equity positions. More often than not, concerned managers will instead reduce perceived risk by selling a portion of their equity holdings and increasing cash positions and/or shifting portfolio allocations from equities to fixed income. It is in this vain that we discuss how the latter option, shifting money from equities to fixed income, has risks that were not as evident during the 2000 tech crash and the 2008 financial crisis.

MPT

Harry Markowitz developed the Modern Portfolio Theory (MPT) in the 1950’s. Simply put his theory argues that portfolio risk can be reduced by holding combinations of different securities and asset classes that are not positively correlated. We agree with the theory that there are benefits to diversification but we do not subscribe to MPT. Diversification makes sense when you buy uncorrelated assets that are undervalued. Buying assets for the sake of diversification without regard for valuation is fraught with risk regardless of how many different securities and asset classes one may hold. In the words of Warren Buffett “diversification is a protection against ignorance. It makes very little sense for those that know what they are doing”. To paraphrase Warren Buffet, diversification is for those that do not know what they are doing.

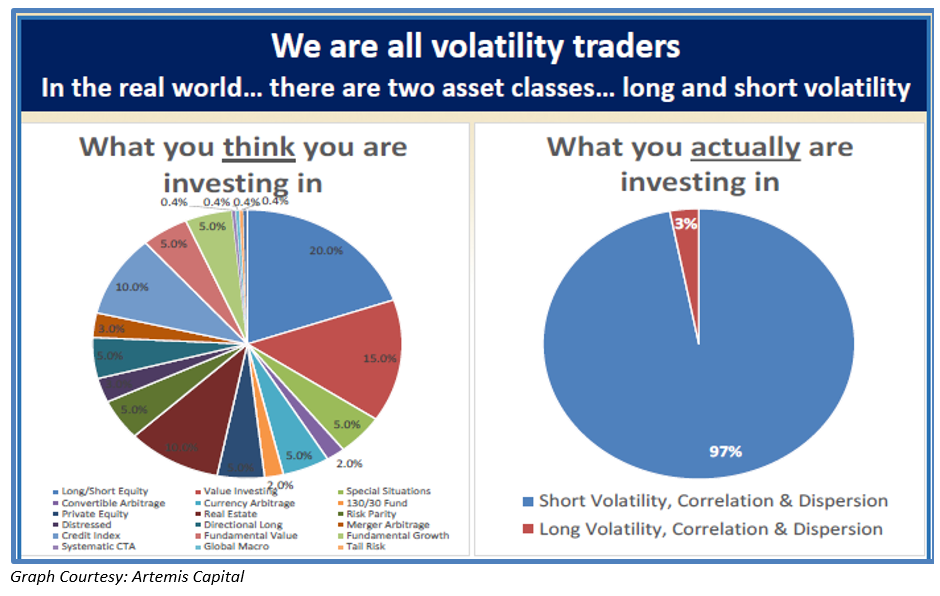

The truth of the matter is that blind diversification does not work simply because it does not take into account the effects of volatility on asset prices. Chris Cole from Artemis Capital, one of the clearest thinkers on the importance of volatility as an asset class, highlights this point in the following graphic.

Contrasting the perception of a well-diversified portfolio with the reality of embedded volatility, the graph reflects enormous concentration risk in short volatility. Importantly, this risk matters most at the exact point in time when one expects – hopes – their strategy of diversification will protect them. Unfortunately, the well-diversified portfolio (left side) turns in to the short volatility-concentrated portfolio in periods of extreme market disruption. Mr. Cole’s analysis may be best summarized with the popular statement that correlations on many assets go to one during a crisis.

Without regard for Mr. Buffett’s or Mr. Cole’s perspectives, many investment managers tend to hold “diversified” portfolios of stocks and bonds in various forms and strongly believe that such diversification will protect their portfolios in the event of a serious market correction. Unfortunately, many investors are not basing this diversification strategy on a fundamental analysis of bonds but largely on a blind assumption that bond prices will rise – yields will fall – in the event of trouble in the equity market.

Bonds

Sovereign bond markets around the world are trading at their lowest yields in decades and in some instances, including in the United States, in centuries. In fact there are approximately $13 trillion worth of global bonds that have negative yields.

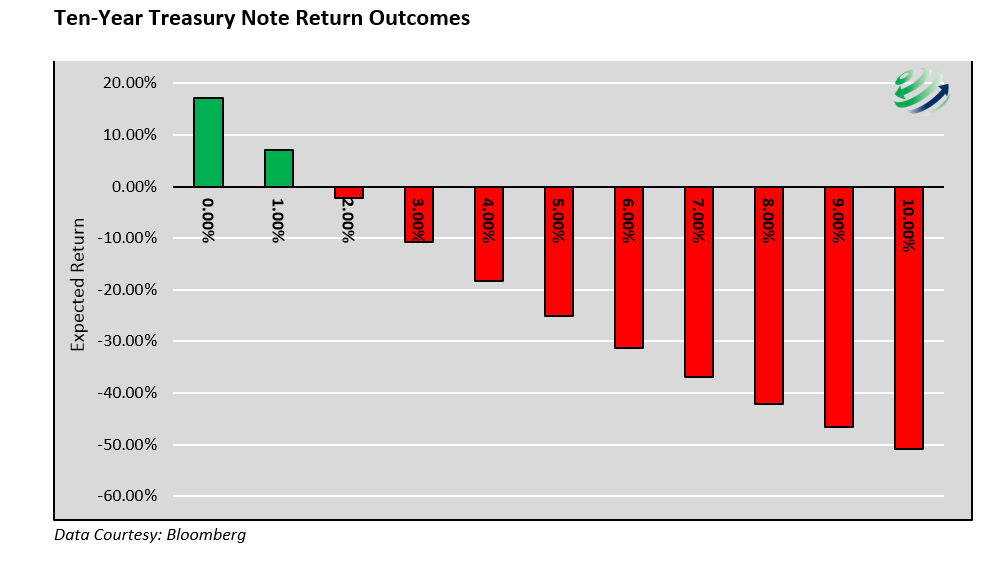

Bond investors today are faced with a unique problem resulting from these low yields. The potential for price increases versus price decreases is grossly asymmetric. In other words there is a lot more money to lose in bonds than can be made. To illustrate this consider a ten-year U.S. Treasury note maturing in August 2026, with a coupon of 1.50% annually, a price of 99.25 and a yield of 1.58%. The chart below shows a range of potential one-year total returns for various yield levels in the ten-year note described above. As a frame of reference the average yield during the 2008 crisis was 3.43%. If the yield on the current 10-year note were to rise to that level in a year an investor would suffer a loss of 14%.

Bond Upside

With the poor risk/reward skew in mind we turn back to the idea of using bonds to hedge against an equity market correction. If such a strategy is going to work, bond yields must fall further into record territory. Can this happen? We do not have the answer, nor does anyone else. Yields have already dropped well beyond the point that most professionals thought possible and given the potential for a deflationary economic recession, they may decline further. Additionally, the Federal Reserve will almost certainly employ bond friendly actions, as they have in the past, to quell equity market and economic turmoil. If Japanese and German ten-year notes are indications, U.S. Treasury yields can certainly go negative.

The question you must consider is, given extremely low yields and seemingly limited room to decline, do you have confidence that, in the event of an economic recession and severe equity market correction, yields will drop further? If so, then to what extent will such a decline protect you?

Bond Downside

If one is to hedge with Treasury securities, they must also consider what happens if yields do not decline during a market correction. What if “safe-haven” securities traditionally used for hedging purposes were to lose 5% to 10% or even 20% or more?

Below is a list of circumstances that could lead to rising bond yields, in a departure from prior major market corrections:

- Increased fiscal stimulus to combat a recession results in massive bond issuance

- S. Dollar decline incites international bond holders to sell

- Federal Reserve takes extreme actions (helicopter money) and inflation expectations soar

- Record low yields lead to a flight to safety in cash and precious metals instead of bonds

- Erosion of investor confidence in the ability of central bankers to protect markets

Current yield levels alter the traditional protection U.S. Treasuries and other bonds now afford. As James Grant of Grant’s Interest Rate Observer has stated, instead of risk-free return, one gets return-free risk. In other words, the past may not be prologue to the future. The hedging benefits that bonds have provided in the past do not appear to offer the same protection of prior periods. This analysis implies an important message for those looking to take a traditional equity hedging approach: the margin of error is quite small for anyone assuming that tomorrow will be like yesterday.

Summary

Recent history has favored those that used fixed income, especially U.S. Treasuries to hedge equity market drawdowns. That however does not take away one’s responsibility to question whether the current risk/reward proposition is still applicable. In a world of declining inflation, stagnating global economic growth and aggressive central bankers, such a hedging strategy may still make sense. However, we would be remiss if we did not reiterate a point made earlier – diversifying for diversification’s sake makes little sense if you are not buying assets that offer value.

There is relatively little upside for Treasury prices and a number of legitimate reasons yields could defy the pattern of the past 35 years and actually increase. Accordingly, one looking for true diversification should consider increasing cash positions, hedging with volatility instruments and/or options, and adding alternative assets such as precious metals.

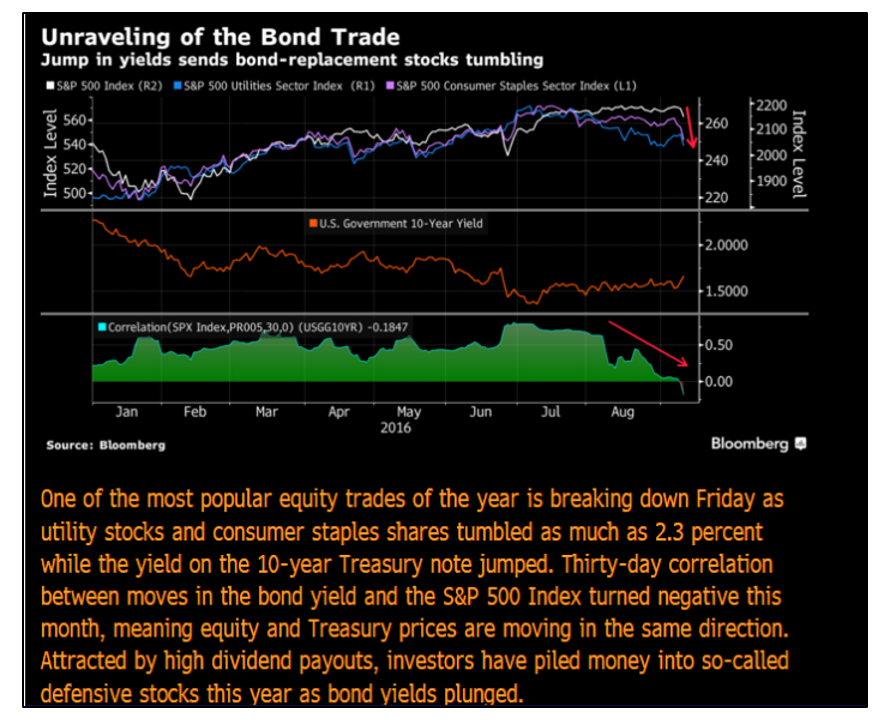

Finally, we were gratified to see this news clip posted from Bloomberg as we were finalizing this article.

Michael Lebowitz, CFA

Investment Analyst and Portfolio Manager for Clarity Financial, LLC. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director.Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Copyright © Clarity Financial